Author: Les Barclays

Translated by: Shaw Golden Finance

In this article, I will analyze what I believe to be one of the most important financial developments happening right now... the new stablecoin legislation and its potential role in helping the U.S. manage national debt, maintain the dollar's dominance, and exert pressure in global markets. In my view, this is not just about cryptocurrency regulation, but also closely tied to the bond market, yield curves, macroeconomic strategies, and the broader geopolitical games being played behind the scenes.

If stablecoins are incorporated into the U.S. fiscal and monetary policy framework, their impact will be significant not only in the cryptocurrency space but also on global trade, manufacturing, debt issuance, and monetary policy. This could enable the U.S. to rebuild domestically at a lower cost, increase financial pressure on competitors, and attract funds back to the U.S. system.

What is the (GENIUS Act) (and why now)

Stablecoins can be viewed as digital dollars that always have a value of exactly 1 dollar. Currently, there are no clear rules on who can issue stablecoins and how they should operate, which raises concerns about their safety.

(GENIUS Act) (Senate version): This bill establishes a regulatory framework for payment stablecoins (digital assets that must be redeemed at a fixed currency value by the issuer). Under this bill, only licensed issuers can issue payment stablecoins. One can think of it as needing a special license to print digital currency.

Key Differences

Who is responsible: The Senate version centralizes regulatory authority in the Treasury, while the House distributes power among the Federal Reserve, Comptroller of the Currency, and other agencies.

Rulemaking: According to the Senate's (GENIUS Act), only the Office of the Comptroller of the Currency (OCC) has the authority to issue these rules. The House's (STABLE Act) would impose more requirements and involve multiple agencies working together.

Both aim to:

Safety First: Only approved companies will be allowed to issue stablecoins, akin to how only licensed banks can hold your funds.

Consumer Protection: This legislation will restrict the issuance of payment stablecoins within the U.S. to 'approved payment stablecoin issuers.'

Market Clarity: Aimed at regulating the approximately $238 billion stablecoin market, creating a clearer framework for banks, companies, and other entities to issue digital currencies.

Current Status: The (GENIUS Act) passed with a vote of 308 in favor and 122 against. The U.S. House of Representatives passed the (Guidance and Establishment of a National Innovation Act for U.S. Stablecoins) (referred to as the 'GENIUS Act') on July 17, 2025, sending this landmark legislation to President Trump for signing. Thus, the Senate version (GENIUS Act) ultimately prevailed and officially became law, becoming the first cryptocurrency bill to gain approval from both houses of Congress.

Essentially, both bills aim to set 'traffic rules' for the digital dollar, but there are disagreements over which government agencies will serve as 'traffic cops.'

The House's (STABLE Act) and the Senate's (GENIUS Act) are two opposing bills, but they share a common goal: to bring stablecoin issuers under regulatory oversight and clarify how much capital, liquidity, and risk management is sufficient. They also aim to clarify which federal or state agencies will act as arbitrators. But there’s a less prominent potential subplot: how widespread acceptance of stablecoins by global traditional institutions could affect the $28 trillion U.S. Treasury market.

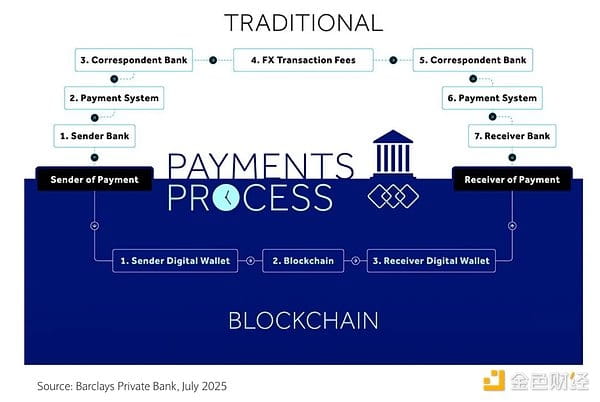

How stablecoins could become latent demand for Treasuries

The situation is this: Treasuries are the backbone of stablecoin reserves because, in terms of safety and liquidity, there are almost no other assets that can compare. If you offer a digital dollar, you need to back it with the closest thing to risk-free assets possible. This sounds a lot like the hundreds of money market mutual funds issued by giants like BlackRock, Fidelity, and Vanguard, which hold over $6 trillion in assets, most of which are U.S. Treasuries. However, unlike the money market funds issued by Fidelity that may offer a 4% annual yield, most stablecoin issuers have so far refused to provide any yield or income to their holders. That is also why the largest stablecoin issuer, Tether, has extremely high profit margins and reported over $1 billion in operating profit in the first quarter of 2025. It indeed sets many standards for reserves, audits, disclosures, and anti-money laundering (AML) compliance as it seeks to address many concerns surrounding illegal activities. It also involves restrictions on marketing stablecoins as legal tender while prohibiting payments of yields or interest to individuals holding stablecoins, as this would significantly undermine the banking industry.

