In the past 24 hours, the crypto industry has seen a wave of new actions regarding stablecoins.

Circle announced the launch of a new public chain named Arc, designed specifically for stablecoin finance and asset tokenization as an EVM Layer 1, using USDC as the native gas asset and equipped with permissioned institutional validators, targeting global payments, foreign exchange settlements, and capital markets.

Around the same time, payment giant Stripe was revealed to be collaborating with Paradigm to develop the Tempo blockchain, combining the previously acquired stablecoin infrastructure company Bridge and wallet developer Privy, rapidly shaping Stripe's stablecoin ecosystem. Meanwhile, USDT issuer Tether is also busy accelerating the development of its chain Plasma/Stable to further strengthen its dominant position in exchanges and the consumer market.

The commonality among these giants is: they are no longer satisfied with issuing tokens on existing chains, but instead want to master the operational rules of the entire chain, bringing everything from users to validator nodes under control.

Legislative Catalyst: The 'starting gun' for U.S. stablecoins has sounded.

If we are to find a time marker to explain the background of this wave of 'stablecoin self-built chains', the U.S. (GENIUS Act) this July is undoubtedly a key trigger. This act, signed by President Trump, provides a clear legal framework for the issuance, settlement, and reserve management of stablecoins at the federal level for the first time.

For companies like Circle and Stripe, which are already licensed operators with close ties to financial institutions, this is a public 'pass' — the compliance foundation has been laid, and the remaining question is who can more quickly and thoroughly secure the technological foundation of stablecoin business. Thus, we see them rapidly accelerating their own chain development, striving to complete infrastructure layout before the policy dividends are realized.

Stablecoins are sliding towards 'bankification'.

However, in a recent Web3 Summit and several interviews, Gavin Wood mentioned that stablecoin issuers are essentially banks now. USDC and USDT are increasingly resembling banks, and they are highly regulated centralized banks.

If Circle and Stripe build their own EVM chains, they are likely to become increasingly centralized — not only in governance but also in control over transaction processing, validator selection, and compliance rules.

Chains led by companies typically prioritize regulatory compliance and operational efficiency over decentralization, which may mean:

• Validators are permissioned, not open to everyone; • Strict KYC/AML requirements are enforced on all users;

• Upgrades and rule-making are driven by Circle's business priorities, with decisions highly centralized;

• The freezing and blacklisting mechanisms at the contract level mean that assets could be 'paused' at any time.

Once the majority of global stablecoin settlements are monopolized by a few centralized entities, the entire industry will face significant single-point risks and governance centralization issues. At that time, the so-called 'chain' will resemble a proprietary ledger owned by enterprises, merely cloaked in blockchain attire.

So, while it may still be 'EVM-compatible', its spiritual core will increasingly diverge from Ethereum's open, permissionless design.

Some believe that the development of so many giants' own EVM chains is beneficial for Ethereum, but I only see the downside: these giants will take away Ethereum's users and liquidity. These giants will only tell you that what is truly valuable is EVM, not Ethereum or ETH.

What will this lead to?

Of course, we do not deny that this is good news; after all, the influx of institutions will bring more liquidity to the entire crypto industry, but at the same time, it also harbors 'crisis' and the next opportunity — decentralized stablecoins.

Decentralized stablecoins typically refer to stablecoins that do not rely on a single centralized issuer, such as crypto-collateralized or algorithmic stablecoins, in contrast to centralized stablecoins (like USDT and USDC).

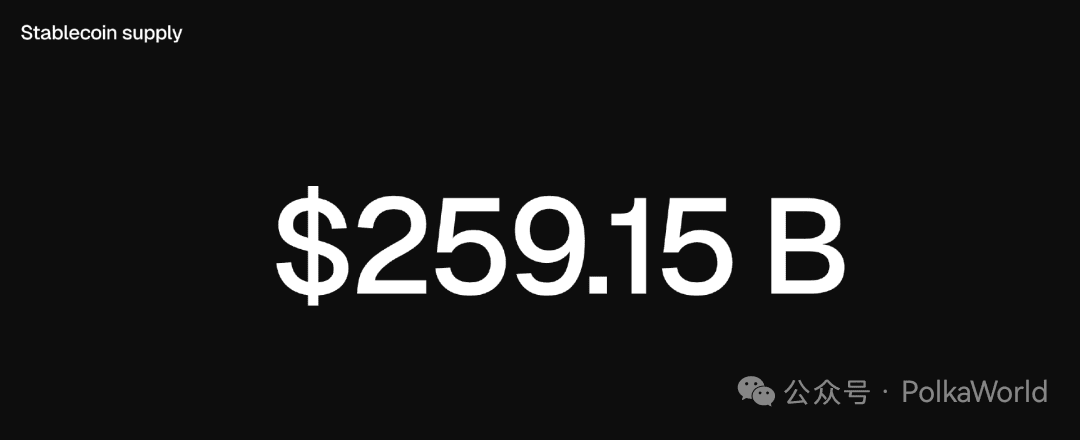

Currently, the overall stablecoin market size has exceeded $250 billion, but the proportion of decentralized stablecoins is relatively small, mainly active in the DeFi field.

