Written by: imToken

Have you seen 12% annualized demand deposit yields for USDC on certain platforms recently?

This is not just a gimmick. In the past, stablecoin holders were often zero-interest 'non-interest depositors', while issuers invested the deposited funds in U.S. Treasuries, notes, and other safe assets to earn huge profits, as seen with USDT/Tether and USDC/Circle.

And now, the exclusive dividends that once belonged to issuers are being redistributed—beyond the interest subsidy battle of USDC, more and more new generation yield-bearing stablecoin projects are breaking this 'yield wall', allowing holders to directly share the interest income from underlying assets. This not only changes the value logic of stablecoins but could also become a new growth engine for RWA and Web3.

One, what are yield-bearing stablecoins?

By definition, yield-bearing stablecoins are those whose underlying assets can generate yield and directly distribute that yield (usually from U.S. Treasuries, RWA, or on-chain yields) to token holders, which is significantly different from traditional stablecoins (like USDT/USDC), as their earnings belong to the issuer, and holders only enjoy the benefits of being pegged to the U.S. dollar without interest income.

Yield-bearing stablecoins turn holding itself into a passive investment tool. The reason behind this is that they distribute the Treasury interest income, which was previously monopolized by Tether/USDT, to the broad base of stablecoin holders. An example may help to understand this more intuitively:

For example, the process by which Tether issues USDT essentially involves crypto users using U.S. dollars to 'purchase' USDT—when Tether issues $10 billion of USDT, it means that crypto users have deposited $10 billion with Tether to obtain this $10 billion of USDT.

After obtaining this $10 billion, Tether does not need to pay interest to the corresponding users, effectively acquiring real U.S. dollar funds from crypto users at zero cost. If it buys U.S. Treasuries, it becomes a zero-cost, risk-free interest income.

