Original author: Michael Nadeau, founder of The DeFi Report

Original text translated by: Azuma, Odaily

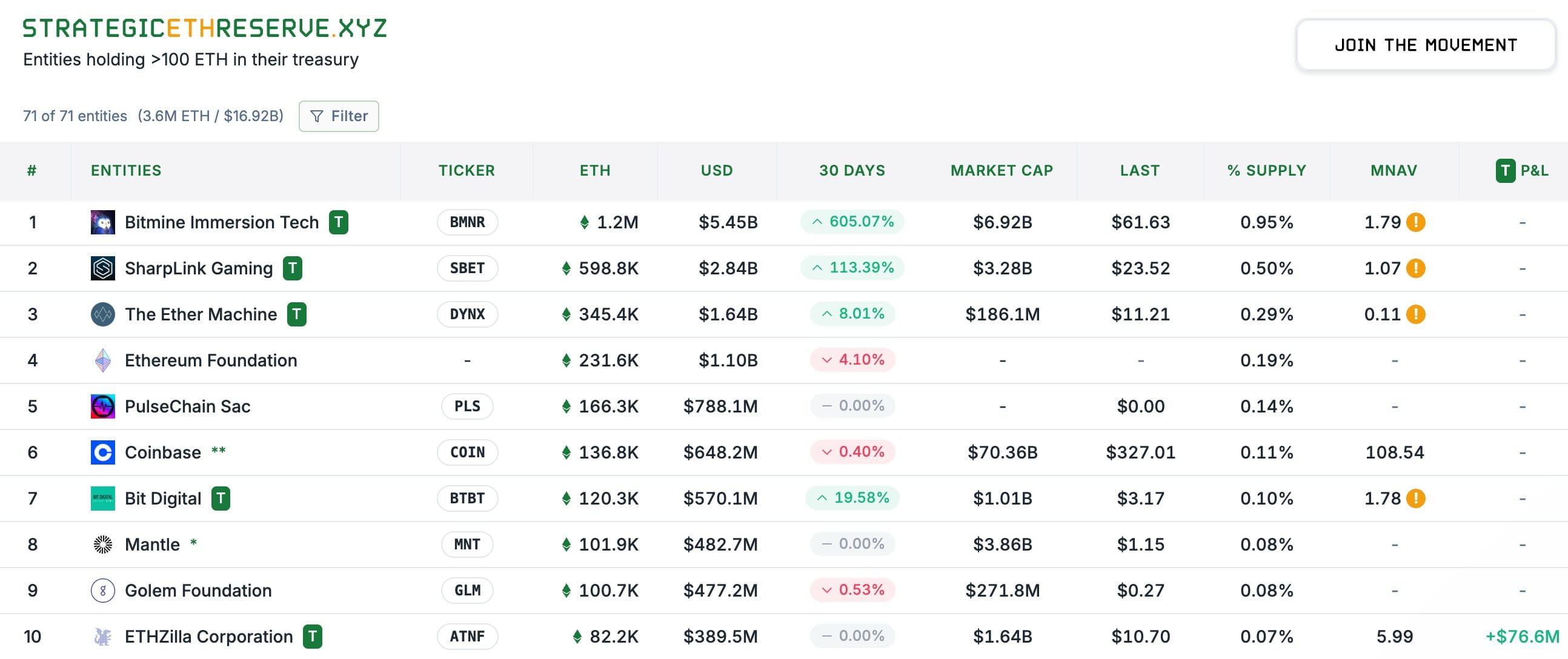

Editor's note: The mad buying spree of ETH treasury companies has become the hottest topic in the recent market, constituting the strongest 'buying impact' on ETH prices. Strategic ETH Reserve data shows that as of August 14, Beijing time, the total holdings of major ETF treasury companies have reached 3.57 million ETH, worth about $16.92 billion, with BitMine (BMNR), Sharplink Gaming (SBET), and The Ether Machine (DYNX) ranking first, second, and third with holdings of 1.2 million, 598,000, and 345,000 ETH respectively.

This morning, Michael Nadeau, founder of The DeFi Report, who has been closely monitoring ETH's status, reviewed the ETF chip distribution status and trends outside of treasury companies (note: there will be some overlap with the holdings of treasury companies), which may help you assess the future source of ETH's momentum.

The following is the original text by Michael Nadeau, translated by Odaily Planet Daily.

