Author: Ryan Yoon, Research Analyst at Tiger Research; Translation: Jinse Finance Xiaozou

Although the private equity market offers substantial returns, retail investors still find it difficult to enter; this field remains an exclusive battleground for institutional investors and high-net-worth individuals.

Tokenization technology is expected to address the inherent limitations of the traditional financial system — especially problems like insufficient liquidity, high barriers to entry, and operational complexities — but significant legal and technical obstacles remain.

Ventuals, Zoshi, and FreeStock are exploring different paths for the tokenization of private equity. Although still in the early stages, these attempts have shown potential to break down structural barriers in the market.

1. The allure of private equity is great — but it has nothing to do with you.

How can ordinary people invest in SpaceX or OpenAI? As non-listed companies, they are off-limits for most investors. Retail investors have almost no channels for participation — investment opportunities typically only arise after an IPO.

The core issue is that you are excluded from the high returns created in the private market. Over the past 25 years, the value created by the private market is approximately three times that of the public market.

Two structural factors lie behind this. First, financing is a highly sensitive process for private companies. Regardless of investor qualifications, transactions often only occur with well-known institutional investors. Second, the growth of the private capital market has broadened financing channels. Nowadays, many companies can raise billions of dollars without going public.

OpenAI is an example of these two trends. In October 2024, it raised $6.6 billion from major investors such as Thrive Capital, Microsoft, Nvidia, and SoftBank. By March 2025, it secured another $40 billion in funding led by SoftBank, with participation from Microsoft, Coatue, and Altimeter, setting a record for the largest private financing round in history.

This is a system limited to participation by specific institutional investors, while mature private capital infrastructure provides companies with alternatives beyond going public.

Therefore, today's investment landscape shows an increasingly severe exclusivity, exacerbating inequality in accessing high-growth opportunities.

2. Equal participation — can tokenization break down structural barriers?

Can tokenization technology really solve the structural inequalities in the private equity market?

On the surface, this model appears attractive: converting real-world assets into digital tokens, enabling fragmented ownership and supporting 24/7 trading in global markets. However, essentially, tokenization merely repackages existing assets like Pre-IPO equity into a new form — solutions to improve participation have long existed within the traditional financial system.

For example, Ustockplus under South Korea's Dunamu, as well as platforms like Forge and EquityZen in the United States, allow retail investors to participate in trading non-listed stocks within existing regulatory frameworks.

So, what exactly is the differentiated value of tokenization?

The key difference lies in the market structure. Traditional platforms use a peer-to-peer (P2P) matching model — buyers must respond to sellers' orders. If there are no counterparties, the transaction cannot be completed. This model suffers from insufficient liquidity, limited price discovery, and uncertain execution times.

Tokenization technology is expected to break through these structural limitations. If tokenized assets are listed on centralized exchanges (CEX) or decentralized exchanges (DEX), liquidity pools or market makers can provide continuous counterparties, thereby enhancing trading execution and pricing efficiency. Besides reducing friction, this approach will also reshape market architecture.

Moreover, tokenization can also realize innovative functions that the traditional financial system cannot support. Smart contracts can automatically allocate dividends, execute condition-based trades, or implement programmable governance rights. These functions give rise to entirely new types of financial instruments — designed with both flexibility and transparency.

3. Pre-IPO equity tokenization projects.

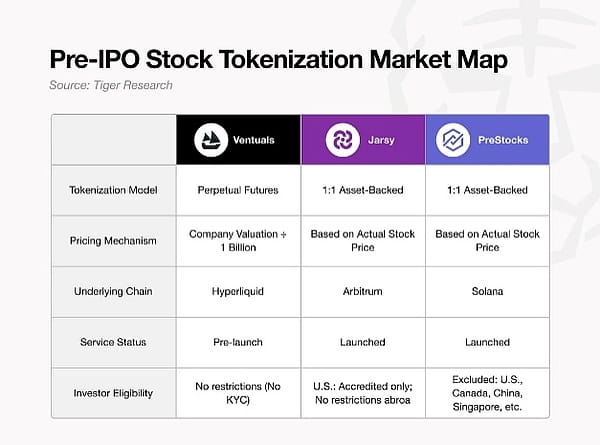

(1) Ventuals

Ventuals is built on a perpetual contract structure, with its core advantage being the ability to trade derivatives without holding the underlying asset. This design allows the platform to quickly launch various Pre-IPO stocks, bypassing conventional regulatory requirements such as identity verification or accredited investor certification.