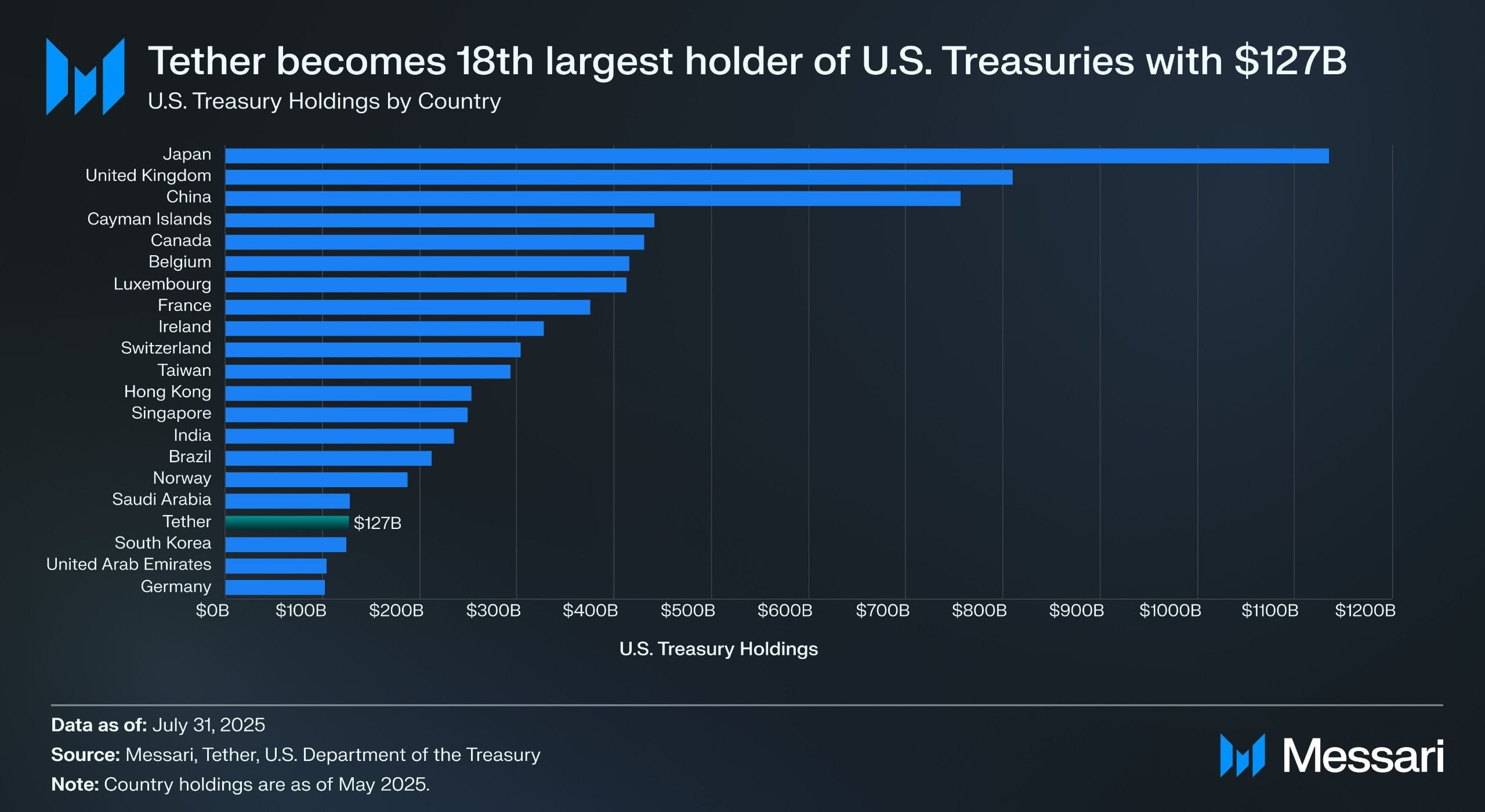

Source: Messari

According to Tether's disclosed second-quarter attestation report, it holds over $157 billion in U.S. government bonds (including $105.5 billion directly held and $21.3 billion indirectly held), making it one of the largest holders of U.S. Treasuries in the world. According to Messari data, by July 31, 2025, Tether surpassed South Korea to become the 18th largest holder of U.S. Treasuries.

This means that even with a Treasury yield of around 4%, Tether can earn approximately $6 billion annually (about $700 million per quarter). Tether's operational profit of $4.9 billion in the second quarter also corroborates the profitability of this model.

Based on market practices, imToken divides stablecoins into several exploratory subsets, believing that 'stablecoins are no longer a tool that can be summarized by a unified narrative; their usage varies from person to person and depends on needs' (Extended Reading: Stablecoin Worldview: How to Build a Classification Framework for Stablecoins from the User Perspective?).

According to imToken's classification method for stablecoins, yield-bearing stablecoins are classified as a special subcategory that can bring continuous returns to holders, primarily including two major categories:

Native interest-bearing stablecoins: Users only need to hold these stablecoins to automatically generate income, similar to a bank's demand deposit. The tokens themselves are a type of yield-generating asset, similar to USDe, USDS, etc.;

Stablecoins that provide official yield mechanisms: These stablecoins may not automatically generate yield, but their issuers or management protocols provide official channels for earning yield. Users must perform specific actions, such as depositing them in designated savings protocols (like the DAI deposit rate mechanism DSR), staking them, or exchanging them for specific yield certificates to start earning interest, similar to DAI, etc.;

If 2020-2024 is the 'expansion period for stablecoins', then 2025 will be the 'dividend period for stablecoins'. Balancing compliance, yield, and liquidity, yield-bearing stablecoins may become the next trillion-dollar category of stablecoins.

Source: imToken Web (web.token.im) yield-bearing stablecoins

Two, a review of leading yield-bearing stablecoin projects

From a practical perspective, most yield-bearing stablecoins are closely related to the tokenization of U.S. Treasuries—on-chain tokens held by users essentially anchor to U.S. Treasury assets held by custodians, preserving the low-risk attributes and yield capabilities of government bonds while also possessing the high liquidity of on-chain assets, allowing for integration with DeFi components to derive financial plays like leverage and lending.

In the current market, apart from established protocols like MakerDAO and Frax Finance continuing to double down, new players like Ethena (USDe) and Ondo Finance are rapidly accelerating development, forming a diversified pattern from protocol-based to hybrid CeDeFi types.

USDe from Ethena

As the traffic representative of this wave of yield-bearing stablecoins, first and foremost is Ethena's stablecoin USDe, which recently saw its supply first exceed the $10 billion mark.