People often discuss the price trend of ETH, but the real key lies in its distribution pattern. Once you see the actual distribution of ETH—existing in different areas like ETFs, staking contracts, Layer 2, wrapped tokens, exchanges, etc.—you will gain insights:

· Who really has control;

· Capital flow and actual liquidity scale;

· Where might the next 'buying impact' come from;

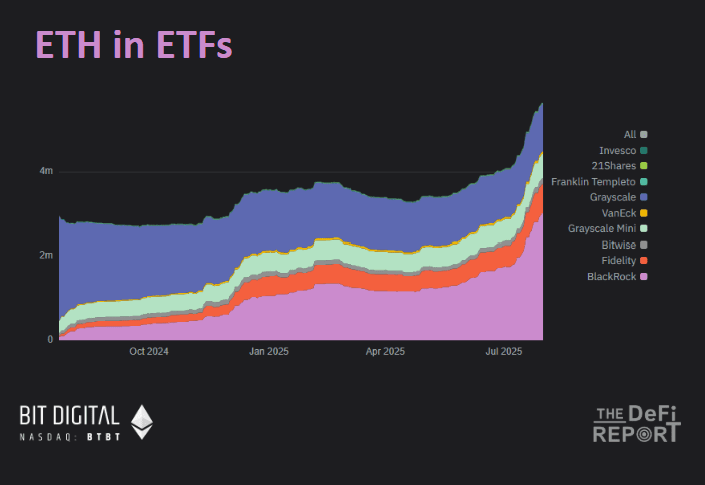

ETF Holdings

Various Ethereum ETFs currently control about 5% of the ETH supply.

In the past three months, the assets under management of ETH ETFs have increased by 80%, with BlackRock and Fidelity's ETFs accounting for 73% of the AUM.

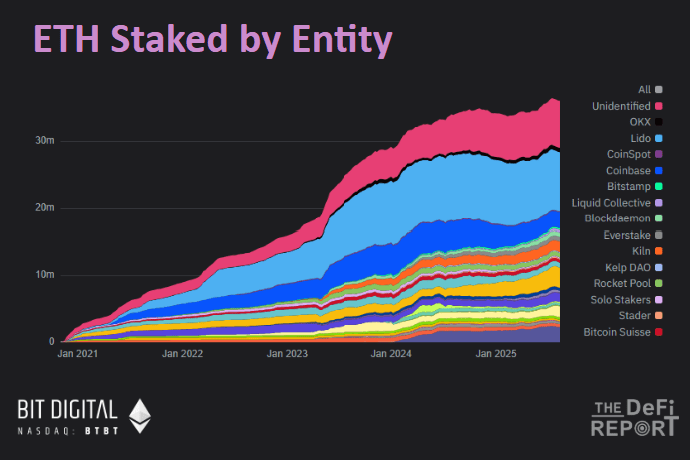

Staking

Currently, about 29.7% of ETH is in a staked state.

In the past three months, the staking scale of ETH has increased by 5%, while the market share of leading staking platform Lido has decreased by 3.5%, and Binance's staking share has increased by 23%, currently ranking second in market share.

As more and more ETH treasury companies stake ETH, we expect this number to continue to rise in the coming months.

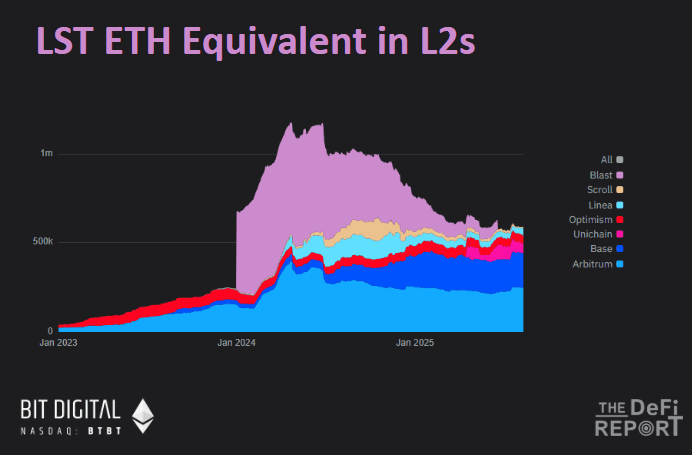

Layer 2 (including LST)

Currently, ETH in Layer 2 accounts for only 5% of the circulating supply.

More than a year ago, Blast accounted for 52% of Layer 2 ETH supply, and now it's nearly 0%—the incentive program was simply a waste of money. Currently, 41% of ETH on Layer 2 is on Arbitrum, and 33% is on Base.

