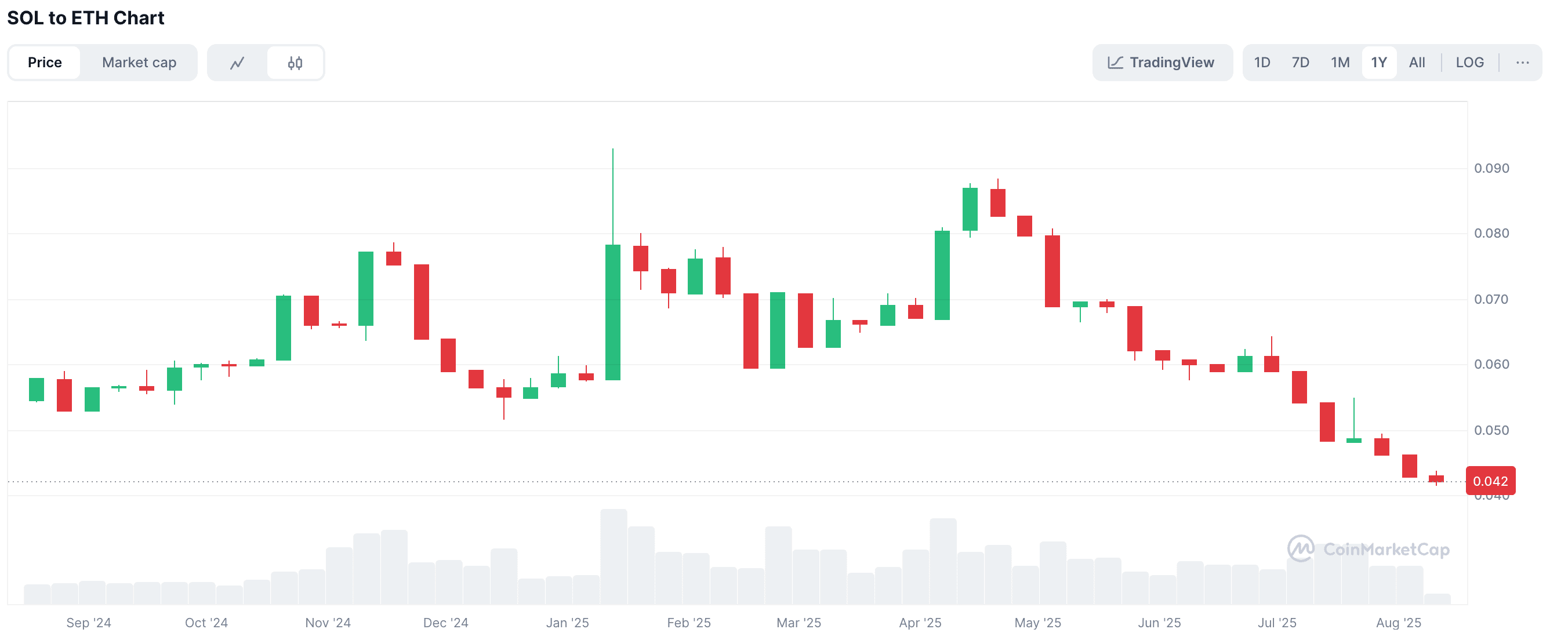

On August 13, ETH forcefully broke through $4,700, hitting a four-year high, while SOL remained weak, hovering around $200. In 2024, Pump.fun triggered a meme frenzy across the entire Solana chain, and at the beginning of the year, Trump even launched $TRUMP on it, pushing SOL's price to nearly $300, leading to a chorus of calls for 'Solana to replace ETH.'

However, the reality has given the market a sober response. Despite both ETH and SOL advancing treasury strategies simultaneously, attempting to accumulate 'bullets' for the ecosystem, their performances have diverged significantly— the SOL/ETH exchange rate has dropped from 0.09 at the beginning of the year to 0.042, with a weak pattern throughout the year. The reasons behind this may be not only price fluctuations but also a comprehensive reflection of narrative heat, ecological structure, and differences in funding expectations.

Treasury strategy: dual gap in leading figures and funding scale

On June 30, Wall Street 'contrarian bull' Tom Lee parachuted into BitMine as chairman, while ETH was still hovering around $2,500. In just a month and a half, ETH surged to $4,700, with an increase of 88%. Lee has long appeared on major financial programs like CNBC and Bloomberg, and during the significant drop in the US stock market in 2022, he reversed market pessimism with precise 'bottom-fishing' remarks. Now, this market opinion leader who comes with traffic has become the best spokesperson for ETH's treasury.

