Written by: Thejaswini M A

Compiled by: Block unicorn

Preface

You would buy several Philips Hue smart bulbs because they are supposedly the best. Its app interface is sleek, colorful, and when you dim the lights with your phone, you feel like a tech genius, quite high-end.

Then you decide your thermostat should also be smart. Nest has the most powerful AI, so you buy that. Different applications, different accounts, but that’s okay, it’s just another feature.

Unbeknownst to you, your life has descended into chaos. Your Ring doorbell cannot communicate with your Alexa speaker, the Alexa speaker cannot control your Apple HomeKit garage door, and the garage door cannot connect with your Samsung SmartThings hub. You need four different apps to turn on lights, adjust the temperature, and lock doors. Every company promises you a 'seamless smart home experience,' yet somehow your house feels bulkier than before, just with more apps.

Will Circle and Stripe repeat the mistakes of the cryptocurrency realm?

Circle and Stripe

On August 2025, two major announcements were made.

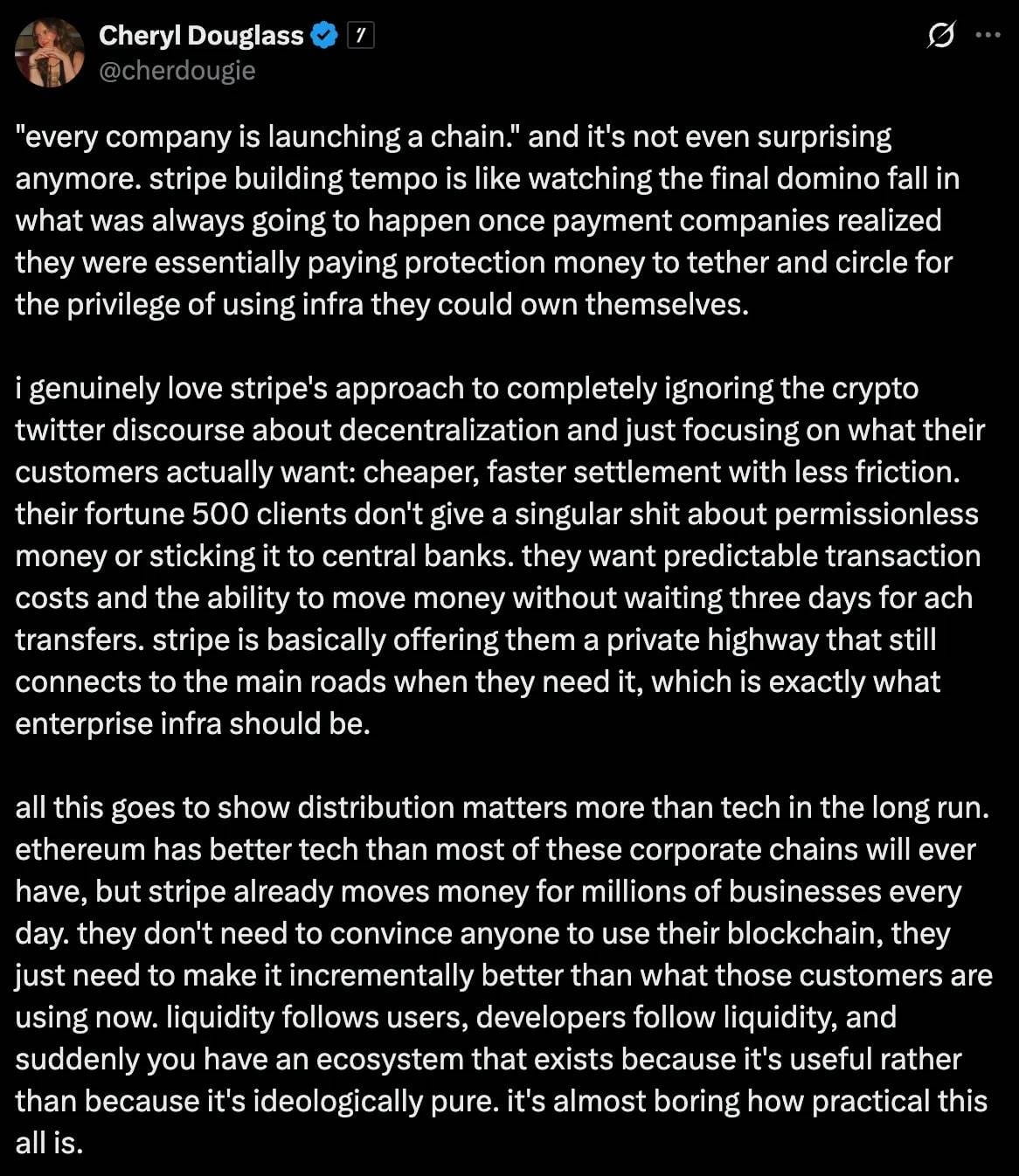

First, reports emerged that the $50 billion payment giant Stripe is collaborating with crypto venture capital firm Paradigm to develop a blockchain called Tempo that is 'high-performance, focused on payments.' A day later, Circle, the company behind the $67 billion USDC stablecoin, announced its Arc project, a Layer 1 blockchain designed for stablecoin payments, forex trading, and capital markets.

Inside Circle Arc: Circle specifically built Arc around its USDC stablecoin. Most blockchains require you to pay transaction fees with their native tokens. For example, Ethereum uses ETH, and Solana uses SOL. But on Arc, you can pay fees directly with USDC without holding volatile tokens to use the network.

Arc has a built-in foreign exchange engine. There is no need to use external services or decentralized exchanges (DEX) for currency conversion; Arc natively handles forex transactions at the protocol level. Send USDC, and the recipient will receive EURC (Euro Coin), with the conversion process automatically completed, requiring no third-party services or additional fees.