One thing I have been observing for a while (but unfortunately haven't discussed with anyone) is the relationship between stablecoins, U.S. Treasuries, and the Treasury Department. And I believe this is why the government is pushing for stablecoins first rather than other matters.

In the chart below, there is one thing I want to highlight:

The reason I emphasize this now is that stablecoins could be one of the largest buyers of U.S. Treasuries, which would lower bond yields. In short, through stablecoins, you can normalize the yield curve, which I believe is exactly what the Trump administration wants to execute, as both Trump and Besant (whom I will discuss later) are concerned about national debt and the amount that needs to be refinanced by the end of the year.

Perspective from Treasuries

I think this is an interesting way to reduce debt interest payments, and the reason it is extremely compelling is that it will allow the U.S. to refinance Treasuries at lower yields, ultimately making it much easier to finance Treasuries.

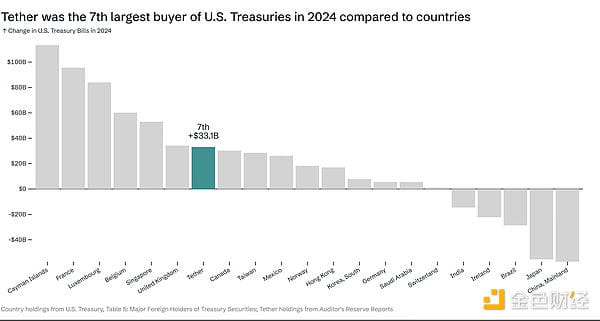

Now, let’s discuss the situation of stablecoins relative to other countries. In 2024, Tether is the seventh largest buyer of U.S. Treasuries, compared to other countries buying U.S. debt. Imagine how much U.S. Treasuries Tether (or Circle or other entities) could purchase within this framework. There are some concerns surrounding stablecoins and central bank digital currencies, and other bills or proposals are being drafted and passed regarding the U.S. not supporting central bank digital currencies. You could speculate that Tether or Circle might be disguised as central bank digital currencies, but that’s a completely different topic, and I won’t delve into it. What I want to emphasize is the impact of stablecoins on national debt.

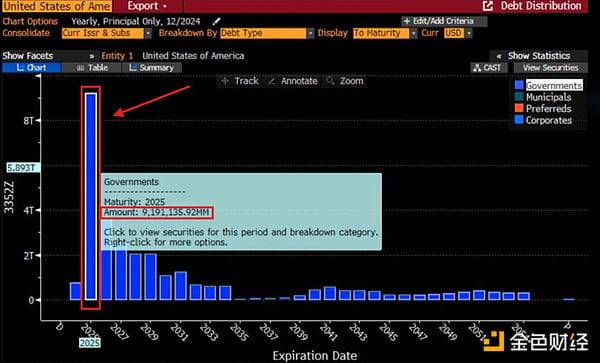

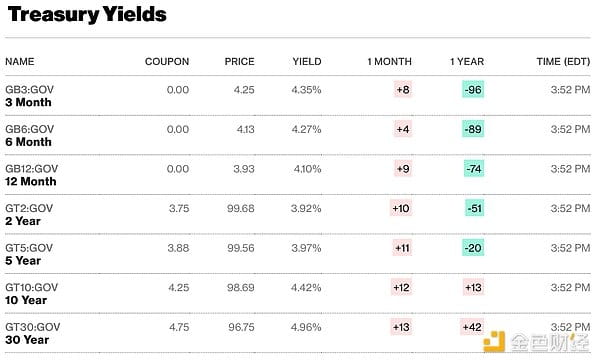

The Federal Reserve currently holds about 40% of Treasury bonds, which will need to be rolled over at new interest rate levels. The maturity dates of these bonds are in 2025 and 2026. Below, I will attach a chart of U.S. short-term Treasury rates for reference.

