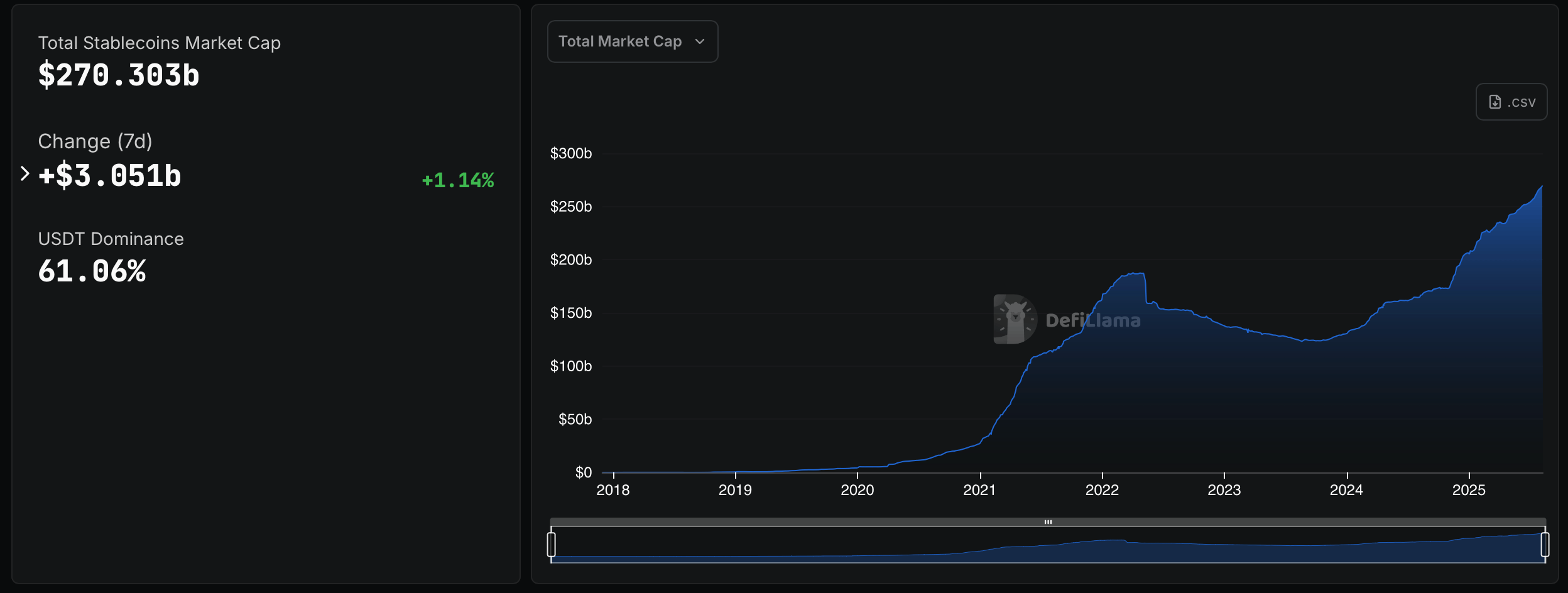

The total market value of stablecoins reached $270.3 billion, with USDT accounting for 61.06% market share and a 30-day trading volume of $2.7 trillion.

The stablecoin market continues to assert its important position in the cryptocurrency ecosystem as total capitalization surpasses $270 billion, marking a new historical milestone for the sector. According to data from Defillama and Artemis Analytics, the current figure of $270.303 billion reflects an increase of $3.051 billion or 1.14% over the past seven days, continuing the steady growth trend throughout 2024 and 2025.