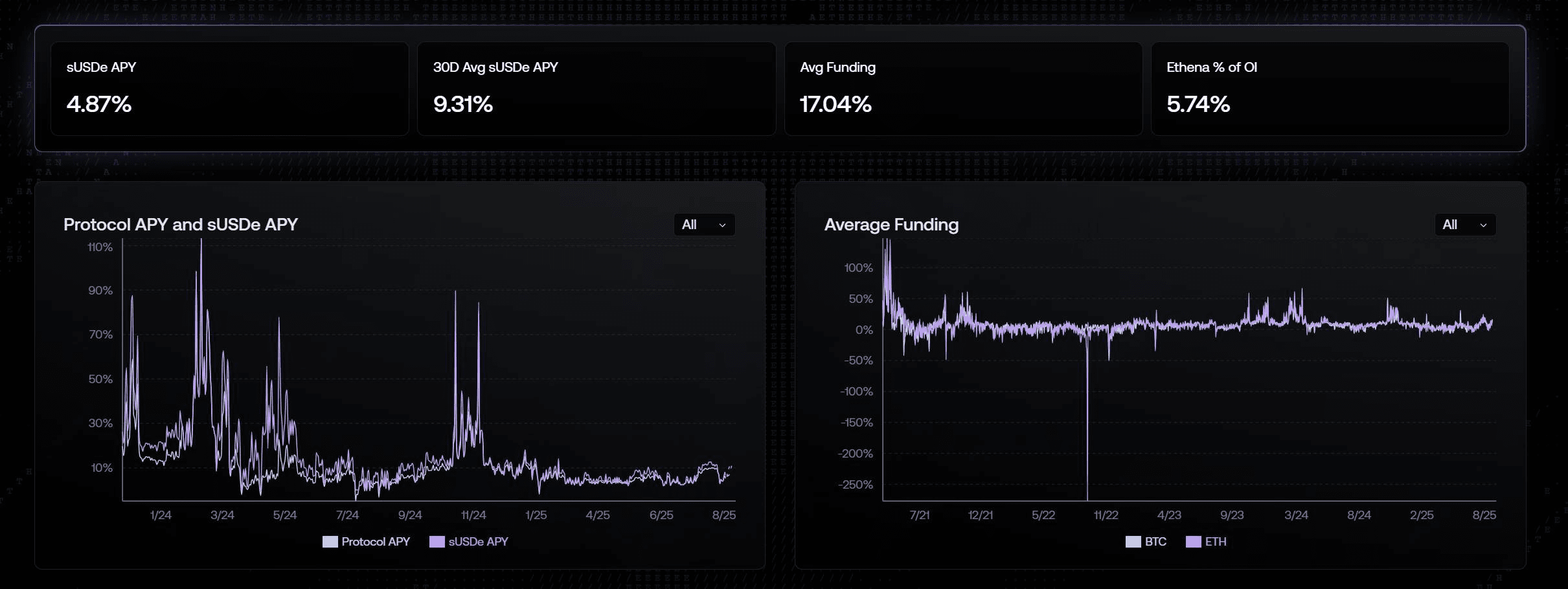

Data from Ethena Labs shows that as of the time of publication, the annualized yield of USDe remains as high as 9.31%, previously even maintaining above 30%. The main sources of high yield are twofold:

LSD staking yields of ETH;

Funding rate income from delta hedge positions (i.e., short positions on perpetual futures);

Among these, the former is relatively stable, currently floating around 4%, while the latter entirely depends on market sentiment. Thus, the annualized yield of USDe is somewhat directly dependent on the overall network funding rate (market sentiment).

Source: Ethena

Ondo Finance USDY

Ondo Finance, as a star project in the RWA sector, has consistently focused on bringing traditional fixed-income products into the on-chain market.

Its launched USD Yield (USDY) is a tokenized note backed by short-term U.S. Treasuries and bank demand deposits, essentially belonging to an unregistered debt certificate, meaning holders do not need to undergo real-name verification to directly hold and enjoy the yield.

USDY essentially provides on-chain funds with a risk exposure close to that of U.S. Treasuries while endowing the tokens with composability, allowing them to combine with DeFi lending, staking, and other modules to amplify yields. This design makes USDY an important representation of current on-chain money market funds.