What decentralized stablecoins are currently available?

1. Crypto-Collateralized:

By locking other crypto assets (like ETH) through smart contracts as over-collateral (usually over 150%), maintaining a 1:1 peg to the dollar. It relies on decentralized oracles for real-time price data and manages volatility risks through automatic liquidation mechanisms. This type of stablecoin emphasizes decentralization and transparency but is sensitive to collateral volatility. Examples include DAI (MakerDAO), LUSD (Liquity), sUSD (Synthetix), etc.

2. Algorithmic:

Not relying on full reserves, but maintaining the peg through algorithms and market incentives (such as supply elasticity adjustments or dual-token models). Subtypes include rebasing (automatically adjusting supply) and seigniorage models (issuing bond tokens). Examples include Ampleforth (AMPL), Basis Cash, TerraUSD (UST, now collapsed), Frax (partially algorithmic), etc.

This type of stablecoin is highly decentralized but susceptible to market panic. The collapse of UST in 2022 resulted in a loss of $40 billion, highlighting algorithmic vulnerabilities. Many projects have shifted to hybrid models to enhance stability.

3. Hybrid:

Combining crypto collateral, hedging, yield, and algorithmic elements, or integrating real-world assets (RWA, such as short-term government bonds). Dynamically adjusting collateral ratios and potentially generating yields (e.g., annualized 5% APY). Examples include Frax, USDD (Tron), USDY (Ondo USD Yield), GHO (Aave), USDe (Ethena), etc.

This type of stablecoin is more resilient and suitable for cross-chain applications, but regulatory complexities exist (such as USDY restrictions on U.S. users). By 2025, hybrids will grow rapidly, driven by RWA trends.

Market Share Analysis

According to 2025 data, the overall stablecoin market capitalization is approximately $259.15 billion, with USD-pegged stablecoins accounting for 99%. The market share of decentralized stablecoins is relatively small (around 5-10%), mainly due to the liquidity advantages of centralized stablecoins (like USDT accounting for 60-70% and USDC for 25%).

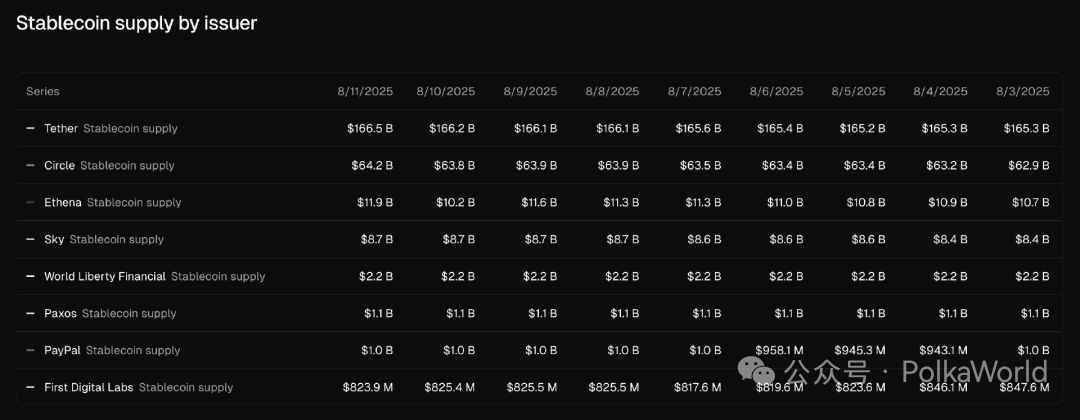

From the above image, it can also be seen that Tether and Circle together occupy about 90%+ of the market supply.

Decentralized stablecoins Sky (DAI) and Ethena (USDe) are among the top ten decentralized stablecoin projects, but their market capitalization is significantly lower compared to leading fiat-collateralized stablecoins. However, decentralized stablecoins have a higher proportion in DeFi, driving innovations such as lending and derivatives.

Moreover, traditional financial and payment giants like PayPal and World Liberty Financial are also entering the stablecoin issuance race.

Growth Trends

By 2025, stablecoin supply is expected to grow by 39%, with monthly transaction volume reaching $1.5 trillion. Decentralized stablecoins like USDe are projected to grow by 84%, benefiting from regulatory clarity (such as the EU's MiCA regulation) and cross-chain interoperability. However, the share of algorithmic stablecoins is declining due to risk events.