Currently, depending on the term being examined, our debt rate is roughly between 4% and 5%. If this is short- to medium-term debt and rolled over at the above rates, it will become very unsustainable, leading to a debt spiral. If stablecoins become one of the largest buyers of U.S. Treasuries, they can lower yields, and they will do so, especially in the short term. That is why I think short-term demand, particularly for short-term Treasuries, is very noteworthy because it means they will essentially become one of the largest buyers of short-term Treasuries and significantly alleviate the pressure of U.S. national debt.

U.S. Treasury Secretary Scott Besant discussed the U.S. desire to be a leader in the digital asset space in an interview, using it as a means to exert pressure in global markets.

Clearly, Besant is an advocate for stablecoins. What couldn't be discussed a few months ago is that you don't want to show your action plan to your opponents. I'm glad he is one of the few who has figured out what the adoption of stablecoins in the U.S. might mean—given his background, it's not surprising for those who know him and work in finance. I think he has a very advanced understanding compared to what stablecoins might be or what it means for the U.S. Treasury market.

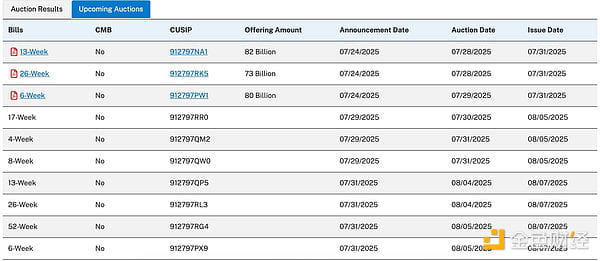

The U.S. Treasury is issuing different types of bonds, and on July 21, they auctioned $82 billion in 3-month Treasuries, and the auction went very well. These are things that everyone involved in finance or investment should pay attention to.

These auctions are very important as they reflect the interest of investors (including domestic and foreign investors) in purchasing U.S. Treasuries. I also believe that Powell's current approach is correct, in that he is not rushing to lower interest rates, not only because economic data indicates so, but also because when interest rates remain high—especially since the U.S. is the driver of the global economy—it disrupts the stability of many other economies, particularly in Asia, Europe, and South America. I say this because when interest rates are high, it actually attracts liquidity back to the dollar as investors seek safe havens. I think currently, they want to force other countries' currencies to realign with the dollar. So they can take action in the bond market by keeping interest rates high. This could severely undermine these countries' economies and/or currencies from a financing perspective, as the capital cost of non-dollar-denominated currencies would become higher, making it more difficult to incur debt. Therefore, those other countries would have to liquidate a large number of assets to fund themselves and stabilize their economies.

When a country faces fiscal distress—regardless of how it got there—it is forced to sell assets to stabilize its economy, and I am sure the Trump administration is aware of this and is leveraging it.

Scott and the entire U.S. government seem to be dissatisfied with Europe. They could have forced many countries to align with U.S. policies and everything proposed through means like tariffs and the bond market, but the bond market is extremely important.

Financial Stability or Digital Vulnerability?

Now, if the U.S. pushes for stablecoin legislation while engaging in tariff negotiations and trade agreements, I think many factors will converge, and domestic pressures in Europe and Asia will mount, potentially even triggering some form of credit event that could lead to a stock market decline, prompting everyone to rush back to U.S. Treasuries. It depends on how quickly and at what scale stablecoins can develop because if they grow too fast and too much, we may encounter some liquidity events (like the 2008 to 2009 money market fund run, or even the brief decoupling of Tether from the dollar in 2022), possibly leading to liquidity spiral dynamics, such as stablecoin redemptions forcing the sale of short-term Treasuries.

In my view, some type of event does need to happen. It's like a compressed spring or a ball underwater. The deeper you press the ball, the more it wants to surface. This is the situation we see with Japanese government bonds and the UK's debt market, etc.

An article written by a friend of mine at Barclays discusses several key adoption risks of stablecoins. Stablecoins are digital assets designed to maintain a stable value relative to a reference asset. The main adoption risks highlighted in the article include:

Regulatory Uncertainty: Stablecoins face significant regulatory scrutiny as regulators attempt to address issues surrounding their use, investor protection, and risks to financial stability. In the absence of a clear regulatory framework, issuers, users, and financial institutions looking to incorporate stablecoins into their operations face ongoing uncertainty.

Operational Resilience: The underlying technological framework of stablecoins, including smart contracts and supporting blockchain, must demonstrate strong stability, scalability, and security. Operational risks arising from disruptions, technical failures, and cyberattacks could undermine trust and usage.