There is also privacy control. Most public blockchains (Ethereum, Bitcoin, Solana) make all information public: addresses, amounts, times. Privacy coins like Monero hide everything by default. Arc offers selective privacy, allowing institutions to hide transaction amounts while keeping addresses visible, and is built with regulatory compliance features. It is designed for businesses that need competitive privacy but not complete anonymity.

Inside Stripe Tempo: Stripe's differentiation seems to lie in the abstraction of user experience. Other crypto payment solutions still feel like using cryptocurrency—connecting wallets, signing transactions, waiting for confirmations, while Tempo seems designed to make blockchain payments feel indistinguishable from credit card payments from the user's perspective.

Being Ethereum-compatible means it can leverage existing DeFi infrastructure and developer tools, but the advantage lies in integrating with Stripe's existing merchant ecosystem. Millions of businesses using Stripe can add crypto payment functionality without changing their checkout processes or learning new systems.

Most importantly, Stripe's existing relationships with banks and regulators can resolve a major issue. Most crypto payment solutions struggle with the 'last mile'—transferring funds from the blockchain back to regular bank accounts. Stripe already has the banking partnerships that other crypto companies have spent years building.

Why am I still troubled?

Thus, we return to my digitally fragmented home, where problems begin to multiply, just like the notification badges on my various home automation applications.

What troubles me first is: where is the demand for these dedicated blockchains?

Circle and Stripe have been talking about stablecoin payments and enterprise features, but the real active area for stablecoins is DeFi. People use USDC to purchase other crypto assets, participate in lending protocols, trade on decentralized exchanges, and interact with the broader financial application ecosystem. All of this primarily takes place on Ethereum.

It's like building the most advanced smart thermostat in the world, but only able to be used in a house without any other smart devices.

Of course, this thermostat may be technically superior, but you have isolated yourself from the entire ecosystem where people really want to use smart home features.

The second question: what is the point of reinventing the wheel?