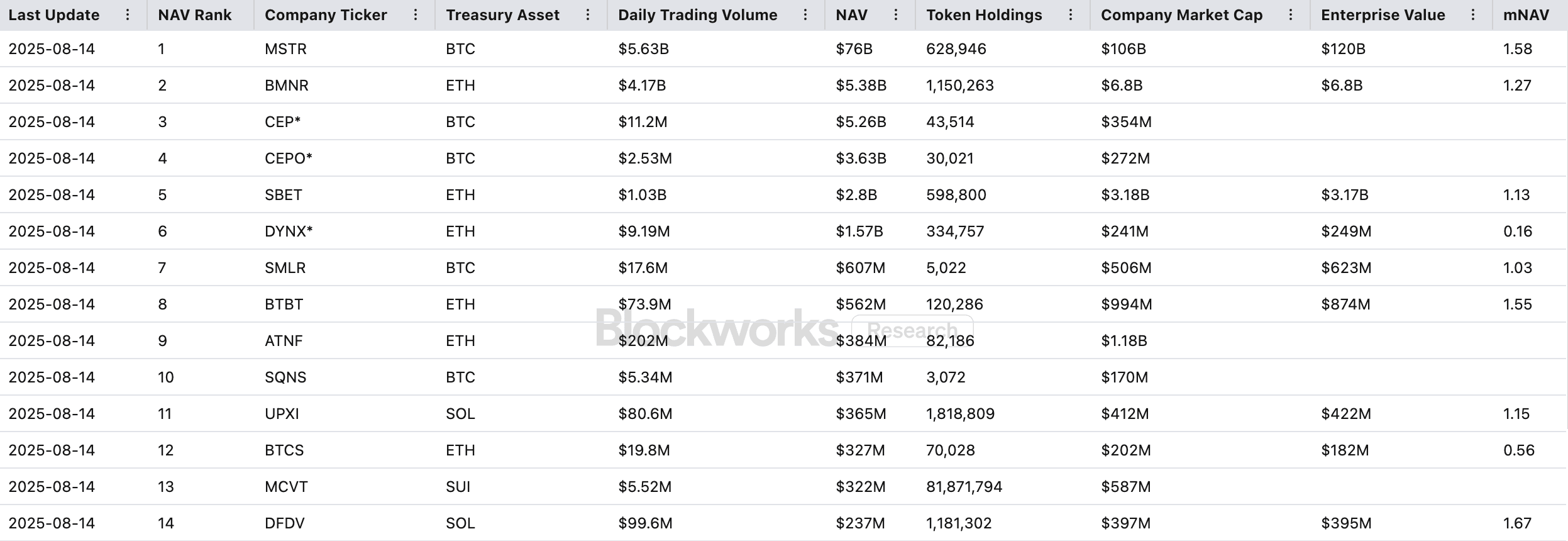

In addition, although both ETH and SOL have their respective treasury strategy companies, their scales differ greatly. In terms of holding scale, BTC and ETH treasury strategy companies occupy the top ten. The leading 'ETH Microstrategy' BitMine Immersion (BMNR) recently plans to increase its financing scale to $20 billion to increase its ETH holdings. Currently, it also has $5.3 billion in NAV (net asset value), second only to MSTR. This level of funding means it has more 'bullets' during market fluctuations and a stronger ability to shape the market. Meanwhile, the NAV of the current 'SOL Microstrategy' leader is only $365 million, ranking 11th, more than 10 times lower than BMNR. Lacking a public spokesperson with global influence like Tom Lee and not having capital firepower of the same magnitude, SOL naturally appears powerless in this round of market.

