Continuing from the analysis in the previous article, China RWA Trilogy Research - Maluzhen Grape Project (China's Non-Standard Assets) 1

Circulation mechanism design

One of the charms of RWA lies in the tokenization of offline assets, enabling circulation in global markets, while the Malu project has made significant sacrifices in this regard.

On November 25, 2024, Maluzhen Grape NFT digital collectibles will be publicly issued on the Shanghai Data Exchange.

Basic rights include 1924 basic version NFTs and 100 scarce version NFTs.

The basic version can obtain a 2 jin (1 kg) pickup card for “Sunshine Rose” grapes, valued at about 200 yuan, valid until December 8, 2025;

The scarce version can obtain a 2 jin (1 kg) pickup card for “Queen Nina” grapes + 2 tickets to Maluzhen Park, valued at about 300 yuan, with a validity period the same as the basic version.

👊 And it is limited to trading from December 9, 2024, to December 8, 2025, with mandatory delisting upon expiration;

👊 Single user holding amount ≤ 5% of the total issuance (about 101), exceeding the limit requires splitting for sale; after a single sale, a waiting period of 5 trading days is needed before trading again.

Basically, such a design has stripped this NFT of even its circulation value, which is a common issue we can see in current RWA projects in China—lack of liquidity!

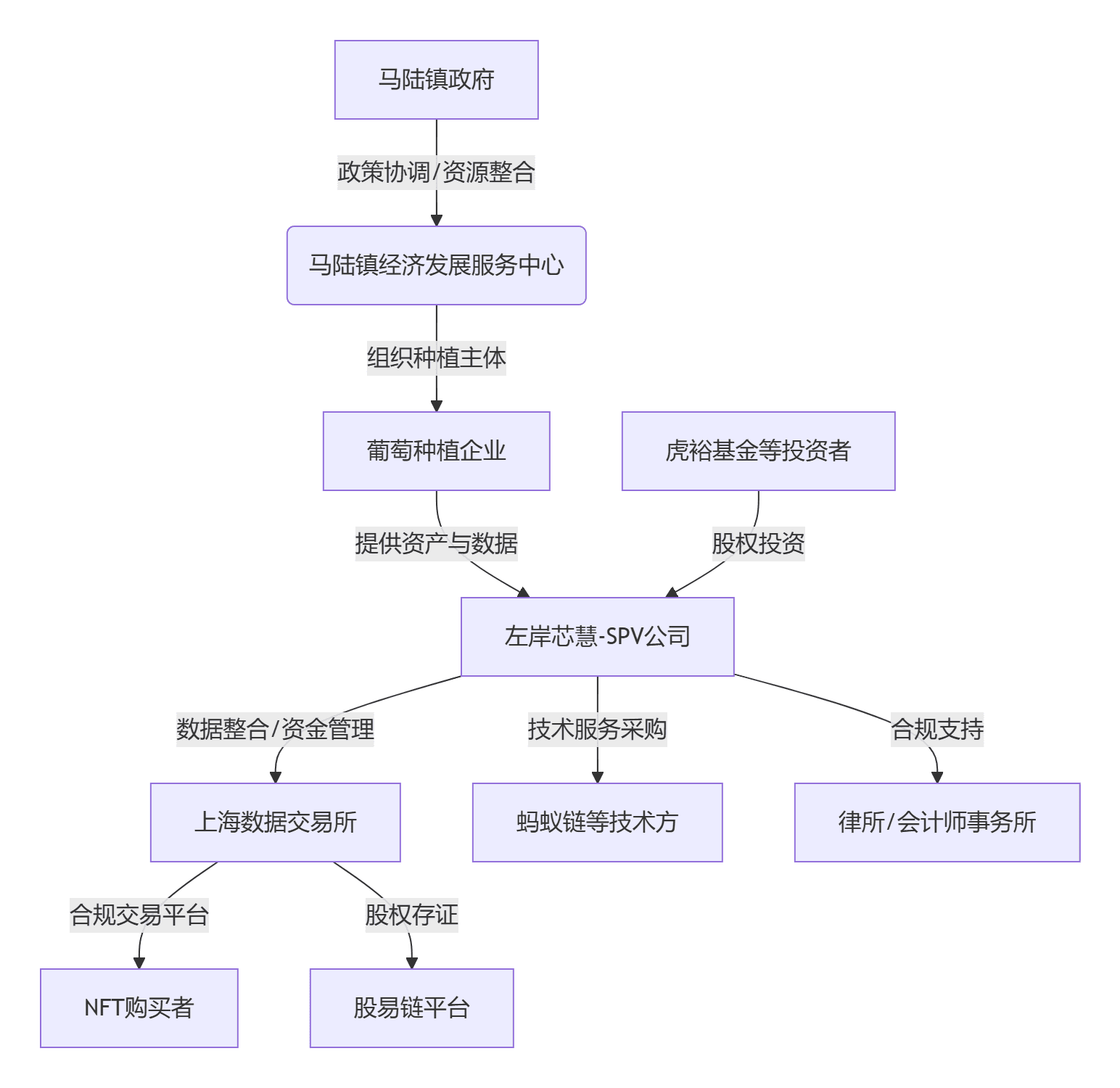

3. Sorting out the relationships among project participants

In China, the participants behind the project cannot be ignored, especially since the Maluzhen grape project involves state-owned assets. This factor can be contrasted with the subsequent project of Langxin Technology to see what characteristics state-owned asset on-chain projects have.

First is the core participants of the project:

Left Bank Xin Hui (project operator), responsible for integrating grape production data and brand qualifications, issuing NFT digital assets, and managing equity financing funds, and is a core participant in the entire project.

Shanghai Data Exchange (compliance trading platform), responsible for providing “Data Asset Shell (DAS)” on-chain proof services, building NFT trading channels, and ensuring compliance with information disclosure.

Maluzhen Economic Development Service Center (government coordinating party), responsible for policy endorsement and resource connection.

