The Ethereum treasury strategy company The Ether Machine (hereafter referred to as ETHM) announced on August 4 that it has increased its holdings by 10,605 ETH, bringing its total Ethereum holdings to 345,362 ETH, valued at approximately $1.27 billion. This is the second large increase within less than half a month since the company went public.

As a company focused on Ethereum investment, ETHM announced in July that it would go public on NASDAQ, initially planning for 400,000 ETH, with a market value of nearly $1.6 billion. By the end of July, the company had already made an additional purchase of 15,000 ETH.

The aggressive expansion of The Ether Machine coincides with a critical period when multiple public companies are competing to purchase ETH. With an increasingly clear regulatory framework, more and more public companies will include ETH in their asset allocation.

Armed with $1.6 billion in ammunition, entering the Ethereum DAT arms race.

The Ethereum treasury track has become a battleground for institutions. ETHM's listing ignited this competition—within just two weeks, the entire landscape of the track underwent a dramatic transformation.

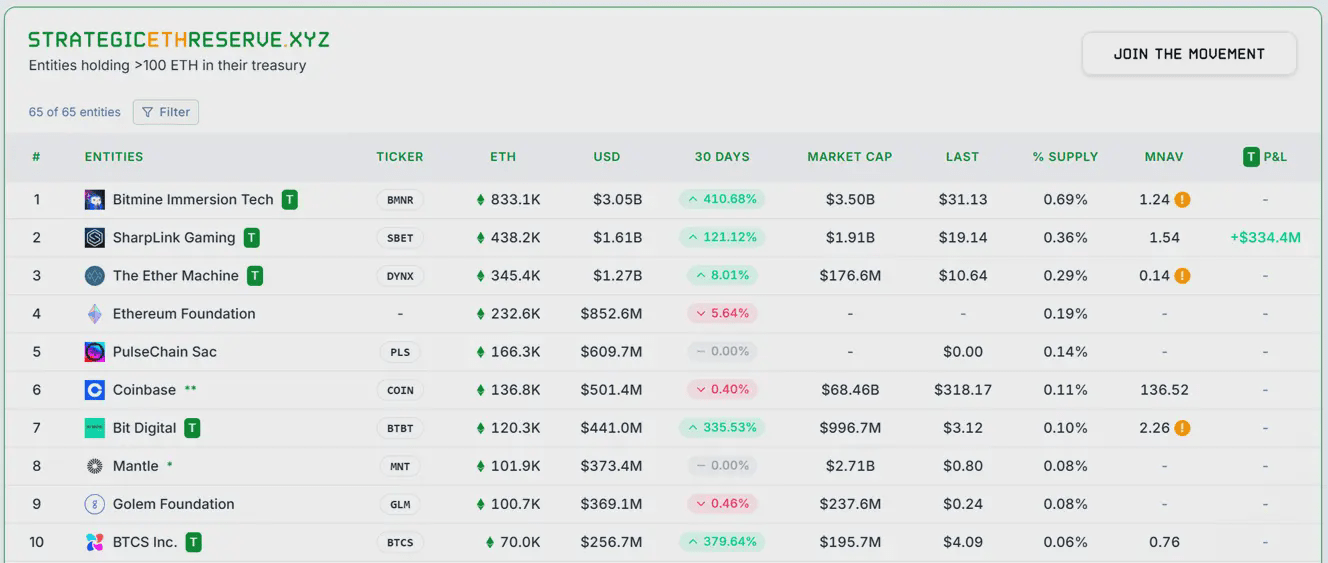

According to official reports, when ETHM announced its listing on July 21, BitMine and SharpLink's ETH reserves were only 300,000 and 280,000, respectively, both below ETHM's planned initial scale of 400,000. However, by August 5, BitMine's holdings had skyrocketed to 833,000 (valued at $3 billion), an increase of 177%, taking the lead; SharpLink also did not lag behind, with on-chain data from Nansen showing its reserves reached 498,000 (valued at $1.8 billion), an increase of 78%, ranking second, and publicly announced plans to aim for 1 million. Even former Bitcoin miner Bit Digital urgently pivoted, accumulating 120,000 ETH.

Image source: Strategic ETH Reserve (SBET data not yet updated)

This wave of crazy accumulation confirms Standard Chartered's prediction: treasury companies have purchased over 1% of the circulating ETH supply, a ratio that could soar to 10%. A multi-billion dollar arms race is escalating.

In this heated competition, The Ether Machine has emerged with a unique advantage of capital + strategy. First, the nearly $1.6 billion initial capital provides robust ammunition—Andrew Keys personally invested $645 million in ETH, and institutions like Pantera Capital pledged over $800 million in financing. But this alone is not enough to allow it to surpass others.

An even more critical advantage lies in its differentiated approach. While competitors are still frantically hoarding coins to capture market share, ETHM has already increased its yield to 4-5.5% through re-staking and DeFi protocol combinations. In a low-interest environment, this stable high yield has become a killer feature to attract institutional funds.

