In the DeFi space, there has always been a structural gap in the fixed income market — the lack of a credible, decentralized interest rate pricing benchmark. In traditional finance, benchmark rates like LIBOR or SOFR serve as pricing anchors for financial products such as bonds and derivatives, while the blockchain world has long relied on centralized oracles or self-operated data from single protocols. The DOR (Decentralized Oracle Rate) model proposed by Treehouse Labs may be opening a new door.

DOR Mechanism: From Game Theory to Interest Rate Discovery

Treehouse's core innovation is transforming interest rate pricing into a carefully designed game. Its DOR model achieves data credibility through a three-tier role division: Professional panel members (Panelists) submit interest rate data or predictions and must stake TREE or tAsset as a "integrity margin"; Operators (currently only Treehouse itself) initiate interest rate queries and maintain the data process; Delegators participate in profit distribution by delegating tAssets to specific Panelists; Referencers are the protocol parties that ultimately use the data. This design essentially replaces traditional financial authoritative certification with economic games — when the accuracy of the data is directly related to the profits and losses of staked assets, the cost of malicious manipulation will far exceed the benefits.

The first product TESR (Treehouse Ethereum Staking Rate) curve has shown practical value. The annualized yield in the Ethereum liquid staking market has long had a protocol-level difference of 3%-5%, while TESR aggregates real-time data from mainstream LSD protocols (such as Lido, Rocket Pool) to provide a verifiable benchmark for derivative pricing and lending rate calibration. According to community testing phase data, the prediction error rate for ETH staking yield by Panelists has been compressed to within ±0.8%, far exceeding the accuracy of most centralized oracles.

