Written by: David, Deep Tide TechFlow

On August 12, the same day that Circle released its first financial report after going public, it dropped a bombshell: Arc, an L1 blockchain specifically designed for stablecoin finance.

If you only look at the headlines, you might think this is just another ordinary public chain story.

But when you interpret it in the context of Circle's trajectory over the past seven years, you will realize:

This is not a public chain; it's a territorial declaration about the 'digital central bank'.

Traditionally, central banks have three main functions: issuing currency, managing payment and clearing systems, and formulating monetary policy.

Circle is gradually completing a digital replica—first using USDC to obtain 'minting rights', then using Arc to build the clearing system; the next step might be the formulation of digital currency policy.

This is not just about one company, but rather the redistribution of monetary power in the digital age.

Circle's central bank evolution theory

In September 2018, when Circle and Coinbase jointly launched USDC, the stablecoin market was still dominated by Tether.

Circle chose a path that seemed 'clumsy' at the time: extreme compliance.

First, it proactively faced the most stringent regulatory hurdles, becoming one of the earliest companies to obtain a New York State BitLicense. This license, known in the industry as 'the hardest crypto license to obtain globally', has an application process so complicated that many companies shy away.

Secondly, it did not choose to fight alone but partnered with Coinbase to form the Centre alliance—this not only shared regulatory risks but also provided direct access to Coinbase's vast user base, allowing USDC to stand on the shoulders of giants from the start.

Thirdly, it has achieved extreme transparency in reserves: monthly public reserve audit reports issued by accounting firms ensure 100% backed by cash and short-term U.S. Treasury bills, avoiding any commercial paper or high-risk assets. This 'straight-A student' approach was unpopular in the early days—during the wild growth period from 2018 to 2020, USDC was criticized for being 'too centralized' and growing slowly.

The turning point came in 2020.

The explosion of DeFi summer led to a surge in stablecoin demand, and more importantly, hedge funds, market makers, and payment companies began to enter the scene, revealing the compliance advantages of USDC.

From $1 billion in circulation to $42 billion, and now to $65 billion, USDC's growth curve is almost vertical.

But merely being a 'money printer' is not enough.

In March 2023, Silicon Valley Bank collapsed, and Circle had $3.3 billion in reserves at that bank, causing USDC to briefly depeg to $0.87, leading to rapid panic.

The result of this 'stress test' was that the U.S. government, due to systemic risk prevention, ultimately provided full guarantees for all Silicon Valley Bank depositors.

Although it was not a specific rescue for Circle, this incident made Circle realize that merely being an issuer is not enough; it must control more infrastructure to truly master its own fate.

What truly triggered this sense of control was the dissolution of the Centre alliance. This event exposed Circle's 'worker' dilemma.