Everything Circle and Stripe are pursuing—faster transaction speeds, lower fees, custom features, enterprise branding—can be achieved through Ethereum Layer 2 solutions. You can gain the security of Ethereum's base layer, access the largest DeFi ecosystem, and be able to customize your network on demand.

Some Layer 1 blockchains have already realized this. The mobile payment-focused independent blockchain Celo announced plans to transition to Ethereum Layer 2. They did the math and found that joining the Ethereum ecosystem made more sense than building their own network effects from scratch.

The more blockchains there are, the more bridges are needed. And the bridges are the problem... they transfer assets between different blockchains. Essentially, they lock your tokens on one chain and then mint equivalent tokens on another through complex smart contracts. But bridges are often hacked. Really often. I swear by Ronin. We're not talking about the minor inconvenience of switching from the Philips Hue app to the Nest app. We're talking about potential economic loss if bridge software fails.

User experience is poor. In my smart home, the worst case is that I have to open another app to turn off the porch light. But for enterprise blockchains, users may need different wallets, different gas tokens, different interfaces, and different security settings for each network. Most people already struggle to manage one crypto wallet. Imagine explaining why they need to use different wallets for Stripe payments and Circle transfers.

But what truly confuses me is that the network effects simply do not exist.

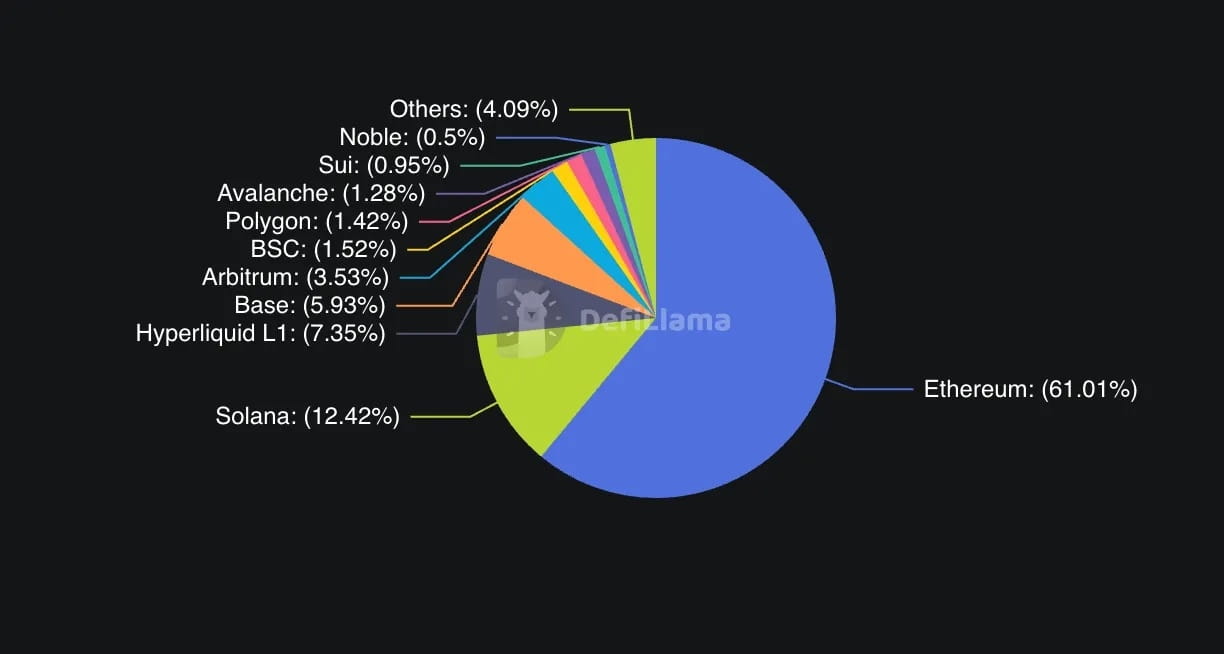