PayPal's PYUSD

PayPal's PYUSD was launched in 2023, primarily positioned as a compliant payment stablecoin, with Paxos as the custodian, pegged 1:1 to U.S. dollar deposits and short-term government bonds.

Entering 2025, PayPal began to experiment with overlaying yield distribution mechanisms on PYUSD, especially in cooperation with certain custodial banks and government bond investment accounts, attempting to return part of the underlying interest income (from U.S. Treasuries and cash equivalents) to token holders, trying to bridge the dual attributes of payment and yield.

MakerDAO's EDSR/USDS

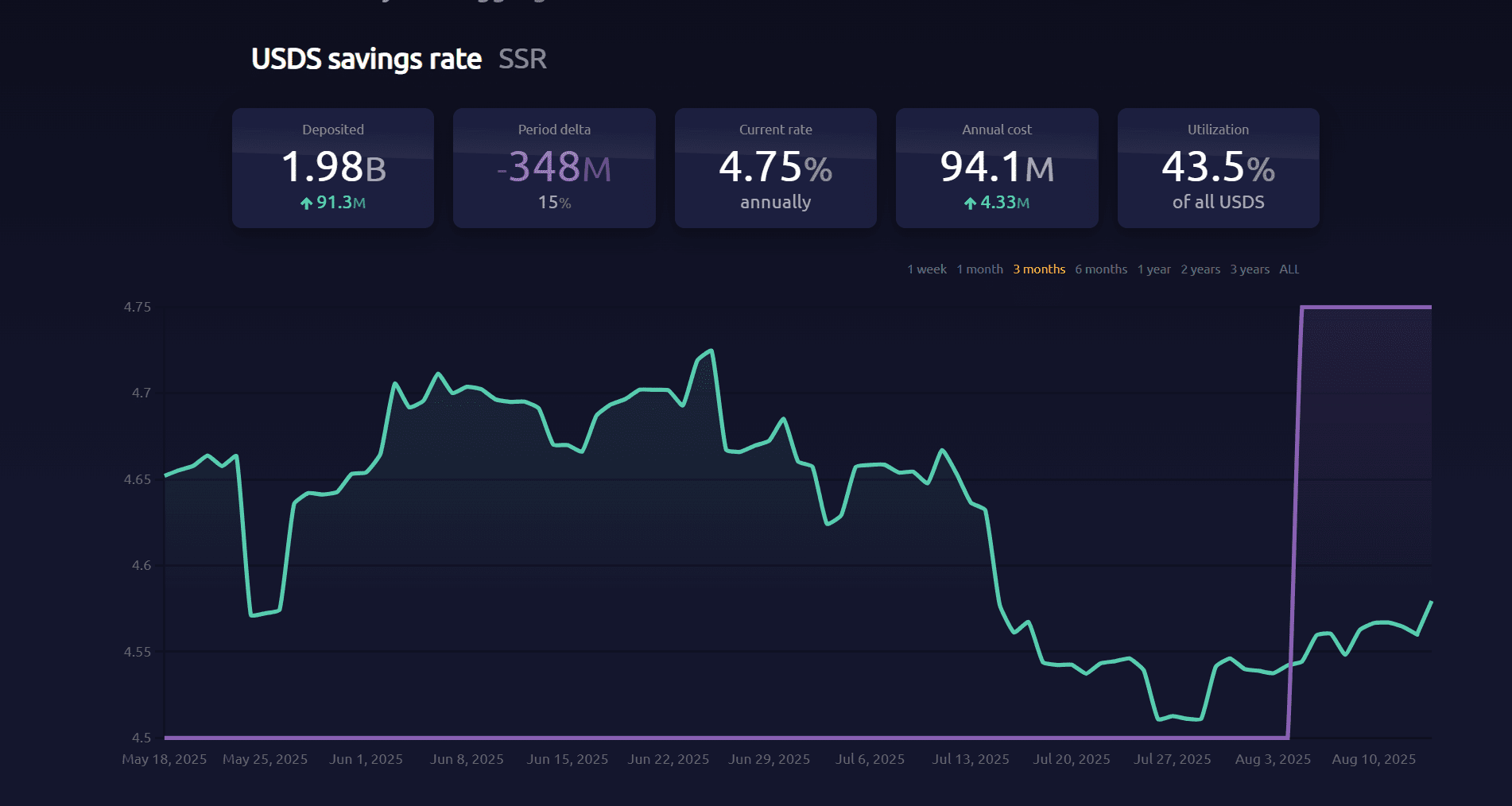

The dominance of MakerDAO in the decentralized stablecoin space goes without saying. Its launched USDS (an upgraded version of the DAI deposit interest rate mechanism) allows users to directly deposit tokens into the protocol, automatically earning interest linked to U.S. Treasury yields without incurring additional operational costs.

Currently, the savings rate (SSR) is 4.75%, with a deposit scale nearing 2 billion tokens. Objectively speaking, the rebranding event also reflects MakerDAO's repositioning of its brand and business form—from a DeFi-native stablecoin to an RWA yield distribution platform.

Source: makerburn

sFRAX from Frax Finance

Frax Finance has been one of the most proactive DeFi projects in aligning with the Federal Reserve, including applying for a main account with the Fed (which allows for holding U.S. dollars and trading directly with the Fed). Its launched staking vault sFRAX, utilizing U.S. Treasury yields, can track the Fed's interest rates to maintain relevance by opening a brokerage account to purchase U.S. Treasuries in partnership with Lead Bank in Kansas City.

As of the time of publication, the total amount staked in sFRAX has surpassed 60 million tokens, and the current annualized interest rate is about 4.8%.

Source: Frax Finance

In addition, it is worth noting that not all yield-bearing stablecoins can operate stably. For instance, the USDM project has announced its liquidation, and its minting function has been permanently disabled, retaining only limited-time primary market redemptions.

Overall, the current underlying configuration of most yield-bearing stablecoins is concentrated in short-term government bonds and reverse repos, with the interest rates offered often in the 4%-5% range, which aligns with the current U.S. Treasury yield levels. As more CeFi institutions, compliant custodial platforms, and DeFi protocols enter this space, this type of asset is expected to gain an increasingly important share in the stablecoin market.