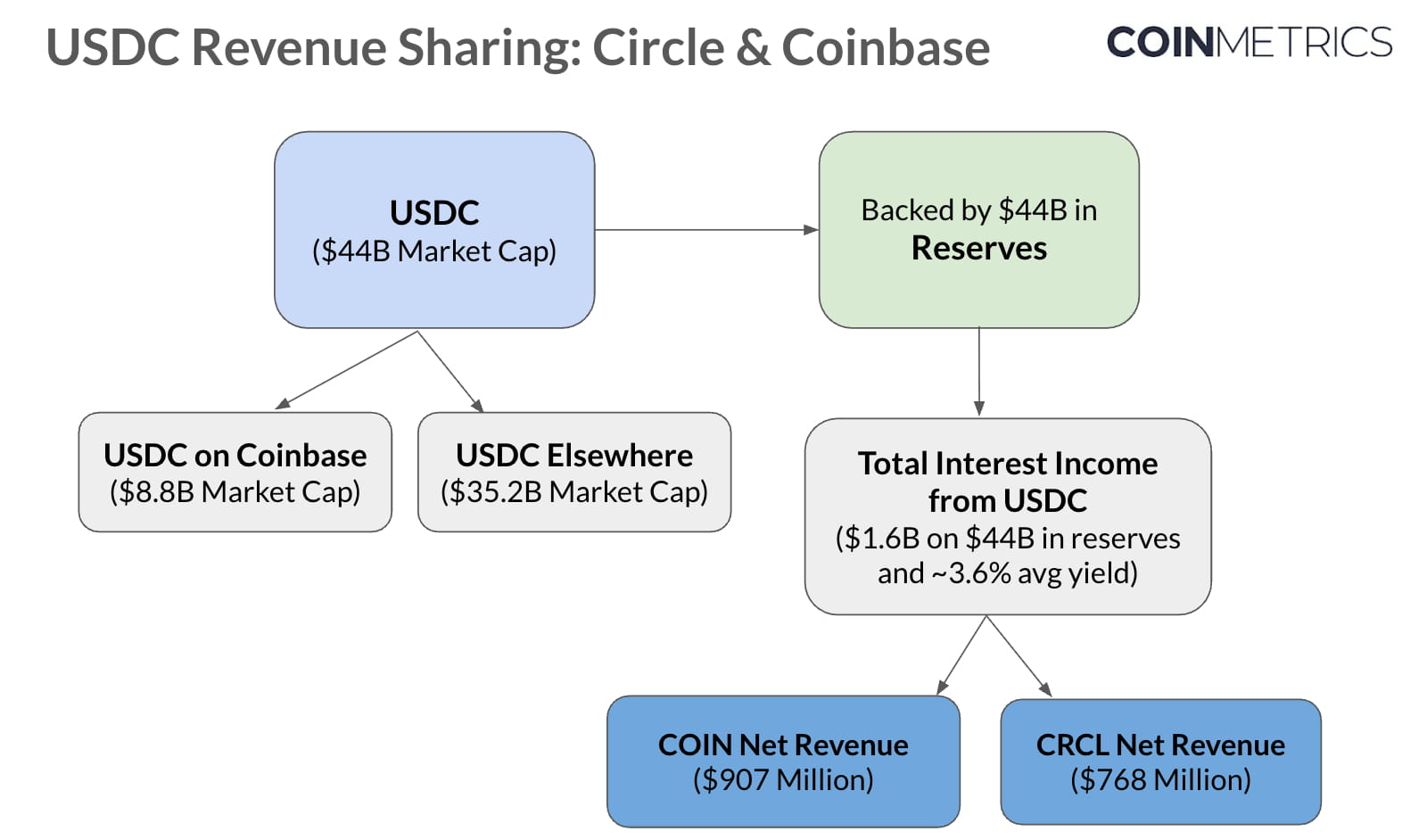

In August 2023, Circle and Coinbase announced the dissolution of the Centre alliance, with Circle fully taking over control of USDC. On the surface, this seems like Circle gaining independence; however, the cost is heavy, as Coinbase obtained a 50% share of USDC's reserve income.

What does this mean? In 2024, Coinbase generated $910 million in revenue from USDC, a year-on-year increase of 33%. Meanwhile, Circle paid over $1 billion in distribution costs in the same year, with most flowing to Coinbase.

In other words, half of the profits from USDC, which Circle worked hard to grow, have to be shared with Coinbase. It's like the central bank printing money but having to hand over half of the seigniorage to commercial banks.

Additionally, the rise of TRON has made Circle see new profit models.

In 2024, TRON processed $5.46 trillion in USDT transactions, averaging over 2 million transfers per day, earning substantial fee income just by providing transfer infrastructure, a more upstream and stable profit model than issuing stablecoins.

Especially with the expectation of interest rate cuts from the Federal Reserve, traditional stablecoin interest income will face contraction, while infrastructure fees can maintain relatively stable growth.

This also serves as a wake-up call for Circle: those who control the infrastructure can continuously collect taxes.

Thus, Circle began its transformation path toward building infrastructure, expanding in multiple directions:

Circle Mint allows corporate clients to directly mint and redeem USDC;

CCTP (Cross-Chain Transfer Protocol) enables the native transfer of USDC across different blockchains;

Circle APIs provide a complete set of stablecoin integration solutions for businesses.

By 2024, Circle's revenue reached $1.68 billion, and its revenue structure began to shift—besides traditional reserve interest, more is coming from API usage fees, cross-chain service fees, and enterprise service fees.

