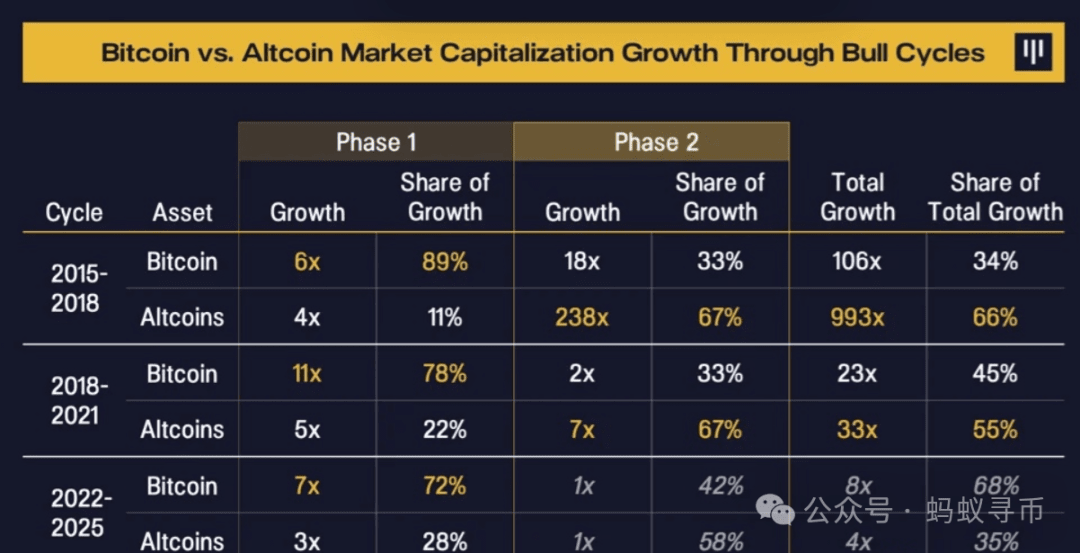

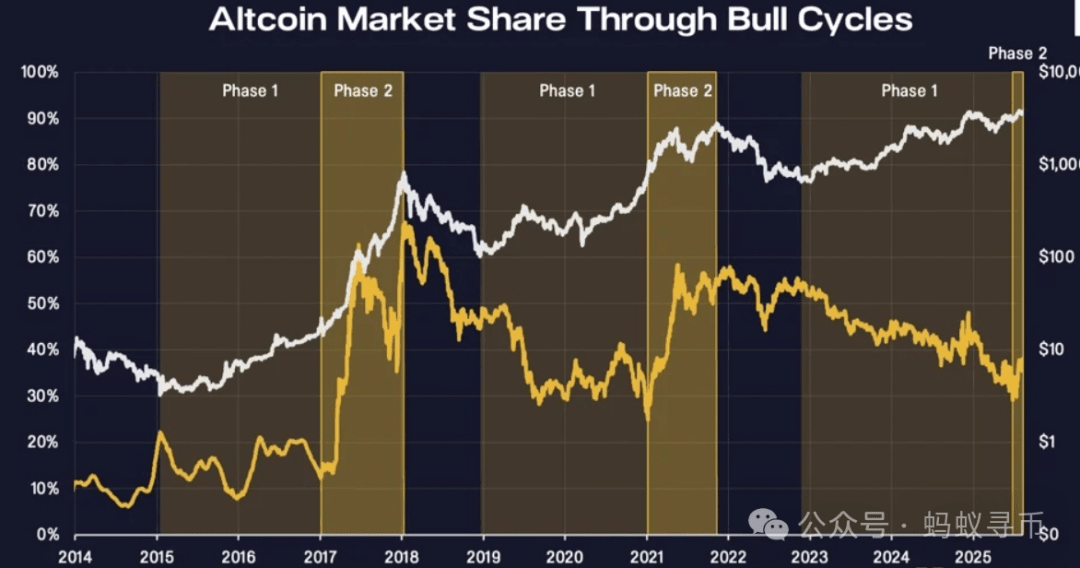

Bitcoin often leads bull market cycles, while altcoins tend to lag in the early stages. As the cycle progresses, altcoins often gain momentum and outperform Bitcoin at the end of the cycle. We refer to this as the 'first phase' and 'second phase' of a bull market.

Importantly, in the past two cycles, altcoins have contributed the majority of value creation. In the 2015-2018 cycle, altcoins contributed 66% of the total growth in cryptocurrency market value. In the 2018-2021 cycle, altcoins contributed 55%.