Three, how to view the yield enhancement of stablecoins?

As mentioned above, the reason yield-bearing stablecoins can provide sustainable interest returns lies in the robust configuration of underlying assets. After all, the revenue sources of most such stablecoins are extremely low-risk, stable-return assets like U.S. Treasuries and other RWA.

From a risk structure perspective, holding U.S. Treasuries bears almost the same risk as holding U.S. dollars, but Treasuries additionally generate annualized interest of 4% or even higher. Therefore, during periods of high U.S. Treasury rates, these protocols generate income by investing in these assets, deducting operational costs, and distributing part of the interest to token holders, forming a perfect 'U.S. Treasury interest—stablecoin promotion' closed loop.

Holders only need to hold stablecoins as proof to receive the 'interest income' from underlying financial assets, while the yields on current U.S. short- to medium-term government bonds are close to or exceed 4%. Therefore, the interest rates of most fixed-income projects supported by U.S. Treasuries are also mostly in the 4%-5% range.

Objectively speaking, this model of 'holding generates interest' is inherently attractive. Ordinary users can let idle funds automatically generate interest, and DeFi protocols can use it as high-quality collateral to further derive financial products such as lending, leverage, and perpetuals. Institutional funds can enter the blockchain under compliant and transparent structures, reducing operational and compliance costs.

Therefore, yield-bearing stablecoins are likely to become one of the most comprehensible and realizable application forms in the RWA sector. Because of this, current RWA fixed-income products based on U.S. Treasuries and stablecoins are emerging rapidly in the crypto market, from on-chain native protocols to payment giants to new players with Wall Street backgrounds, and the competitive landscape is beginning to take shape.

Regardless of how U.S. Treasury rates change in the future, this wave of yield-bearing stablecoins driven by the high-interest cycle has already shifted the value logic of stablecoins from 'anchoring' to 'dividend distribution'.

In the future, perhaps when we look back at this time point, we will find it not only marks a watershed in the narrative of stablecoins but also represents another historical turning point in the integration of crypto and traditional finance.