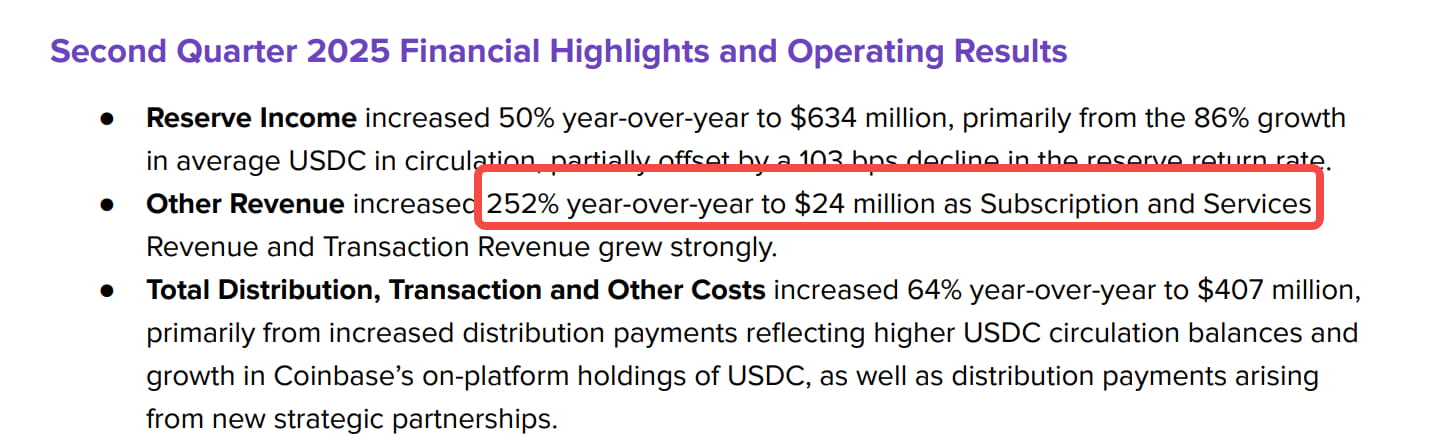

This transformation was confirmed in Circle's most recent financial report:

Data shows that Circle's subscription and service revenue reached $24 million in the second quarter of this year, although it only accounted for about 3.6% of total revenue (the majority still coming from USDC reserve interest), but it grew rapidly by 252% year-on-year.

Shifting from a single business model of printing money for interest to a diversified 'rental' business model gives more control.

The arrival of Arc is the highlight of this transformation.