Annualized 4-5.5%, breaking down ETHM's golden strategy.

To understand how The Ether Machine achieves 4-5.5% annual returns, one must grasp its core positioning—a company that generates Ether.

This concept can be likened to the oil economy: traditional crypto investment is like buying crude oil and hoarding it for a price increase; while The Ether Machine chooses to become an oil company, generating cash flow from the asset itself.

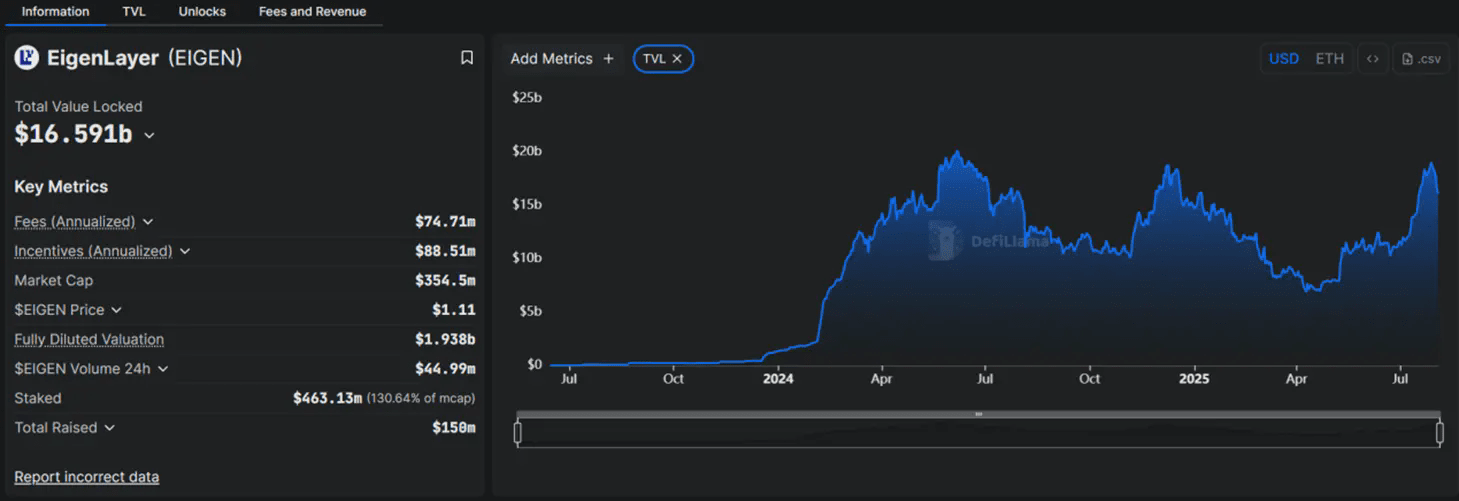

Keys and his team discovered that ETH is not just an asset, but also a production tool. Through the EigenLayer protocol, staked ETH achieves multiple benefits—providing security for the Ethereum mainnet while simultaneously serving protocols like oracles and cross-chain bridges, with each service generating additional income.

Just like bank deposits can earn interest while also working to earn extra income. EigenLayer's total locked value of $16.591 billion confirms the attractiveness of this model, and The Ether Machine has become one of the largest institutional participants in that ecosystem.

In addition to re-staking returns, the company also gains returns by participating in DeFi protocols. When the basic staking yield for ETH is only about 3%, this combination strategy raises total returns to 4-5.5%.

Thus, ETH has transformed from a static asset waiting for appreciation to a productive asset that continuously creates value.

ETHM is not the next MicroStrategy.

The market always likes to find a reference point. When The Ether Machine appeared, almost everyone was asking the same question: Is this the next MicroStrategy?

Perhaps people tend to use yesterday's framework to understand today's innovations.

Indeed, on the surface, both companies seem to be doing the same thing—holding a large amount of crypto assets as a public company. But upon closer observation, you'll find that these are two completely different approaches.

MicroStrategy's logic is straightforward and crude. Issue bonds to buy Bitcoin, betting that the price will rise to cover interest. However, this model's efficiency is rapidly declining. In 2021, MicroStrategy could generate one basis point of return for shareholders with every 12.44 BTC. By July 2025, it would take 62.88 BTC to achieve the same result. The scale has expanded fivefold, yet efficiency has dropped to one-fifth.

In contrast, The Ether Machine is taking a different path. Through staking and DeFi participation, ETH generates approximately 5% annual cash flow each day. There is no need to wait for the price to rise or pray for a bull market—this is real income, not paper wealth.

The fundamental difference lies in asset attributes: Bitcoin is digital gold, with its value stemming from scarcity and consensus. Ethereum is digital infrastructure, with its value lying in its ability to support the operation of the entire ecosystem.

We can now trace back the history from the MicroStrategy era and find that we are experiencing the third phase of evolution towards a crypto treasury.

Phase One: Pioneer Dividend Period (2020-2023) At that time, MicroStrategy, which was not well regarded, proved that public companies could gain a premium by holding crypto assets.