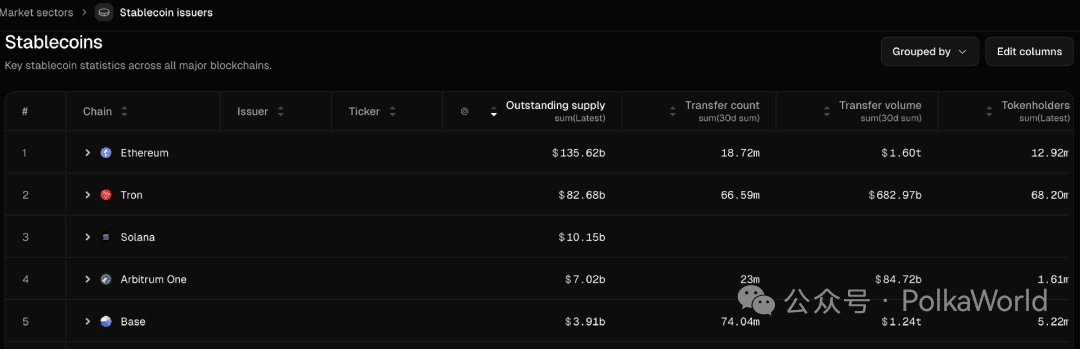

In terms of platform distribution, Ethereum accounts for over 55%, Tron 34%. Solana and Base are growing, supporting more decentralized issuance.

Ethereum holds an absolute advantage in total market value and transaction volume of stablecoins ($1.6 trillion monthly transaction volume), but the number of holders is relatively small, indicating that Ethereum is more used in institutional and large transaction scenarios.

Tron's number of holders and transaction frequency far exceed others (66.59 million holders), but its total transaction volume is lower than Ethereum, indicating its popularity in small payments and cross-border remittances.

Base's transaction volume in the past 30 days (74.04 million transactions) is close to Tron, and the total transaction amount ($1.24 trillion) is close to Ethereum, indicating its rapid rise in the stablecoin transfer arena.

Additionally, some reports predict that by 2030, the market may reach $2-3.7 trillion, with the decentralized share potentially rising to 10-15%, mainly driven by DeFi and RWA.

Polkadot will also issue decentralized stablecoins.

Yes, if you noticed Gavin Wood's speech at the Web3 Summit a while back, you should already know that Polkadot will also issue a native stablecoin and ensure complete decentralization.

Gavin stated that this will be one of the directions he promotes — creating a truly Web3 stablecoin.

It must be decentralized, with no centralized issuer;

It must be sound, with a rational and justifiable mechanism to maintain its value;

It must be capital-efficient, as many so-called decentralized stablecoins have very low capital efficiency;

It must be inclusive, scalable, and universal.

Currently, the widely used stablecoins are mostly centralized, merely a shell of Web2.

While there isn't much information about this stablecoin yet, from Gavin's hints at the Web3 Summit, DOT will be part of the collateral for this project, and it will be initiated through a treasury proposal.

So, will this native stablecoin be HOLLAR?

If you are closely following Polkadot's ecological progress, you should know that HOLLAR, a decentralized, over-collateralized stablecoin pegged to the dollar (1 HOLLAR ≈ 1 USD), was announced by Hydration (formerly HydraDX) in March this year for trading, lending, payments, and other scenarios. HOLLAR is native to Hydration and Polkadot.

It is based on the smart contract mechanism driving AAVE's stablecoin GHO, allowing anyone to mint HOLLAR after providing collateral. Its current design is:

Deep integration with high capital efficiency AMMs, using on-chain routers to find the most efficient trading paths, providing excellent liquidity;

The interest income generated will flow into the Hydration treasury, forming a sustainable revenue source;

Complete governance control achieved by the Hydration community through the cutting-edge Web3 governance mechanism OpenGov;

Priority on-chain liquidation enhances stability and reduces risk;

Providing liquidity incentives for minting HOLLAR.

The latest information is that Hydration is completing the final preparations for HOLLAR's launch on the testnet.

However, whether the stablecoin mentioned by Gavin refers to HOLLAR has not yet been officially confirmed.

Regardless of the answer, this means Polkadot will enter the decentralized stablecoin market, bringing truly decentralized value-pegged assets to Web3. Stay tuned to PolkaWorld, and we will continue to follow this development.

Conclusion

It is foreseeable that centralized stablecoin chains and decentralized stablecoin networks will coexist, but they represent two entirely different value propositions. The former pursues compliance, control, and operational efficiency at the cost of sacrificing openness and resistance to censorship; the latter seeks financial sovereignty and public attributes, which may require exploring more balance in terms of performance and compliance.

The implementation of stablecoin legislation in the U.S. will undoubtedly accelerate this differentiation process. Giants will use it to build 'bank-like' chains, while public chain projects like Ethereum and Polkadot will attempt to maintain their decentralized original intent.

For users, choosing one path over another will determine whether you are a serviced customer or a truly autonomous participant in the future on-chain world.