The SWIFT network and Ripple's blockchain system are often positioned as separate, even competing ecosystems, for handling cross-border payments. The idea that they operate in coordination often assumes a formal partnership that does not exist.

However, a technical analysis and diagram presented by cryptocurrency researcher SMQKE (@SMQKEDQG) on X shows a technology-based method to ensure interoperability.

This connection is activated within the existing software infrastructure of financial institutions, creating an unofficial yet highly functional bridge between SWIFT's messaging standards and Ripple's modern payment capabilities.

Payment Flow From SWIFT To Ripple

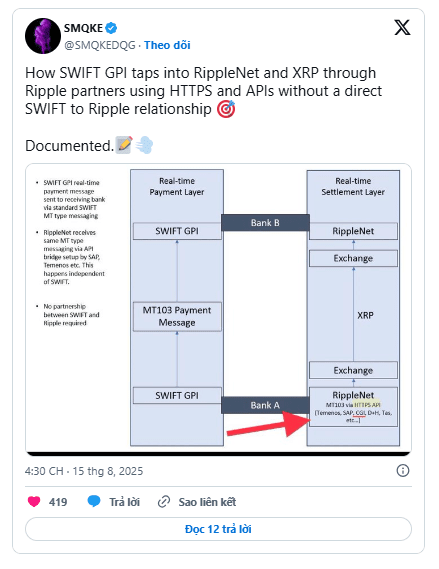

When a bank conducts a cross-border transaction using SWIFT's Global Payments Innovation (GPI) service, that bank will send a standardized payment notification in MT103 format to the receiving organization.

SWIFT GPI was introduced to enhance speed and provide comprehensive tracking. Typically, this message would be held in the correspondent banking system until the payment is made.

When the bank receiving also uses Ripple, the bank's internal system can operate as a transit point. Core banking platforms and enterprise resource planning (ERP) systems from providers such as Temenos, SAP, or CGI can be configured to analyze data from MT103 and trigger a separate workflow.

Ripple Integration Point

At this point, the workflow shifts from traditional rails to digital payments. Instead of having to go through correspondent banks, the bank's software can make secure HTTPS API calls to Ripple. This action converts the SWIFT payment order into a payment request on the Ripple platform.

This step occurs independently of SWIFT. The role of the SWIFT network ends when the GPI message reaches the bank. Next is the bank's decision to use Ripple as a payment layer, allowing the bank to maintain a familiar SWIFT interface with customers while still relying on Ripple for faster transactions.

Real-Time Payments Using XRP

When the order is entered into Ripple, the payment can be made using XRP through On-Demand Liquidity (ODL). This process removes the need for a pre-funded nostro account.

The original currency is exchanged for XRP on the digital asset platform, transferred through the XRP Ledger (XRPL) within seconds, and then converted back to local currency at the destination.

Funds are transferred to the beneficiary almost instantly. This shortens payment times from several days to just a few seconds, freeing up capital that would be stuck in the correspondent banking network.

Many experts believe that Ripple and XRP will replace SWIFT. This system could help banks transition from legacy systems to embrace the future of global finance.