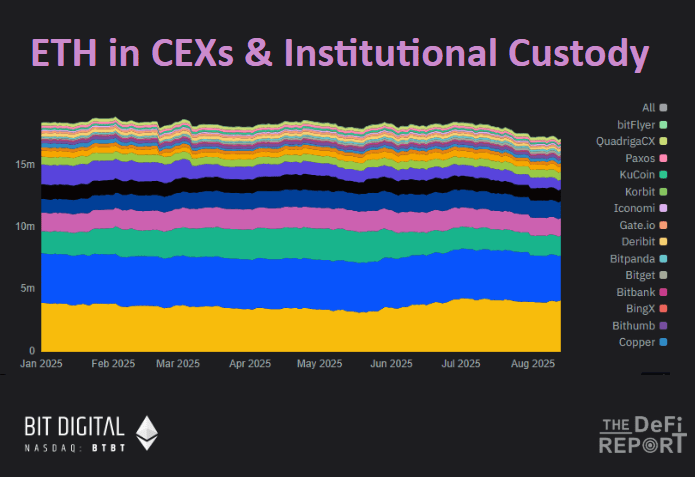

Centralized Exchanges (CEX)

Currently, the total amount of ETH in major CEXs accounts for 14% of the circulating supply.

Since the third quarter, this number has decreased by 6.7% and is currently at its lowest level since July 2016.

Where has most of this ETH gone? Most of it has entered staking contracts and cold wallets.

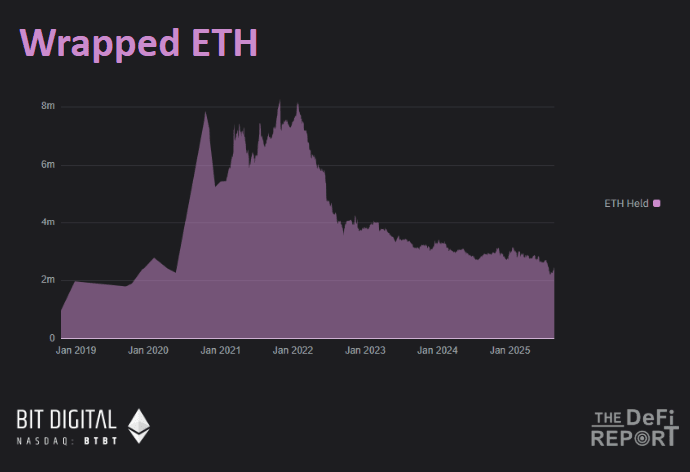

Wrapped ETH

The proportion of Wrapped ETH currently in circulation is only 1.8%.

Since the beginning of 2022, this number has dropped by 70% from its peak, and this downward trend aligns with the upward trend of ETH in staking contracts.

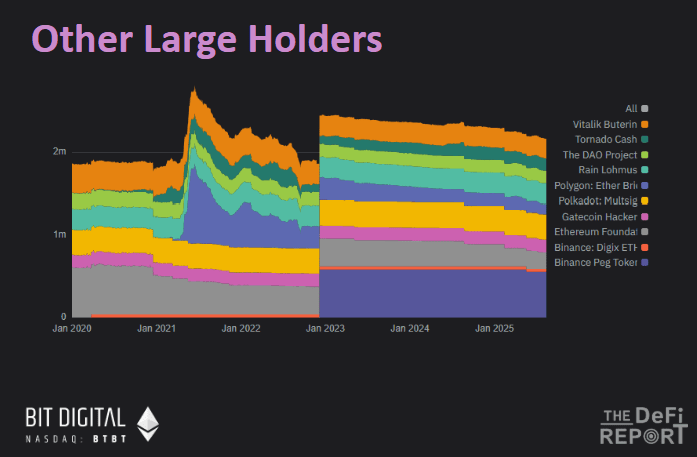

Other large holding entities and individuals

Apart from the aforementioned categories, the ETH holdings of other large entities and individuals account for approximately 1.7%.

Of this 1.7%, Binance's Binance Peg Tokens Fund accounts for about 25%, with Polygon Bridge, Tornado Cash, the Ethereum Foundation, and Vitalik himself being the main holders.

In summary, the above six charts cover about 55% of the ETH supply. Besides this, most of the remaining ETH is stored in externally owned accounts (EOA) and cold wallets.

Original link