Consumer Protection and Trust: Users must trust that the tokens are fully backed by reserves and can be redeemed at the promised value. Insufficient transparency or poor reserve management can undermine confidence, leading to value loss for holders or other issues.

Integration with Existing Systems: The adoption of stablecoins may be hindered by the challenges of integrating new digital assets with traditional payment, banking, and financial market infrastructure. Achieving the advantages of stablecoins at scale will require seamless interoperability.

Systemic Risk: If poorly designed or inadequately regulated stablecoins are widely adopted, they could pose new systemic risks to the broader financial system, especially if they hold a significant share in payments or deposits.

These risks indicate that despite the bright prospects for stablecoins, their widespread use depends on clear regulatory standards, robust technology, transparent reserve management, and successful integration with the existing financial ecosystem.

The Politics of Quiet Monetization

Shashank Rai describes a phenomenon that can be referred to as 'quiet monetization'—how stablecoins create a significant increase in demand for U.S. Treasuries without expanding traditional government debt. Here’s how it works:

Stablecoin issuers must fully back their tokens with liquid assets (mostly short-term U.S. Treasuries). As of early 2025, stablecoin issuers held over $120 billion in U.S. Treasuries, a number expected to reach $1 trillion or more by 2028. This creates what they describe as 'a structural and persistent source of demand for short-term U.S. Treasuries, even as the market becomes increasingly cautious regarding U.S. fiscal policy and long-term debt.'

The UK has been slow to act in establishing the necessary regulatory certainty around stablecoins. Stablecoins are an expensive form of currency. They are costly because they limit the monetary transmission mechanism (thereby reducing economic growth). They are costly because they increase the volatility of Treasuries (and the dollar) and heighten term premiums. They are costly because they fragment liquidity. They are costly because most of them yield lower returns than money market funds. They are costly also because blockchain transaction costs are an order of magnitude higher than domestic payment systems.

Stablecoins are a higher-risk form of currency. The risk lies in their use of an atomic swap model rather than a fiat currency model. The risk also lies in their KYC processes, which are subject to much less regulation. Additionally, there is a concentration risk around miners on the blockchain.

As a competitive form of currency, they should receive regulatory certainty and be brought under regulatory oversight (which differs from the EU’s approach, as the EU over-regulates, repeating the mistakes it made in the retail forex market, driving that market offshore). However, the structure of stablecoins should not (as in the U.S.) undermine the stability of the banking system or erode public confidence in the currency. Stablecoins that are properly regulated and operate within the regulatory framework will be able to interoperate completely with cash. In a capital market environment, this will ultimately eliminate most stablecoins. Efficient markets, efficient liquidity, and programmable money do not require blockchain-based stablecoins.

A good regulatory structure for stablecoins needs to include:

Redemption/Liquidity Real-time Reporting - Daily Net Asset Value Reports

Regulatory Capital Based on RWA Models (like money market funds or banks)

Minimum Short-term Liquidity Ratio (24-hour).

Periodic Requirements for Transparent Internal Audits (systems and processes) - Senior Personnel System (key decision-makers must be qualified).

CRO's Duty of Attention to Regulators.

Stablecoin issuers should be able to access the central bank's real-time gross settlement system, repo market, and obtain central bank funds just like banks do during periods of market stress. However, there should be no regulations regarding the asset composition of stablecoins (aside from meeting short-term liquidity needs). Transparency should be maintained, and the market should decide.

The Effect of 'Offshore Quantitative Easing'

The concept of 'offshore quantitative easing' refers to how stablecoins create demand for dollars globally without the Federal Reserve needing to print more money.

As stablecoins are market-driven, users tend to choose the most stable and widely accepted stablecoins, which naturally favors strong currencies (primarily the dollar) while potentially excluding weaker national currencies. With the proliferation of stablecoins, especially in emerging markets, the process of dollarization may further intensify.

The author believes this will create 'a new game of dollarization', where 'the rapid and low-cost liquidity of stablecoins may marginalize weaker currencies, further entrench the dominance of the dollar, and reshape the international financial landscape by making the dollar more accessible and liquid in cross-border transactions.'

Unlike traditional quantitative easing (QE) where central banks openly expand the money supply, this operation is achieved through private market forces—stablecoin companies automatically purchase Treasuries to back their tokens, thereby creating demand for Treasuries without government intervention.