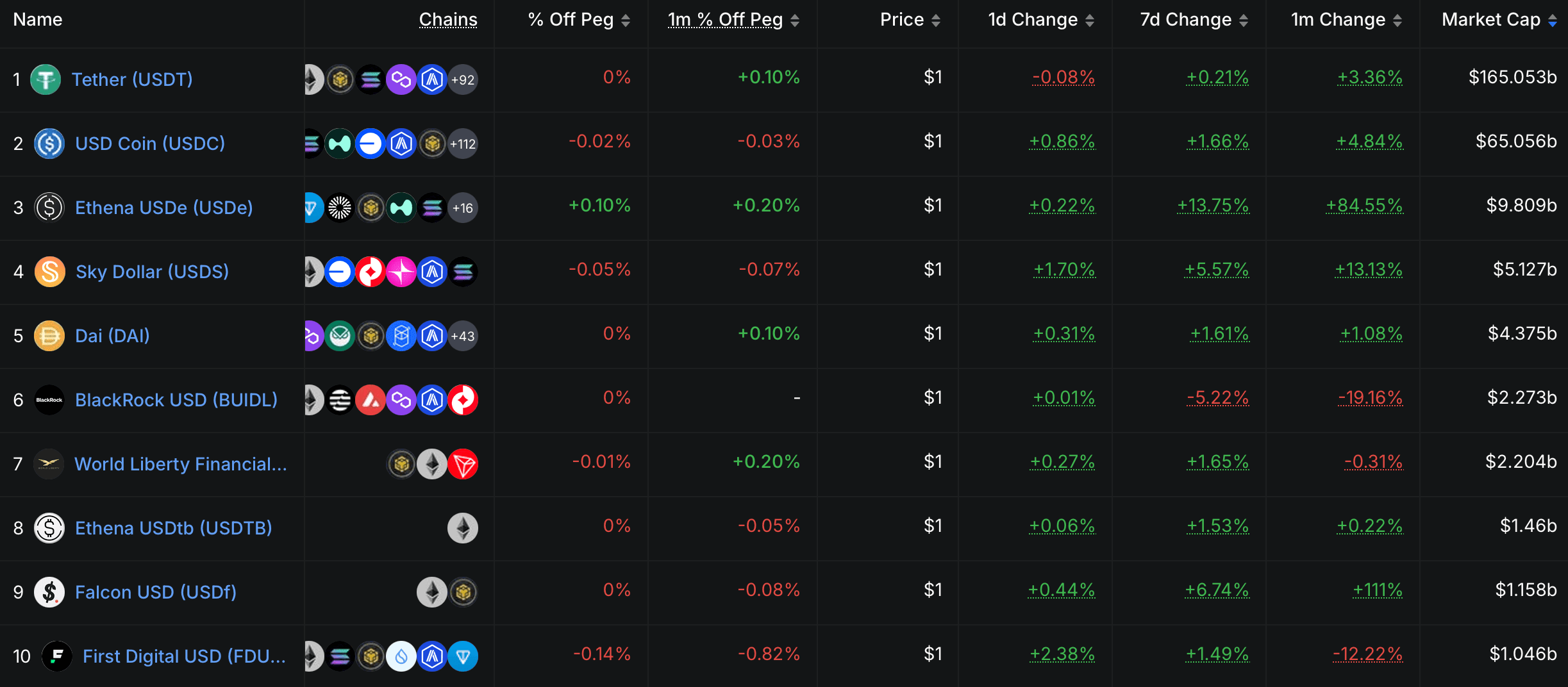

This development reflects the circulating supply multiplied by the market price, primarily focused on USD-pegged tokens. Tether (USDT) maintains its dominant position with a 61.06% market share, while USDC comes in second. Other competitors like Ethena’s USDe, Sky’s USDS, DAI, and BlackRock’s BUIDL only account for single-digit percentages, indicating a strong concentration on the top two issuers.

Source: Defillama.com

Source: Defillama.com

Data from Artemis Terminal shows USDT continues to lead in 2025, while USDC has a tendency to increase its market share. Market activity remains high with 42.8 million wallet addresses interacting with stablecoins in the past month, although down 15.2% from 30 days ago, it still falls within the high range of the past five years.

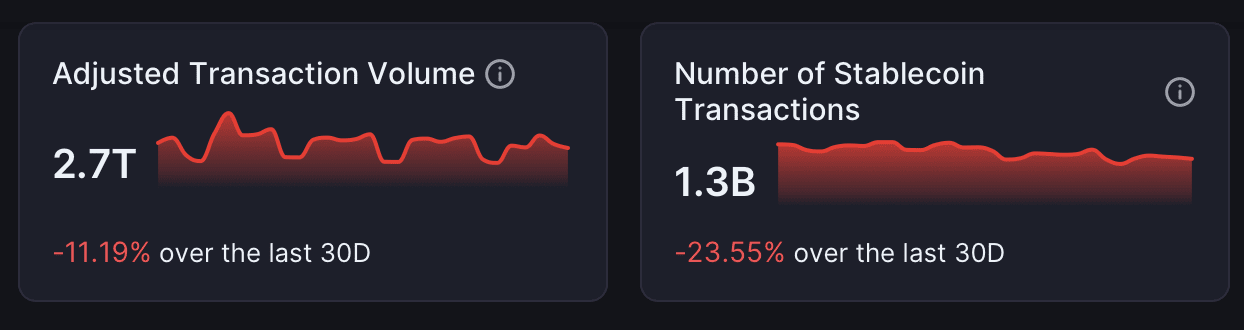

Trading volume equivalent to Visa scale

Adjusted trading volume over the past 30 days reached $2.7 trillion, a decrease of 11.19% from the previous month but still maintaining an impressive level. Multi-year data shows this volume fluctuating around $1 trillion for most of 2024-2025, equivalent to the scale of Visa and significantly higher than PayPal or the total global remittance value.

Source: Artemis Terminal

Source: Artemis Terminal

The number of transactions reached 1.3 billion in 30 days, down 23.55% from the previous period, but still reflecting high usage frequency for payment, settlement, trading, and wallet deposits/withdrawals across both centralized exchanges and on-chain platforms. Trading activity has expanded across multiple blockchains, with significant participation from BNB Chain, Tron, Base, Arbitrum, Solana, and OP Mainnet alongside Ethereum.