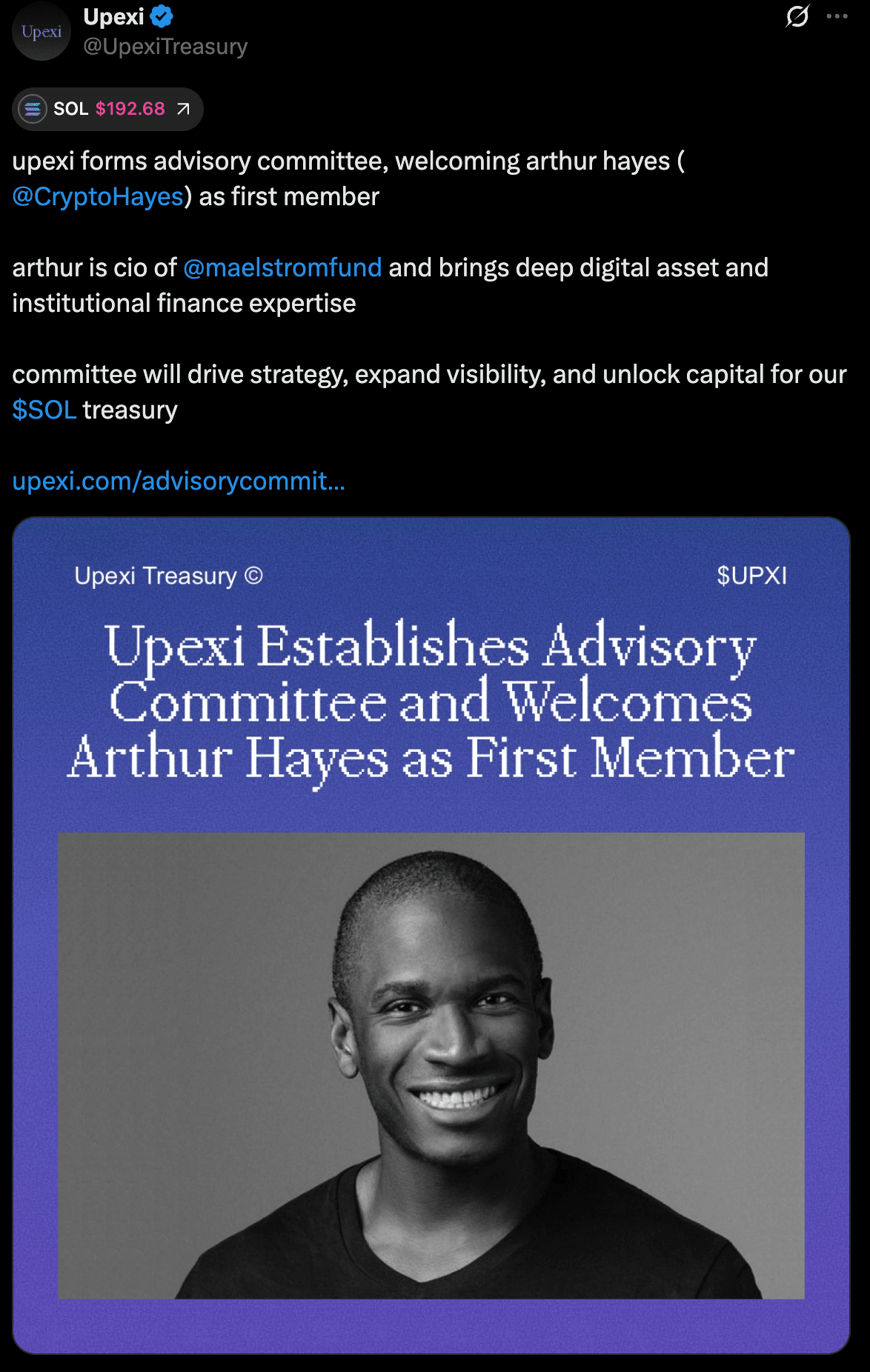

However, recent new actions from Solana are gradually compensating for this deficiency. On August 12, 'SOL Microstrategy' Upexi established a brand-new advisory committee and appointed Arthur Hayes as the first member. Hayes is the co-founder of BitMEX and a pioneer of perpetual contracts, having served as a trader at Deutsche Bank and Citigroup, and now leading the digital asset investment fund Maelstrom. He has both a traditional finance background and a deep understanding of crypto market structure, capable of providing practical guidance for institutional financing and digital asset strategies.

Upexi's strategic goal is very clear: to further expand its layout in SOL by utilizing Solana's scalability and efficiency. According to public documents, the company currently holds over 1.8 million SOL (valued at about $365 million) and will stake part of its holdings to obtain a 7%-9% return, ensuring long-term holding while creating stable cash flow. It is worth noting that the company will buy locked SOL at a discount price, thus bringing profits to shareholders. Upexi will recruit more members to join the advisory committee to provide expertise in cryptocurrency and finance.

