Source: M31 Ventures; Compilation: Jinse Finance

M31 Ventures recently published a 95-page research report on Chainlink. The report argues that the LINK token represents one of the best risk/reward investment opportunities they have seen.

The following are the main contents of the research report:

The LINK token represents one of the best risk/reward investment opportunities we have seen:

1. A major beneficiary of the $30 trillion long-term trend; 2. Complete monopoly in the on-chain financial middleware space; 3. An undervalued asset with a severely misunderstood narrative; 4. Recent catalysts that could change market narratives; 5. A realistically reasonable upside of 20-30 times; (objectively less capable) comparable tokens trading at a premium of up to 15 times.

1. A major beneficiary of the $30 trillion long-term trend

The global financial system is undergoing a structural shift towards tokenization: digitizing real-world assets, payments, and market infrastructure onto blockchain rails. Industry forecasts indicate that by the end of 2030, there will be trillions of dollars in assets tokenized, covering government bonds, real estate, funds, commodities, and currencies. This transformation requires a secure, standardized, and compliant infrastructure layer to connect traditional finance (TradFi) with the emerging on-chain economy.

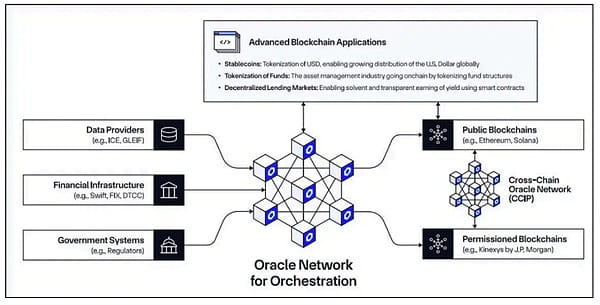

Chainlink has established its position as this infrastructure layer. As the de facto standard for on-chain data delivery and cross-chain interoperability, Chainlink secures hundreds of billions of dollars in decentralized finance (DeFi) value daily, providing mission-critical systems for the Society for Worldwide Interbank Financial Telecommunication (SWIFT), the Depository Trust & Clearing Corporation (DTCC), JPMorgan, Euroclear, Mastercard, and sovereign nation projects, and is recognized at the highest policy levels, including the (White House Digital Assets Report) (excerpt from below). Its enterprise-grade products, such as Price Feeds, Proof of Reserve (PoR), and Cross-Chain Interoperability Protocol (CCIP), have been deeply embedded in regulated pilot projects connecting traditional systems and tokenized assets.

These integrations are not just technical proofs of concept, but strategic footholds in regulated tokenized workflows. As the first infrastructure provider to solve compliance-level interoperability and asset verification issues, Chainlink has positioned itself as the default choice for institutions that cannot afford operational or reputational risk.

These integrations are not just technical proofs of concept, but strategic footholds in regulated tokenized workflows. As the first infrastructure provider to solve compliance-level interoperability and asset verification issues, Chainlink has positioned itself as the default choice for institutions that cannot afford operational or reputational risk.

2. Complete monopoly in the on-chain financial middleware space

No competitors can match Chainlink in terms of technical reliability, breadth of integrations, regulatory readiness, and institutional trust. Once integrated, it becomes critical infrastructure with high switching costs and self-reinforcing network effects.

Chainlink's recognition in Washington, its leadership in the 'American Tokenization' initiative, and its advisory role in state-level proof of reserve projects signify unprecedented trust at the policy level. Its participation in SEC working groups and central bank pilot projects positions Chainlink as a policy-aligned infrastructure partner; this is a key differentiator when institutions adopt regulated clarity.

3. An undervalued asset with a severely misunderstood narrative

For more than the past 5 years, the story of LINK has been severely misunderstood; despite its unparalleled integrations, dominant market share, and trillions of dollars in potential market, Chainlink's market cap lags significantly behind its strategic value and objectively less capable tokens. This pricing error directly stems from three prevalent misconceptions: 1) It is just a data oracle; 2) It lacks profitability; 3) Chainlink Labs (the core contributor and product company behind the Chainlink protocol) continuously sells tokens to retail investors. All three points are completely false or misleading:

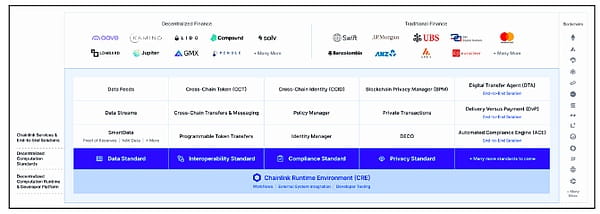

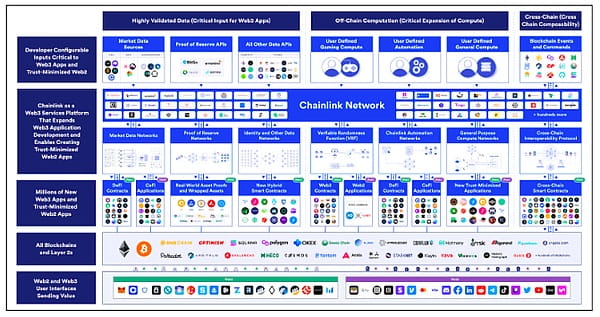

1) As mentioned above, Chainlink provides a comprehensive platform for decentralized finance and large financial institutions. Although it pioneered the blockchain oracle category when it launched in 2017, the protocol has since expanded to become the premier one-stop middleware provider, connecting the real world (data, computation, value, legal, regulation, etc.) with on-chain systems. As shown in the figure below, oracle price feeds are just one of the many products on the platform, and their share of total revenue will continue to decline in the future.