Maluzhen Grape planting enterprise (underlying asset provider): provides physical grape assets and generates agricultural data.

Secondly, there are some third-party service companies, such as law firms, asset evaluation companies, equity custody institutions, etc.

Here I have drawn a diagram to organize the project participants. It can be seen that, at least in this project, its essence is a market-driven governance experiment guided by the government, which is very characteristic of China, a local pilot.

One can refer to the relationship between China and Hong Kong, with Hong Kong as a pilot for foreign openness, establishing sandbox mechanisms, and selectively introducing inland after mature and stable.

Special economic zones, the rich lead to the richer (in reality, there is no follow-up on that 😂😂😂)

4. Project analysis

From here, we can actually see that

The Maluzhen Grape RWA is essentially an NFT as a compliant shell, with equity financing carrying the core value of capital operations, being a “chain shell + traditional financial core,” where technology serves only to enhance credit rather than liberalize, a “Chinese-style” RWA project with high government involvement.

Compared to typical RWA projects, it clearly has many localized improvements.

Specific references can be found in the table below.

Summarizing several characteristics of this project

Government-led initiatives are evident, and a notable point in on-chain projects for state-owned and private assets in the country needs special attention.

The inherent characteristics of agricultural non-standard assets require investment in data collection, and there is also a lack of a unified pricing market for asset evaluation, which is inherently risky.

Rather than being an RWA project, it is better described as a semi-finished RWA product with Chinese characteristics; the on-chain aspect is a private chain with almost no liquidity, leaning more towards NFT mechanics, but lacking liquidity compared to typical NFT projects.

The underlying assets do not generate income; they are anchored to physical goods, suggesting that the commemorative significance of buying the NFT may outweigh the satisfaction of eating grapes.

So, what is the significance of this project? How difficult is it to promote? What is the situation of other similar Chinese non-standard asset on-chain projects?

The next post will continue the analysis.