Meanwhile, other listed companies are also increasing their SOL holdings, such as DFDV further expanding its SOL holdings, which now exceed 1 million coins; BTCM disclosed a new purchase of about 27,190 SOL and plans to convert some of its crypto assets into Solana. This institutional demand is expected to reduce circulating chips in the secondary market, thereby forming support on the supply-demand level.

ETH ETF leads, SOL ETF awaits a breakthrough

The management scale of the ETH spot ETF has exceeded $22 billion, not only validating institutions' high recognition of ETH but also rapidly establishing its absolute advantage in liquidity and market depth. Under the continuous inflow of institutional funds, BlackRock also submitted a staking application for the ETH ETF last month, which, once approved, will bring stable staking returns to holders and attract more long-term capital into the market.

In contrast, although REX-Osprey launched a Solana ETF (SSK) with a staking mechanism in July, the market heat has remained low, with net inflows being zero on most trading days, and a total inflow of only about $150 million since its listing, and it is not a standard spot ETF registered with the SEC but indirectly holds SOL through other vehicles. This structure combines a staking mechanism with offshore ETF configurations, increasing the complexity of understanding and operation, causing some institutions to remain on the sidelines; the issuer REX's influence in branding and channels is also far less than that of Wall Street giants like BlackRock and Fidelity, and it lacks endorsements from heavyweight institutions.

The market's focus is now shifting towards the SOL spot ETF applications expected to be approved in October from VanEck, Grayscale, and others. Once regulatory approval is granted, combined with the funding push from treasury strategies, if institutional investors begin to seek to diversify their allocations from BTC and ETH to other quality assets, the SOL ETF may bring new growth points to the Solana ecosystem.

The fork in application narratives

From the perspective of application narratives, ETH and Solana are currently on two completely different tracks.

Ethereum is steadily building a compliant and sustainable on-chain financial infrastructure. The explosion of stablecoins has been described by Tom Lee as the 'ChatGPT moment' in the crypto industry. Currently, the global stablecoin market cap exceeds $250 billion, with more than half of the issuance and about 30% of Gas fees occurring on the Ethereum network, which not only further solidifies ETH's core position in payment and settlement systems but also provides a continuous cash flow for staking, DeFi yields, and on-chain infrastructure.

In addition, Robinhood has issued stock tokens on the Ethereum Layer 2, and Coinbase is vigorously developing the Base chain ecosystem, all of which have brought more application scenarios to ETH. Currently, Ethereum has almost become the only main chain that can simultaneously meet regulatory adaptability, ecological maturity, and scale effects. Once ETH occupies a key node in stablecoin payments and RWA settlements, its strategic position will be prioritized by financial institutions as a 'structural subscription right.'

On the Solana side, the main narrative is more focused on meme coins and the Launchpad battle, which are 'old stories' in high-volatility tracks. Despite multiple attempts this year to enter the RWA field with the slogan 'Internet Capital Market' and supporting a series of tokens like $IBRL and Believe ecosystem, all have ended in failure. However, recently, the situation has taken a turn. On August 8, CMB International, a subsidiary of China Merchants Bank, partnered with Singapore's DigiFT and Solana's public chain service provider OnChain to tokenize a USD money market fund recognized in Hong Kong and Singapore, issuing CMBMINT on-chain, setting a benchmark for cross-border RWA compliant cooperation. On that day, the price of SOL broke through $200, and the market immediately regarded it as a potential new narrative starting point, hoping this new application scenario could open up broader institutional funding channels for Solana.

Summary

Currently, although Solana is still lagging behind ETH in key indicators such as market heat and exchange rate performance, its underlying competitiveness and potential space have not been weakened. As an 'American chain,' it naturally has a higher degree of regulatory adaptability and capital recognition. At present, ETH has gained institutional favor relying on treasury strategies, ETF booms, RWA, and stablecoin applications, but this also leaves SOL with opportunities for 'catch-up' and narrative switching.

Structurally, the expectation of the approval of spot ETFs will open new institutional funding channels for SOL. Once products from giants like VanEck and Grayscale are approved, market liquidity and trading depth may see a leap. Moreover, the cross-border landing cases of RWA have also proven that Solana's application capability on high-performance public chains is not limited to memes and Launchpads, and there is still significant room for improvement in penetration rates in fields such as DeFi, payments, and asset tokenization. The current pullback seems more like a buildup of strength rather than a curtain call.