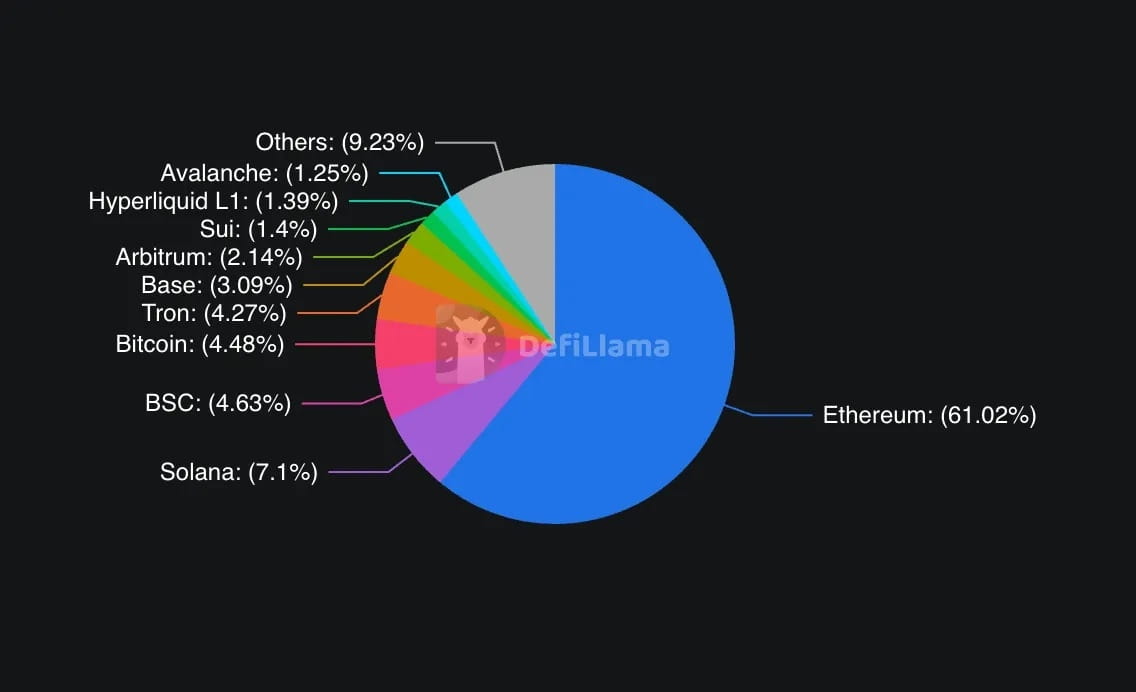

The value of payment networks grows exponentially with the number of users and applications. Ethereum has the most developers, the most applications, and the most liquidity. As of mid-2025, Ethereum's TVL (total value locked) is $96 billion, accounting for about 60-65% of DeFi activity. Solana, positioned as a high-performance alternative, has a TVL of $11 billion. Other major chains like Binance Smart Chain ($7.35 billion), Tron ($6.78 billion), and Arbitrum ($3.39 billion) share the remainder.

These enterprise chains are choosing to opt out of these network effects to build something isolated, hoping users will just come.

Would you build the perfect store on a deserted island? Sure, countries like the UAE have built cities like Dubai, and people actually went there. But that's because of geographical constraints. They had to do it.

Finally, there is a competition issue that no one wants to face directly. Are these companies really trying to build better infrastructure, or are they just unwilling to share the 'sandbox' with competitors? When I look at the smart home chaos I am in, I find that each company has reasonable technical reasons for making their choices. But the real driving force is often that they do not want to rely on someone else's platform or pay fees to competitors.

Perhaps this is the reality. Circle does not want to pay Ethereum transaction fees, and Stripe does not want to build on infrastructure they cannot control. This makes sense. But let's be candid about what this really is. It has nothing to do with innovation or user experience; it's about control and economic benefits.

The real kings seem unconcerned.