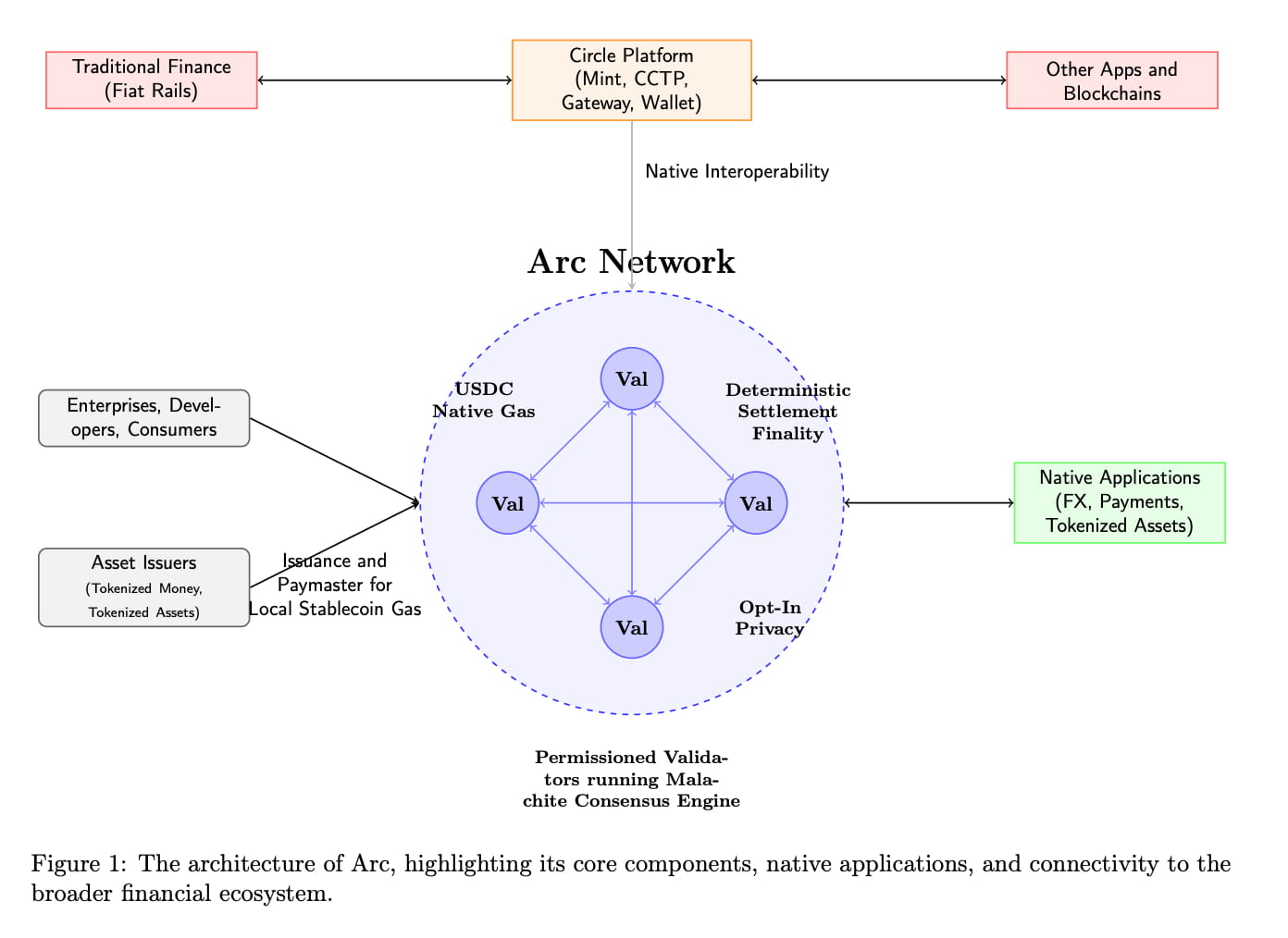

This is a blockchain tailored for stablecoins (USDC):

USDC serves as native gas, eliminating the need to hold ETH or other volatile tokens; a request for quotes system at the institutional level supports 24/7 on-chain settlement; transaction confirmations are less than one second, providing businesses with balance and transaction privacy options to meet compliance needs.

These functions are more like a technological declaration of monetary sovereignty. Arc is open to all developers, but the rules are set by Circle.

Thus, from Centre to Arc, Circle has completed a triple jump:

First leap: obtaining minting rights (USDC);

Second leap: building financial pipelines (APIs, CCTP);

Third leap: establishing sovereign territory (Arc)

This path almost reenacts the historical evolution of central banks in the digital world:

From private banks issuing banknotes, to monopolizing currency issuance rights, to controlling the entire financial system—only, Circle's speed is faster.

And this 'digital central bank dream' is not the only one chasing this vision.

Ambitions are the same, but paths differ.

In the stablecoin landscape of 2025, several giants have 'central bank dreams', but their paths differ.

Circle chose the most difficult but possibly the most valuable path: USDC → Arc blockchain → complete financial ecosystem.

Circle is not satisfied with merely being a stablecoin issuer; it aims to control the entire value chain—from currency issuance to the clearing system, from payment rails to financial applications.

The design of Arc is filled with 'central bank thinking':

First, it has monetary policy tools; USDC as native gas gives Circle a regulatory capability similar to a 'benchmark interest rate'; second is clearing monopoly; the built-in institutional-level RFQ foreign exchange engine requires on-chain foreign exchange settlements to go through its mechanism; finally, it retains rule-making power, allowing Circle to control protocol upgrades and decide which functions to launch and which actions to permit.

The most challenging aspect here is ecosystem migration—how to convince users and developers to leave Ethereum?

Circle's answer is not to migrate but to supplement. Arc is not meant to replace USDC on Ethereum but to provide solutions for use cases that existing public chains cannot meet. For instance, enterprise payments needing privacy, foreign exchange transactions requiring instant settlement, and on-chain applications with predictable costs.