1) As mentioned above, Chainlink provides a comprehensive platform for decentralized finance and large financial institutions. Although it pioneered the blockchain oracle category when it launched in 2017, the protocol has since expanded to become the premier one-stop middleware provider, connecting the real world (data, computation, value, legal, regulation, etc.) with on-chain systems. As shown in the figure below, oracle price feeds are just one of the many products on the platform, and their share of total revenue will continue to decline in the future.

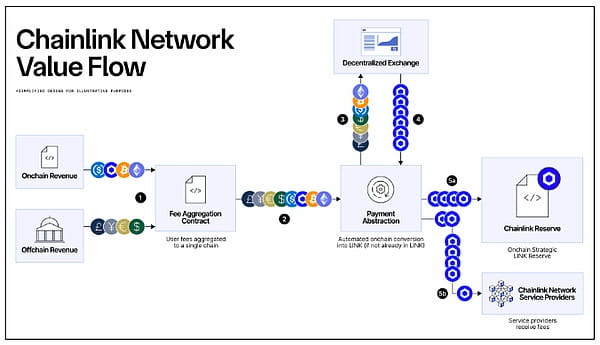

2) To some extent following Amazon's market capture strategy, Chainlink has been able to win dominant market share from the start through subsidized services. However, unlike Amazon, this is also necessary for nurturing the young Web3 industry, as most of Chainlink's clients are still seeking product-market fit (PMF) and cannot sustain payment for Chainlink's critical mission service fees. Although Chainlink has been able to win well-known clients and expand its business in both decentralized finance and traditional finance, this has never translated into substantial on-chain revenue. However, the recently launched Chainlink token reserve has completely changed this situation.

3) Chainlink Labs has not taken venture capital since 2017, instead funding its operations for its 400-500 employees through treasury token sales. This has led to the narrative of Labs 'constantly selling tokens' (although it can be argued that every other project also relies on venture capital... ultimately, someone is using cash to exchange for tokens to fund operations), deterring potential investors. Similar to the above point, Chainlink's reserves completely undermine this narrative.

4. Recent catalysts that could change market narratives

In early August, Chainlink launched a strategic token reserve, marking a significant shift in the network's token economics and triggering a 50% price surge within a week. This reserve utilizes payment abstraction technology to automatically convert on-chain (still heavily subsidized) and previously opaque off-chain enterprise revenue into LINK, creating strong and sustained buying pressure. With 'hundreds of millions' in revenue already generated from enterprise clients, this immediately shifted the narrative from 'token selling' for LINK to 'net buying'.

This also reveals the monetization scale of Chainlink in the real world. Although we are still in the early stages of a decade-long tokenization mega-trend, and Chainlink has only just begun to bring its institutional integrations into production, the platform has already generated hundreds of millions of dollars in revenue from enterprise data feeds, proof of reserve contracts, CCIP usage, and private institutional agreements.

These verifiable institutional revenues that could not be seen through on-chain analysis before have completely reversed the narrative of 'lack of profit potential' and demonstrated that Chainlink will become one of the highest-revenue protocols. As more institutional pilot projects enter production over the next 12 to 18 months, along with the inevitable 'fee switch' for on-chain services, verifiable revenue is bound to soar.

5. A realistically reasonable upside of 20-30 times; (objectively less capable) comparable tokens trading at a premium of up to 15 times

Chainlink's monetization opportunities encompass CCIP transaction fees, data feed subscriptions, proof of reserve certifications, automated services, and new enterprise-specific products. Each new integration increases usage rates and drives recurring, diversified revenue growth, making Chainlink a multi-business-line infrastructure company that grows alongside the global blockchain economy, with exponential growth expected in the coming years. With significant revenue now verifiable on-chain, we believe valuations are about to come much closer to fundamentals; the bullish case presented in this report forecasts a 38x upside for LINK by 2030.

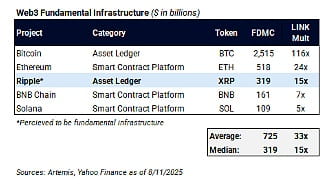

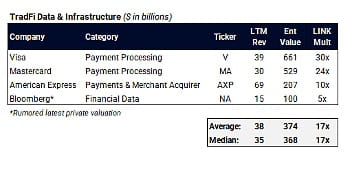

Moreover, the most comparable liquidity token to LINK is XRP; not because Ripple can actually compare with Chainlink, but because LINK possesses all the traits that XRP holders believe XRP has. In reality, XRP has no utility, no formal connection to Ripple, and has no institutional traction, yet its trading price is 15 times the premium of LINK, offering investors perhaps the most asymmetrical risk/reward opportunity in today's market. In the long term, we believe traditional financial companies like Visa and Mastercard will be more appropriate comparables, which means LINK has 20-30 times the upside potential.

This revaluation could be sudden, drastic, and sustained, as institutional capital recognizes the scale of this opportunity. Now is the time to invest.

This revaluation could be sudden, drastic, and sustained, as institutional capital recognizes the scale of this opportunity. Now is the time to invest.

Full report address: https://docsend.com/view/d9zgwzxxfbdjg7ck