Ethereum does not seem to care much about this. The network processes over 1 million transactions daily, accounting for the majority of DeFi activity, and has recently seen massive institutional inflows through its ETF. On one day in August, net inflows into Ethereum ETFs reached $1 billion, exceeding the total of Bitcoin ETFs over the past week.

The Ethereum community's reaction to these enterprise chains is interesting. Some see it as an affirmation. After all, both Arc and Tempo are built as EVM-compatible chains, essentially adopting Ethereum's development standards.

But here lies a subtle threat. Every USDC transaction on Arc instead of Ethereum is revenue from transaction fees that does not flow to Ethereum validators. Every merchant payment on Stripe processed on Tempo rather than Ethereum Layer 2 is an activity that does not contribute to Ethereum's network effects.

Solana may feel this competition more acutely. The network is positioned as a high-performance alternative to Ethereum, particularly in payments and consumer applications. When major payment companies choose to build their own chains instead of adopting Solana, it undermines Solana's argument that 'everything can run on a single fast computer.'

The graveyard of enterprise blockchains

History has not been kind to companies attempting to build their own blockchains. As I mentioned earlier, Celo made the same move in 2023.

Remember Facebook's Libra? It started as an ambitious plan to create a global digital currency, then became Diem, only to become unsustainable under regulatory pressure, ultimately being dismantled and sold off. Don't forget, under today's clearer rules, the GENIUS Act explicitly states how stablecoin issuers can operate, which means Facebook's project might actually succeed.

JPMorgan's blockchain attempts may provide the most relevant cautionary tale. The bank spent years developing JPM Coin (digital dollar), Quorum (their private blockchain network), and other blockchain projects. Despite having almost unlimited resources, regulatory relationships, and a vast existing customer base, these projects never gained meaningful adoption outside of JPMorgan’s own operations. JPM Coin processed billions of dollars in transactions but was primarily just for fund transfers between internal institutional clients.

Even the attempts of major payment companies are not particularly exciting. PayPal launched its own stablecoin (PYUSD) in 2023, becoming the first large fintech company in the U.S. to enter the stablecoin space. But PayPal chose to launch on existing networks like Ethereum instead of building custom infrastructure. The result? PYUSD's market cap is only $1.102 billion, insignificant compared to USDC's $67 billion, and is primarily limited to PayPal's own ecosystem.

This raises a question: if a company like PayPal, with extensive influence and payment expertise, cannot make a significant impact relying solely on a stablecoin, why do Circle and Stripe think building an entire blockchain will perform better?

This model suggests that building a successful blockchain requires more than just technical capability and financial resources. You need network effects, developer enthusiasm, and organic adoption, which are extremely difficult to manufacture even with corporate support.

Will this time be different?

We have reason to believe that Circle and Stripe may succeed while other companies struggle.

First, regulatory clarity has significantly improved. The U.S. passed the GENIUS Act, providing a clear framework for stablecoin issuers, eliminating much of the uncertainty faced by early enterprise blockchain efforts. When Circle launched Arc, they were no longer operating in a legal gray area. They are a publicly traded company operating under clear rules.

Secondly, these two companies already have what JPMorgan lacks: a vast user base that is not primarily focused on cryptocurrency. Stripe processes over $1 trillion in transactions for millions of merchants worldwide every year and has been systematically building its crypto infrastructure—acquiring Bridge (stablecoin infrastructure) and Privy (crypto wallet technology) for $1.1 billion, creating an end-to-end payment stack. Circle's USDC is integrated into hundreds of applications and trading platforms. They are not building a blockchain and hoping someone will use it; they are building the infrastructure for the users they already serve and providing tools for seamless access.

Paradigm's Matt Huang emphasized how blockchain technology can 'fade out' of ordinary users' view when describing Stripe's strategy. Imagine online payments with instant settlement, lower fees, and programmable features, but the merchant integration looks exactly like the existing Stripe checkout process. This is completely different from asking people to download MetaMask and manage seed phrases. It's a Web2 user experience combined with Web3 infrastructure. Users may not even feel any 'blockchain flavor.'

