Source: arca; Translation: Golden Finance

The race for control over the value of cryptocurrencies has officially begun. If you think the Layer 1 competition is cooling down, you are mistaken. The latest participants are the world's largest fintech and stablecoin companies.

Last week, Stripe announced the launch of Tempo, an EVM-compatible blockchain designed for stablecoin payments and enterprise applications. The goal of Tempo is to build a blockchain optimized for cross-border settlements that Stripe can fully control. Previously, Stripe acquired Bridge (stablecoin infrastructure) and Privy (crypto wallet), indicating its intention to control the full stack from payments to rails to wallets.

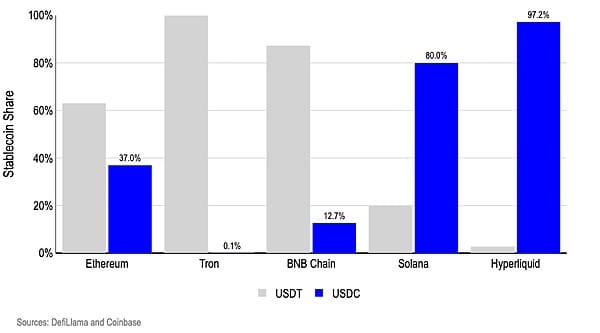

Following Stripe, USDC issuer Circle launched Arc, its own EVM-compatible L1 chain. Arc is designed entirely around stablecoins, using USDC as the gas token, providing optional privacy features and a built-in foreign exchange engine. Circle's validator set will be permissioned, further emphasizing that it is not about decentralization; rather, it relates to efficiency, compliance, and margin acquisition. Arc is expected to go live on the mainnet in 2026, but Circle's intent is already clear: it no longer wants to be a guest in someone else's ecosystem. It wants to own the home. This could hurt Solana more than Ethereum, as Solana's stablecoin base is primarily USDC (about 80% USDC / about 20% USDT), while Ethereum's stablecoin base is primarily USDT (about 37% USDC / about 63% USDT).

Earlier this year, Tether and Bitfinex announced the launch of Plasma, their own blockchain initiative aimed at building settlement and financial infrastructure. While specific details are yet to be determined, its positioning echoes the same theme: if you can control the rules, fees, and transaction processes independently, why rely on external chains? For Tether, which already dominates the stablecoin issuance sector, Plasma is a logical extension of its business empire, as it not only issues stablecoins but also operates its underlying systems. For Bitfinex, Plasma further solidifies the vertical integration between the exchange, token issuance, and infrastructure.

As we recently stated, it is almost impossible to value a layer 1 blockchain. That said, we clearly state that these blockchains do have value; we just cannot determine exactly how much they are worth. But almost everyone recognizes that infrastructure is the most profitable part of cryptocurrency. Simply being an application on someone else's chain is no longer enough — the real attraction lies in owning the chain itself.

It is worth remembering that none of this is new. Cosmos (ATOM) has been promoting 'sovereign blockchains' since 2017, launching the Cosmos SDK and Tendermint consensus engine. Their promotion is exactly what Stripe, Circle, and Tether are currently chasing — building dedicated blockchains based on your application without renting block space on Ethereum or other blockchains. Cosmos achieves modularity by providing plug-and-play components (consensus, governance, staking), while allowing projects to customize fees, tokens, and execution environments.

Some of the earliest vertically integrated projects in the cryptocurrency space originated from the Cosmos ecosystem. Binance Chain, dYdX's new chain Osmosis, and dozens of application chains were built using the Cosmos SDK. These projects are not designed to compete for block space; they aim to become ecosystems with autonomy, capturing more value from users, sorting fees, and governance. Cosmos's vision is that every company will eventually own its own Layer 1, which is precisely the transformation we see Stripe, Circle, and Coinbase pursuing today.

In many ways, Cosmos is ahead of its time. The current wave of enterprise L1 and application chains precisely validates Cosmos's argument: customization and sovereignty are the ultimate goals. The question is whether the companies building projects like Tempo, Arc, and Plasma can successfully launch applications.

But not everyone is building their own chain. There are also some notable counterexamples. Despite its strong vertical integration capabilities, Coinbase has thoughtfully decided to build Base as an Ethereum Layer 2 rather than a new Layer 1. They believe it is more important to align with Ethereum's liquidity, developer ecosystem, and credibility than to start from scratch. Similarly, Robinhood has chosen to build a new chain on Arbitrum Orbit to speed up its go-to-market pace. These two decisions reflect a trade-off — giving up some control and theoretical long-term value capture, but gaining faster deployment speed, credibility, and network effects.

However, it is worth noting that Coinbase's goal remains to have a complete vertical stack. For example, during Coinbase's second-quarter earnings call, Brian Armstrong explained how Coinbase integrates decentralized exchanges (such as Aerodrome - AERO). Aerodrome will also become the decentralized exchange (DEX) for Coinbase to achieve its goals of tokenizing stocks and other assets. The old model of Coinbase's exchange only generated trading fees at the time of trading. The new model will allow Coinbase to earn from three sources: CEX trading fees, sorting fees from Base (fully owned by Coinbase), and a share of DEX fees (Coinbase Ventures is an investor in AERO).

Ironically, this cycle looks remarkably similar to Web 2.0. Just as Amazon and Apple built vertically integrated stacks to control distribution, hardware, software, and payments, cryptocurrency companies are now rushing to build their own sovereign layers. Some companies will succeed, but most will underestimate the difficulty of driving actual usage outside their exclusive ecosystems.

Whether it’s the collaboration between Stripe and Tempo, Circle and Arc, or Coinbase and Base and Aerodrome, the common theme is clear — everyone wants to move up (or down) the tech stack to maximize profits. But history tells us that network effects are stubborn, and developing in isolation rarely outperforms developing where users already exist. Each collaboration between Tempo and Arc will be accompanied by dozens of failures. The ultimate winners will be those who strike the right balance between control and ecosystem coordination.