This perpetual contract is implemented through Hyperliquid's HIP-3 standard, but this standard is currently only operational on the testnet, and Ventuals is still in pre-release phase.

Its pricing model also breaks the norm: the token price is not based on the stock price or actual market trades, but rather the company's total valuation divided by one billion. For example, if OpenAI is valued at $35 billion, each vOAI token would be priced at $350.

However, this low barrier to entry comes with structural challenges — most notably, the issue of oracle dependency. The valuation data of non-listed companies is inherently opaque and lagging, and derivatives based on such incomplete information may exacerbate market information asymmetry.

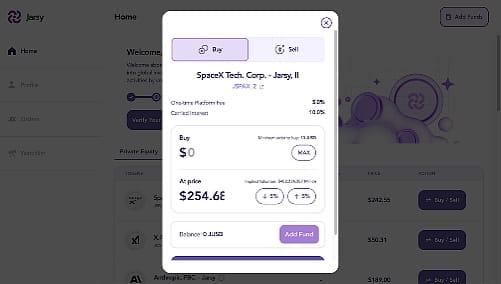

(2) Jarsy

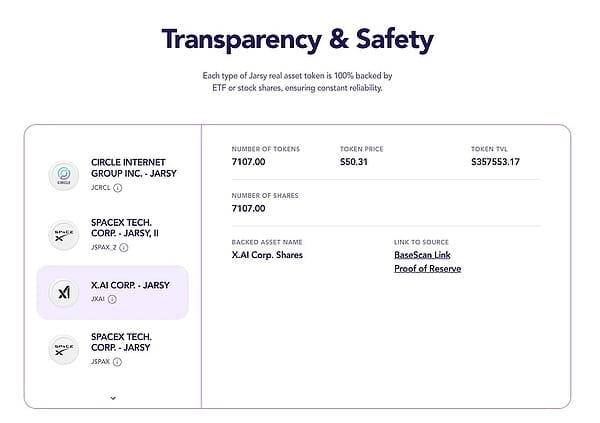

Jarsy adopts a 1:1 asset-backed tokenization model. Its core mechanism is to directly acquire Pre-IPO shares and issue tokens on a 1:1 basis. For example, if Jarsy holds 1,000 shares of SpaceX stock, it mints 1,000 JSPAX tokens. Although investors do not directly hold the underlying stocks, they enjoy all related economic rights — including dividends and capital appreciation.

The model relies on Jarsy operating as an asset management entity: the platform first estimates market demand via presale tokens, then pools funds to acquire shares. If the acquisition is successful, presale tokens convert to formal tokens; if unsuccessful, refunds are issued. All assets are held by a special purpose vehicle (SPV) and real-time verification is achieved through a reserve proof page.

The platform will also significantly lower the investment threshold to start from $10. There are no qualification requirements for investors outside the United States, greatly enhancing global accessibility. All transaction records and asset holdings are stored on-chain, ensuring auditability and transparency.

However, this model faces structural limitations. The most pressing issue is insufficient liquidity, stemming from the limited holding sizes of various companies. For instance, Jarsy currently holds approximately $350,000 in X.AI, $490,000 in Circle, and $670,000 in SpaceX. In such shallow markets, even small sell orders from large holders could trigger significant price fluctuations. Given the opacity and illiquidity characteristics of private equity, price discovery is already difficult, which further amplifies volatility.

Moreover, while asset-backed tokenization provides stability, it sacrifices scalability. Each new token launch requires actual share acquisition — a process involving negotiations, regulatory coordination, and potential procurement delays, which limits the platform's responsiveness to rapidly changing market trends.