The supply structure is heavily skewed towards the USD, with the majority of stablecoins issued pegged to the US dollar. Other currencies like the euro and British pound account for a very small proportion, affirming the dominant role of the USD in the stablecoin ecosystem. USD-pegged tokens continue to play a crucial role as price-pegged assets and primary collateral on major exchanges and lending platforms.

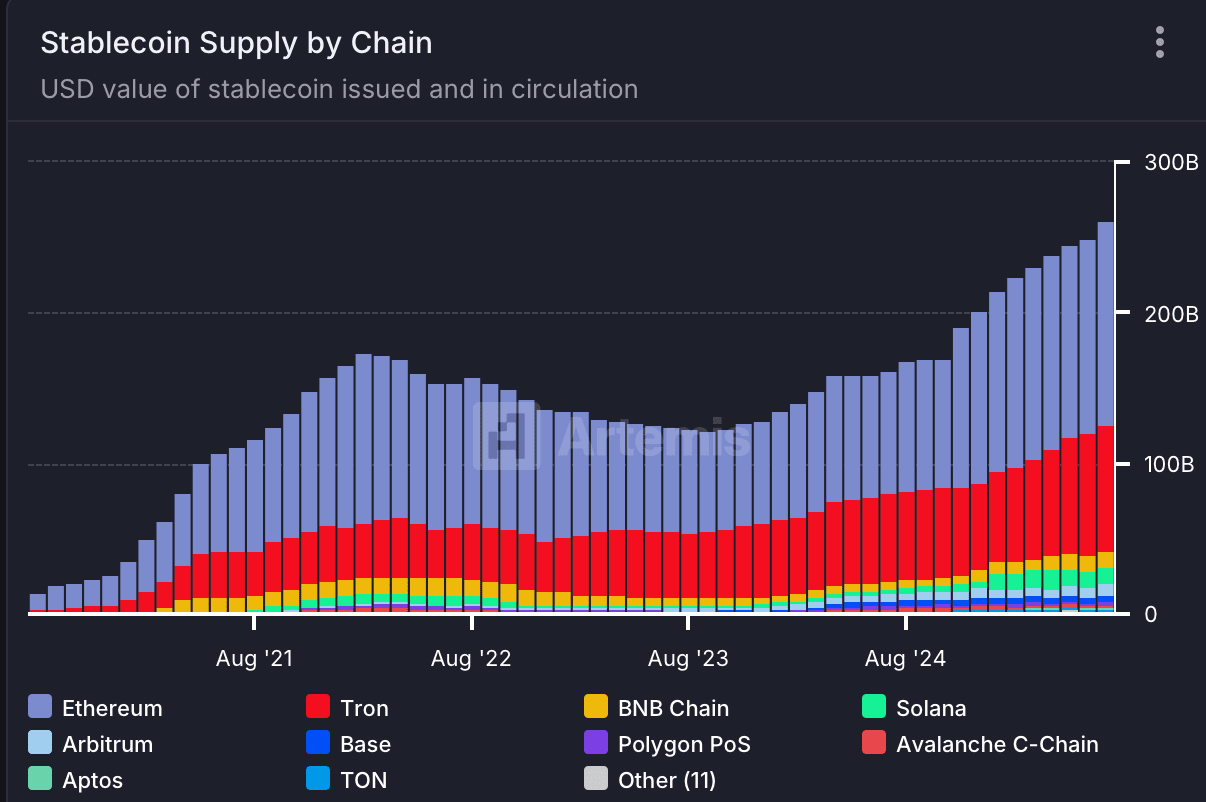

In terms of blockchain allocation, Ethereum and Tron lead with the largest balances, followed by BNB Chain, Solana, Base, and Arbitrum. Five-year data shows Ethereum at the top for absolute supply growth, Tron in second place, while Base and Solana are emerging as important additional issuance and circulation channels.

Source: Artemis Terminal

Source: Artemis Terminal

Analysis by timezone on Ethereum and Solana shows that most transactions come from North America and Asia, while Europe's market share has been increasing since 2024. Latin America, Southeast Asia, and Africa have smaller but notable shares, reflecting the participation of both individual and institutional users globally.

The activity address chart by token shows USDT and USDC as the main drivers, with the number of addresses and interactions reaching new highs in 2025. Smaller issuers like PYUSD maintain stable activity but on a limited scale. The broad coverage of active addresses reinforces the role of stablecoins as entry points and means of payment-settlement in the crypto ecosystem.

Source: Defillama.com

Source: Defillama.com

The current market capitalization of $270.3 billion marks a new peak in the recovery phase, after the market rose from under $10 billion in 2019 to over $250 billion by the end of 2021, then adjusted and gradually recovered into 2025. The combination of a dominant issuer, multi-chain allocation, and high address activity levels indicates stable demand for tokenized dollars in trading, remittances, and settlement.