Phase Two: Model Replication Period (2024-2025) Successful imitators emerge. The stock price of the imitator SharpLink soared 4000% before plummeting 70%. Marathon Digital and Riot Platforms followed suit, but with poor results, exposing the risks of a simple hoarding model.

Phase Three: Model Evolution Period (2025-) The new model represented by The Ether Machine—not hoarding assets, but operating assets, creating diversified income sources.

However, achieving this evolution from accumulating assets to operating assets is no easy feat. It requires not only a deep understanding of the crypto world but also experience navigating the compliance labyrinth of traditional finance.

Four key operators behind the giant.

The Ethereum Avengers—when the chairman of The Ether Machine used this term to describe the team, it was not a joke. This group of well-connected avengers is attempting to reshape the landscape of institutional crypto investment.

The story begins with the forge of the Ethereum ecosystem, ConsenSys. It was there that Andrew Keys first met David Merin. At that time, they had no idea they would be deeply bound to the world's top financial institutions.

In 2017, during the crypto winter following the ICO bubble burst, the entire industry was filled with despair. At this moment when everyone was fleeing, Andrew Keys sought to open the doors of Microsoft and JPMorgan with Ethereum.

They look at Andrew Keys as if he's a madman selling a perpetual motion machine.

But he did not give up. After numerous rejections and explanations, skepticism gradually turned into curiosity. Ultimately, he founded the Enterprise Ethereum Alliance (EEA), bringing the term Ethereum into the boardrooms of the Fortune 500 for the first time.

Meanwhile, David Merin pushed for commercialization within ConsenSys, leading over $700 million in financing and acquisitions.

The two realized in countless late-night discussions that the divide between traditional finance and the crypto world is not only prejudice but also a tangible compliance gap.

Countless institutions are interested in Ethereum, but ultimately stop due to the lack of reliable investment tools.

This pain point prompted them to make a bold decision: to no longer be mere evangelists, but to personally get involved in creating a regulated financial vehicle.

Keys' first move shocked everyone—he used over $600 million of personal ETH as initial investment. If I don't believe it myself, how can I expect others to believe it?

His all-in stance demonstrated his determination to everyone. In a later CNBC interview, he explicitly stated: I would rather have an iPhone than a landline. This metaphor aptly explains why he only bets on Ethereum.

Soon after, the team began to assemble. They found Darius Przydzial, a dual-faced individual who had managed traditional risk at Fortress and was a core contributor to the DeFi protocol Synthetix.

His task is very clear: to strike gold in the wild west of DeFi while staying alive.

For technical security, Tim Lowe, who has twenty years of banking system experience, joined the team. Ultimately, the arrival of PayPal board member and former Icahn Enterprises executive Jonathan Christodoro provided the final endorsement for the company's governance structure.

Internal team dynamics have not been smooth. Traditional finance advocates for conservative stability, while crypto natives lean towards radical innovation. After numerous meetings and debates yielded no results, keys made a decisive statement: we are not choosing a side; we are to become a bridge connecting both sides.

This statement has become the unchanging core philosophy of The Ether Machine.

Vitalik's call: We should not be chasing large institutional capital at full speed.

If the idealism represented by the Ethereum Foundation, which centers on technology and community, constituted ETH's first lifeline, what we are witnessing now is the natural evolution and transition of this lifeline: as EF gives way to capital, ETH's second lifeline has already begun.

This new lifeline may not deviate from its original intention, but it will undoubtedly lead Ethereum into a more complex deep water area. The question is, what will Ethereum become in the process? What risks will it face?

The first and foremost risk is technical: smart contract vulnerabilities and staking penalties could lead to a 100% loss of ETH, coupled with weeks-long unlocking periods, liquidity becomes a luxury. When a single entity controls a large amount of ETH, are we reinforcing Ethereum or fundamentally changing its nature?

Subsequently, community opinions showed clear divisions. A comment from @azuroprotocol accurately captured this anxiety: from building a decentralized Ethereum to selling 400,000 ETH to enterprises, it has ultimately evolved into Web3 becoming Wall Street 2.0.

Even Vitalik has issued a warning: we should not be chasing large institutional capital at full speed. Now, with 70% of staked ETH concentrated in a few pools, is his concern becoming a reality?

At the same time, when prices rise, who still cares about decentralization? @agentic_t has hit the nail on the head regarding the community's core dilemma. The 4%-5.5% staking yield seems enticing, but history tells us that all excess returns will ultimately be arbitraged away.

Similarly, although Keys believes Ethereum has become the biggest beneficiary of the GENIUS Act, the spring of regulation seems to have arrived. But what happens after spring? When the policy direction changes, will these institutional efforts become targets of regulation?

A mark of maturity, or the end of ideals?

Perhaps every successful technology ultimately moves towards institutionalization. The internet, mobile payments, and social media have all undergone this process.

As Ethereum transitions from an idealistic experiment to an investment product embraced by Wall Street, is this a mark of maturity or a departure from its original intention?

Time will provide the answer.