Brothers, this project is indeed promising.

Have you ever experienced this: hungry in the morning, calling the delivery guy to check, 'Is my pancake ready yet?' The slow pace is worse than your mom cooking? This is like traditional loan approval, which can take days or even weeks to disburse. And takeaway can't wait.

Huma Finance's PayFi is like installing 'express delivery' in the loan industry: funds arrive in seconds, stable access to money, no more waiting with an empty stomach for approval—apply for a loan in the morning, receive it in the afternoon, and seamlessly handle takeaway orders.

What is Huma Finance? The ancestor of PayFi, do you understand?

In simple terms, Huma is a pioneer of PayFi (Payment Finance)—bringing traditional finance's 'credit-based loans' model into DeFi. You just need to upload your future income, invoices, pay slips, etc., to the blockchain, and you can immediately receive USDT or USDC without waiting for approval like in traditional banks. Bills serve as collateral, which is very efficient.

It supports retail users and institutional operations, and has a permissions version called Huma Institutional, combining aspects of an intermediary and a self-service bank.

What is the HUMA token? Remember this name, we can still peak later.

HUMA is the 'universal token' in this ecosystem—serving as both a ticket and a candy dispenser. Its design is quite unique:

The total supply is fixed at 10 billion, preventing unscrupulous coin printing.

50% of the protocol fees are used to buy back and burn HUMA—when you borrow and pay fees, the protocol takes back half and burns HUMA, automatically controlling inflation, making it even more valuable.

The initial circulation of the token is only 17.3%; the lock-up mechanism is rigorous, releasing to users and LPs in a structured manner rather than all at once.

Operating process: let me give you a cheeky metaphor.

You go to the 'online bank' to submit a future income proof, like an invoice for a trade order.

After the smart contract audit, funds are instantly transferred to you, whether it's USDT or USDC, it's your choice.

At the same time, keep your privileges (HUMA) as rewards—LP, voting rights, etc. all rely on it.

When you repay a loan, a portion of the fees will be repurchased and burned by the protocol, reducing the supply of HUMA, naturally increasing price pressure.

You can think of Huma as a 'future income instant arrival tool', 'DeFi + real economy + express', with a bit of 'PayPal + St Nicholas' flavor—giving you speed, stability, and a Christmas bonus (HUMA rewards).

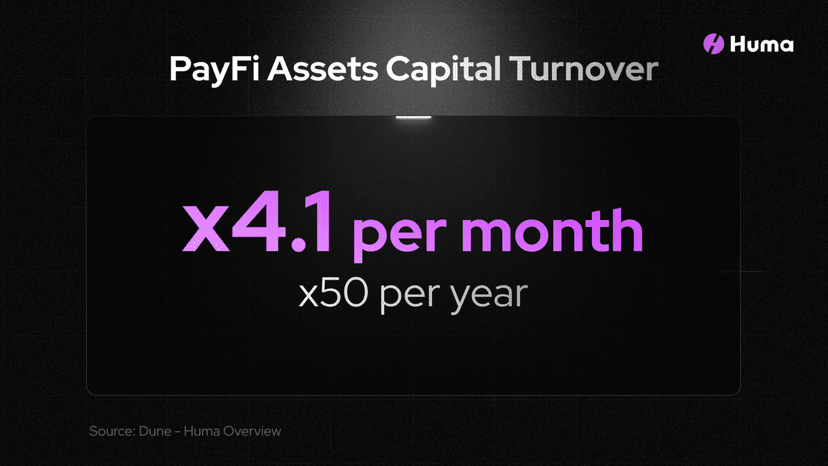

Real hardcore data backing.

The project has processed over $4 billion in on-chain transaction volume, and there have been no reports of bad debts or bankruptcies, quite stable.

The team behind it has a strong background: backed by the Solana Foundation, Circle, Galaxy Digital, Stellar Foundation, and VCs have also joined.

Cooperation is thriving: partnering with Visa, Arf, GeoSwift to enable 'same-day settlement' functionality, allowing cross-border sellers to receive payments on the same day, better than nothing.

Tokenomics & distribution—there's a plan behind it, don't think it's a 'printing machine'.

According to official disclosures:

Total supply of 10B HUMA, of which about 1.73B (17.3%) is already in circulation.

Airdrop rewards account for 5%, used for Season 1; Season 2 is also in planning.

Distribution details also include: liquidity incentives, team rewards, marketing, development funds, etc., with strict lock-up, beneficial for long-term healthy development.

HUMA price performance: soaring or crashing? Did the roller coaster not tell you?

As of August 2025, HUMA's price fluctuates between $0.033 and $0.036, with a market cap of around $58M, not much volatility, but the increase hasn't taken off yet, with future prospects.

It's like when you bought the 'Pokémon' cartridge from your childhood tape recorder; when you first got it, it was a small creature, but whether it can evolve into a 'god card' in the future depends on how you nurture it. Huma is still in its nurturing stage, but this sector is large, and it's uncertain who will nurture it well.

Advantages + be careful of pitfalls, don't just hype without mentioning risks.

Advantages:

Instant arrival, it's fierce: traditional financing is on a weekly basis, Huma PayFi settles in seconds.

Various asset collateral methods: not just crypto, but also invoices, salaries, etc. as collateral.

There is a buyback mechanism, and deflation expectations are clear.

The team and investment institutions have strong backgrounds; don't underestimate this 'golden spoon' existence.

Multiple access paths: ordinary people, businesses, and sellers can all use it, strong utility.

Potential risks:

RWA (real-world assets) on-chain is a fresh play; legal policies and compliance risks cannot be ignored.

There are many competitors, like Centrifuge, Maple, Goldfinch; this sector is attractive but very competitive.

Airdrops are not that significant, user growth may be slow, and community voices are hard to raise.

HUMA price still has short-term volatility risks; capital management must be cautious.

Huma has opened a 'fast lane' for DeFi!

Overall, Huma Finance feels like installing a 'teleportation engine' in traditional loans: funds arrive instantly, low thresholds, transparency, and community governance, plus the fees help burn HUMA, making it more valuable. Want to buy groceries with a card? Or settle sales immediately? Huma has you covered.

If you are a Dev, seller, financial enthusiast, DeFi fan, or you often complain about slow loans, Huma is definitely worth you 'keeping a VIP card' in your blockchain wallet. Let's watch how it can create a new ecosystem of 'payment + financing' together.

@Huma Finance 🟣 #HumaFinance $HUMA