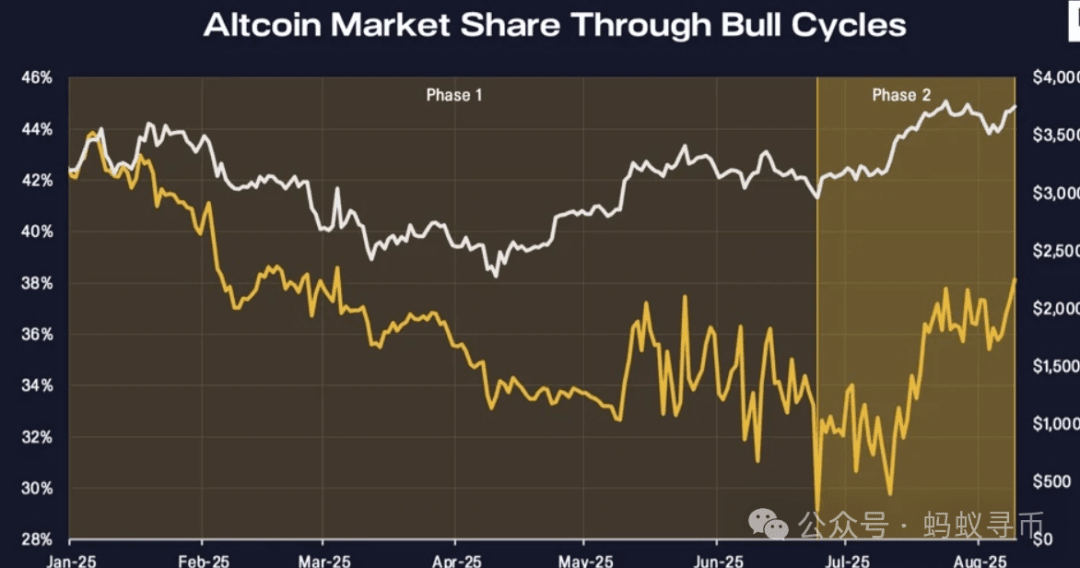

So far, altcoins have accounted for 35% of the overall market growth in this cycle.

For a long time, Bitcoin has benefited from regulatory clarity—this is reflected not only in its classification as a commodity but also in its well-known role as 'digital gold.' This has been a key driving force behind Bitcoin's outperformance relative to altcoins in the early stages of this cycle. Altcoins have historically faced greater regulatory uncertainty, which has only recently changed. Under the leadership of the new U.S. government, this landscape is shifting, making significant progress in driving digital asset innovation.

Historically favored for its clarity and tailwinds, Bitcoin's advantages are now starting to extend to altcoins. The market is beginning to reflect this.

As victories in regulatory matters continue to accumulate, momentum is building. Last month, President Trump signed the GENIUS Act, creating conditions for the prosperity of U.S.-regulated stablecoins, which are expected to become the engine of global financial transactions. The CLARITY Act, passed by the House of Representatives, aims to establish clearer boundaries between digital commodities and securities, helping to address the long-standing jurisdictional uncertainty between the U.S. SEC and the Commodity Futures Trading Commission (CFTC). A transformation is underway, and we have reason to believe that non-Bitcoin tokens will be one of the biggest beneficiaries.

Innovation and development are accelerating, especially in the field of tokenization. Robinhood recently launched stock tokens supported by Arbitrum, aimed at democratizing stock trading and creating more efficient markets. Major U.S. banks like Bank of America, Morgan Stanley, and JPMorgan Chase are exploring issuing their own stablecoins. BlackRock's BUIDL fund has accumulated $2.3 billion in tokenized national bonds. Figure has processed over $50 billion in blockchain-native RWA transactions. In addition to tokenized bond funds, Ondo also plans to list over 1,000 tokenized stocks on the NYSE and Nasdaq through Ondo Global Markets. On-chain migration is underway.

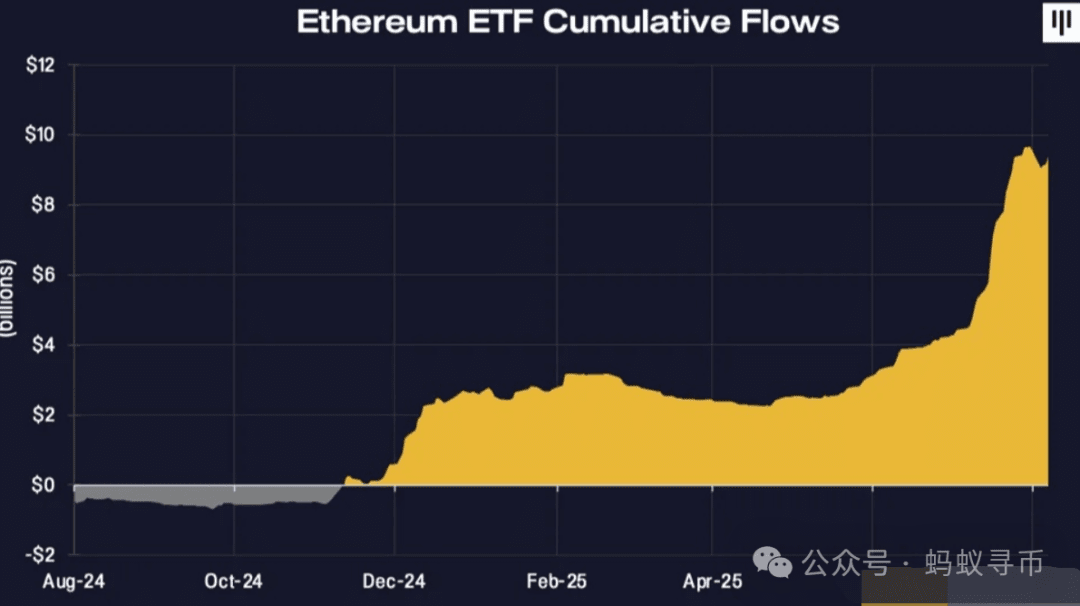

Ethereum is driving the growth of non-Bitcoin market share.

Most assets in the real world are flowing to Ethereum. In the $260 billion stablecoin market, 54% of stablecoins are issued on Ethereum. 73% of on-chain national bonds are on Ethereum. DAT is accumulating ETH at an unprecedented rate. Wall Street is gradually becoming aware of this, and the demand for ETH is skyrocketing.

The price of Ethereum, priced in BTC, has increased by 103% since hitting bottom in April 2025.