It is worth noting that Jarsy has only been online for just over a year and is still in its early stages. As the user base and assets under management (AUM) grow, liquidity issues may gradually ease. When the platform achieves scale expansion, a broader coverage and deeper pool of tokenized equities will naturally cultivate a more stable and efficient market.

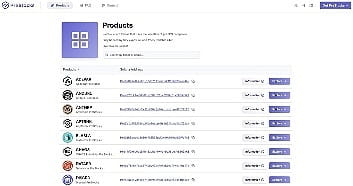

(3) PreStocks

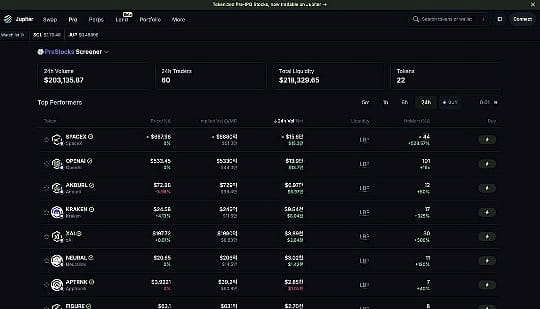

PreStocks adopts a similar operational model to Jarsy, acquiring shares of non-listed companies and issuing tokens backed on a 1:1 basis. The platform currently supports trading of 22 Pre-IPO stocks and recently opened its products to the public.

PreStocks, built on the Solana blockchain, implements trading functionality through integration with Jupiter and Meteora. It provides 24/7 trading and instant settlement services without management fees or performance commissions. There is no minimum investment threshold, and any user with a compatible Solana wallet can participate — significantly lowering the barriers to entry.

However, there are specific limitations: users from the United States and other major jurisdictions cannot use the platform. Although the platform claims that all tokens are fully collateralized by the underlying stocks, detailed holding verification documents have not been publicly disclosed. The team states that they will regularly release third-party audit reports and can provide paid single-holding verification services upon request.

Compared to Jarsy, PreStocks has a closer integration with decentralized exchanges (DEX), which may foster broader secondary application scenarios (such as token staking and lending). In the Solana ecosystem, tokenized public equity (such as xStock) has formed active usage scenarios, and PreStocks may benefit from synergistic effects at the ecosystem level.

(4) Barriers to Pre-IPO stock tokenization need to be broken.

The tokenized equity market has begun to take shape. Although platforms like Ventuals, Jarsy, and PreStocks show early developmental momentum, significant structural challenges remain.

The primary obstacle is regulatory uncertainty.

Most jurisdictions still lack a clear legal framework for tokenized securities. Therefore, many platforms operate in a regulatory gray area, maintaining operations without direct compliance through jurisdictional arbitrage.

Secondly, resistance from private enterprises remains a key barrier.

In June 2025, Robinhood announced it would launch tokenized exposure services for companies like OpenAI and SpaceX for EU customers. OpenAI immediately issued a public statement opposing this: 'These tokens do not represent equity in OpenAI, and we have no partnership with Robinhood.'

This response highlights private enterprises' desire to control equity structures and investor management — which is a core function they fiercely protect.

Thirdly, the complexity of technology and operations cannot be ignored.

Maintaining a reliable connection between real assets and tokens, addressing cross-border compliance, handling tax implications, and implementing shareholder rights enforcement are all challenging tasks. These issues could severely constrain user experience and scalability.

Despite various limitations, market participants are still actively seeking solutions. For example, Robinhood, despite facing public criticism, claims it plans to expand tokenized assets to thousands by the end of the year. Platforms like Ventuals, Jarsy, and PreStocks are also continuously advancing differentiated paths for tokenizing equity access.

In short, tokenization provides a viable path to improve accessibility to private equity, but this field is still in the early stages. Various limitations currently exist, but the development history of the crypto space indicates that technological breakthroughs and rapid market adaptation can — and often will — redefine the boundaries of possibility.