Thirdly, the technology itself has matured. When JPMorgan experimented with blockchain in 2017-2018, the infrastructure was indeed very primitive. Today, building a high-performance blockchain with institutional-grade features, while challenging, is not unprecedented. Circle acquired the Malachite consensus engine team, providing them with battle-tested sub-second finality technology. Stripe's partnership with Paradigm brings deep crypto expertise to complement its payment knowledge.

Cost dynamics have also changed dramatically. In 2017, launching a new blockchain typically required $1 million to $5 million, with development cycles lasting 1-2 years or longer. By 2025, the average cost of launching a functional blockchain application is expected to be $40,000 to $200,000, usually taking 3-6 months, thanks to improved developer tools, consensus engines, and blockchain-as-a-service platforms. Modern deployments can be up to 43% cheaper than centralized applications in certain areas, due to increased efficiency and infrastructure scaling.

Payment companies realize they are paying for infrastructure that they could have built themselves. Rather than paying Circle for USDC transactions or relying on Ethereum's fee structure, companies like Stripe can now build their own infrastructure stack at a long-term cost of paying a small fraction to third parties.

This is the classic 'build or buy' decision, and now the cost of building has dropped from millions to hundreds of thousands.

Coexistence Issues

So, where does this lead us? Are we heading towards a fragmented future where every big company runs its own blockchain, or will market forces drive integration and interoperability?

Early signs suggest that the future is more likely to be pragmatic coexistence rather than winner-takes-all competition. Circle has made it clear that Arc will complement rather than replace its multi-chain strategy. USDC will continue to operate on Ethereum, Solana, and dozens of other networks. Arc is positioned as an additional option for users needing specific features such as institutional privacy, guaranteed settlement times, or built-in forex functionality.

Stripe's strategy seems similar. Tempo is not designed to completely replace existing payment channels but rather to provide alternatives for use cases where blockchain features have clear advantages. Cross-border payments, programmable currency, and merchant settlements are areas where blockchain technology truly outperforms traditional systems.

User experience will ultimately determine whether this fragmentation becomes a feature or a problem. If 'chain abstraction' technology develops as promised, users may unknowingly use different blockchains. Your payment app might automatically route transactions through the network with the best speed and cost.

My guess (if I’m a bit optimistic) is that we will see both outcomes simultaneously, but in different market domains.

For institutional and enterprise users, multiple dedicated blockchains may thrive. A multinational company transferring $100 million between subsidiaries is concerned about compliance features, settlement guarantees, and integration with existing financial systems. They do not care about gas price fluctuations, whether their blockchain has the coolest NFT projects, or the most active DeFi protocols. A chain that allows enterprises to directly access traditional banking systems, provides built-in regulatory reporting, or guarantees settlement times will be more popular than Ethereum's general-purpose infrastructure.

Arc may indeed serve these users better than Ethereum.

Stable fees, instant settlements, and built-in compliance features may be more important to CFOs than accessing the latest DeFi protocols.

For retail and developers, network effects remain crucial. The blockchain with the most applications, the most liquidity, and the most developer activity will continue to attract more of the same. Today, this is still Ethereum, and these enterprise chains do not seem to directly challenge that dominance.

One variable is whether these enterprise blockchains will remain enterprise-focused. If Stripe provides merchants with faster, cheaper payment options, and customers do not realize they are using blockchain, it could potentially extend beyond the realm of enterprise applications.

But the key to infrastructure is: the best kind is invisible. When you flip the light switch, you do not think about the power plant or the transmission lines. When these blockchain experiments succeed, it will be because they make the underlying technology completely disappear.

Whether this will actually happen remains to be seen. Right now, we are in a phase of territorial disputes, with everyone wanting a piece of the future financial infrastructure.