This is a gamble. If successful, Circle will become the 'Federal Reserve' of digital finance; if it fails, the billions invested could go to waste.

PayPal's approach is pragmatic and flexible.

In 2023, PYUSD was first launched on Ethereum, in 2024 it expanded to Solana, in 2025 it went live on the Stellar network, and recently it even covered Arbitrum.

PayPal did not build a dedicated public chain but allowed PYUSD to flexibly spread across multiple available ecosystems, with each chain serving as a distribution channel.

In the early stages of stablecoins, distribution channels were indeed more important than building infrastructure. When you have something ready to use, why build it yourself?

First, occupy user minds and usage scenarios, then consider the infrastructure issue in the future, after all, PayPal itself has a network of 20 million merchants.

Tether, on the other hand, is like the de facto 'shadow central bank' of the crypto world.

It hardly interferes with the use of USDT, sending it out like cash; how it circulates is the market's business. Especially in regions and use cases where regulation is ambiguous and KYC is difficult, USDT has become the only choice.

Circle founder Paolo Ardoino stated in an interview that USDT primarily serves emerging markets (such as Latin America, Africa, Southeast Asia), helping local users bypass inefficient financial infrastructure, functioning more like an international stablecoin.

With a trading pair quantity on most exchanges 3–5 times that of USDC, Tether has formed a strong liquidity network effect.

Interestingly, Tether's attitude toward new chains is to not actively build but to support others in building. For example, supporting stablecoin-specific chains like Plasma and Stable. This is like placing a bet, maintaining presence in various ecosystems at a minimal cost to see which one can succeed.

In 2024, Tether's profits exceeded $10 billion, outpacing many traditional banks; Tether did not use these profits to build its own chain but continued to buy Treasury bonds and Bitcoin.

Tether bets that as long as it maintains enough reserves and avoids systemic risk, inertia can keep USDT dominating the stablecoin circulation.

The three models above represent three different judgments about the future of stablecoins.

PayPal believes in putting users first. With 20 million merchants, the technology architecture is secondary. This is the internet mindset.

Tether believes in liquidity being king. As long as USDT remains the base currency for trading, everything else is unimportant. This is the exchange mindset.

Circle believes in infrastructure being king. Controlling the rails means controlling the future. This is central bank thinking.

The rationale for this choice may lie in Circle CEO Jeremy Allaire's testimony before Congress: 'The dollar is at a crossroads; monetary competition is now a competition of technology.'

Circle sees not just the stablecoin market, but the standard-setting power of the digital dollar. If Arc succeeds, it could become the 'Federal Reserve System' of the digital dollar. This vision is worth the risk.

2026, a critical time window

The time window is narrowing. Regulation is advancing, competition is intensifying, and when Circle announced that Arc would launch its mainnet in 2026, the immediate reaction from the crypto community was:

Too slow.

In an industry that adheres to 'rapid iteration' as a creed, taking nearly a year to move from testnet to mainnet seems like a missed opportunity.

However, if you understand Circle's situation, you will find that this timing is quite favorable.

On June 17, the U.S. Senate passed the GENIUS Act. This is the first federal-level regulatory framework for stablecoins in the U.S.

For Circle, this is a long-awaited 'rebranding'. As the most compliant stablecoin issuer, Circle has nearly met all the requirements of the GENIUS Act.

2026 is precisely the time when these details will be implemented and the market will adapt to new rules. Circle does not want to be the first to take the plunge but also does not want to arrive too late.

Corporate clients value certainty the most, and what Arc provides is precisely this certainty—certain regulatory status, certain technical performance, and a certain business model.

If Arc successfully goes live and attracts enough users and liquidity, Circle will establish its leadership position in the stablecoin infrastructure space. This could open a new era—a reality where 'central banks' operated by private companies exist.

If Arc performs mediocrely or is surpassed by competitors, Circle may have to rethink its positioning. Perhaps in the end, stablecoin issuers can only be issuers, not dominate the infrastructure.

Regardless of the outcome, Circle's attempt is prompting the entire industry to ponder a fundamental question: In the digital age, who should hold the control over money?

The answer to this question may become clear in early 2026.