TREE Token: Spiral Structure of Value Capture

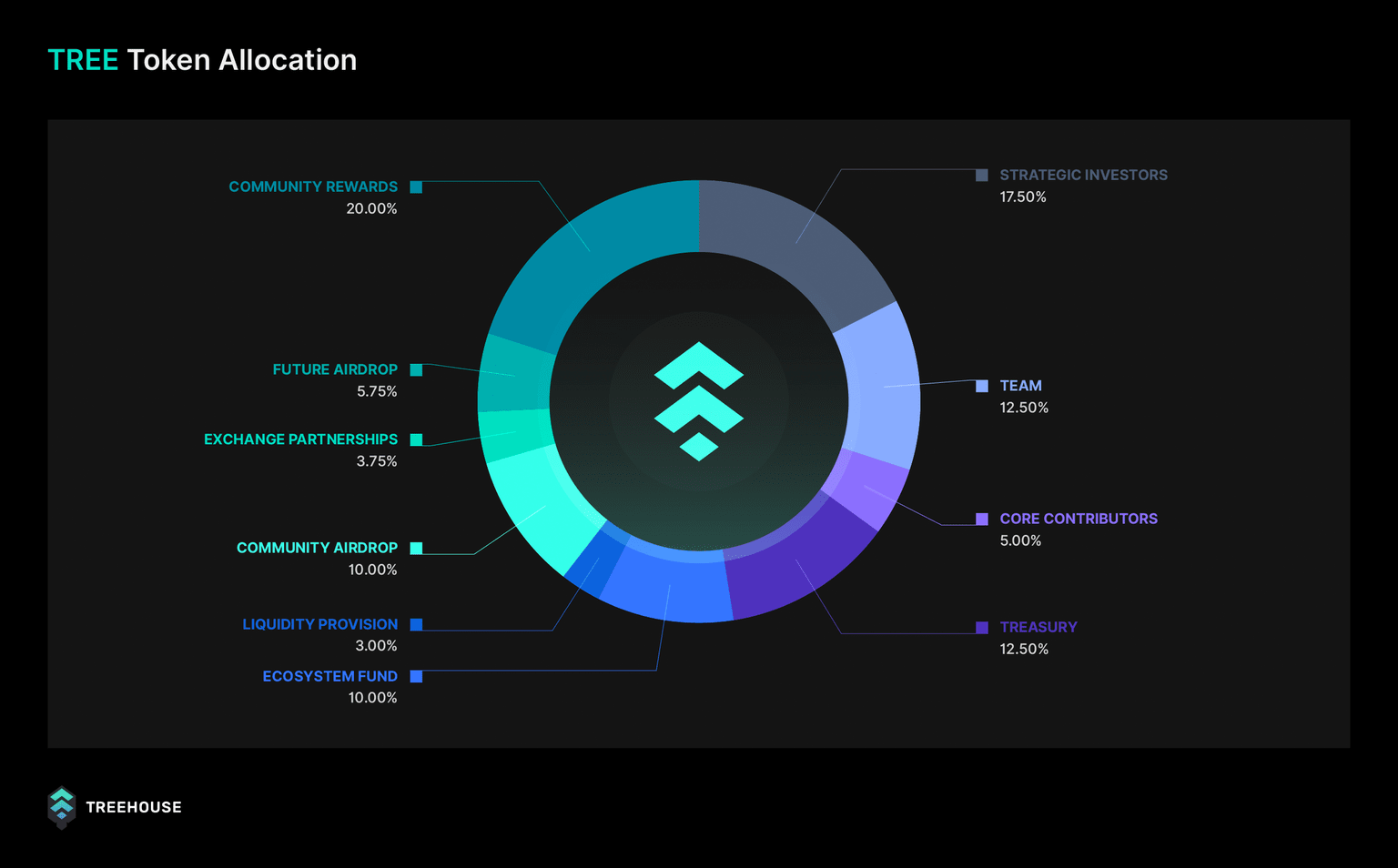

The economic model of TREE exhibits typical characteristics of a "tool asset." Its value support comes from multiple scenarios:

- Data Usage Fee: Referencers must pay TREE each time they call DOR data, with fees dynamically adjusted by the DAO. According to the documentation, the initial fee rate is set at 0.5 TREE per thousand queries, equivalent to about $1.2 when converted based on Ethereum mainnet Gas prices, which is 30%-40% lower than traditional oracles like Chainlink;

- Rigid Demand for Staking: Panelists must stake TREE to participate in predictions, and the amount staked is positively correlated with the weight of the data they can submit. Early testnet data shows that leading Panelists have an average staking amount of 12,000 TREE;

- Governance Premium: Key parameters such as the staking coefficient, penalty threshold, etc., are decided through voting by TREE holders. This design gives the token both "license" and "equity" attributes.

It is worth noting that Treehouse adopted a progressive distribution strategy during its cold start phase. Real users are filtered through the GoNuts activity (the anti-witch mechanism requires proof of on-chain activity), combined with the priority allocation of TSC NFTs, to ensure the early community has sufficient governance capability. This "contribution proof" is more effective at retaining active users than simple airdrops — as of July 25, over 23,000 addresses have accumulated Nuts, but only 37% passed the anti-witch verification.

The Imagination Space of On-chain Benchmark Interest Rates

The scale of the fixed income market has always been proportional to the credibility of interest rate benchmarks. The long-term value of Treehouse lies not only in the current staking rate pricing of Ethereum but also in its scalable architectural design. The DOR model theoretically supports the construction of any interest rate curve, such as:

- Government Bond Yield Curve: Introduces traditional interest rates such as US Treasury and German bonds on-chain to provide pricing references for RWA products;

- Cross-chain Interest Rate Differential Index: Captures the interest rate differences between different chains to help optimize the efficiency of arbitrage strategies;

- Volatility Surface: Derivative protocols can develop more complex interest rate options products based on this.

Given that the LSD track has gathered over $18 billion in TVL, if Treehouse can occupy the "infrastructure layer" of interest rate benchmarks, its moat will naturally deepen with the increasing frequency of data usage. As more protocols rely on DOR data like they do with Uniswap TWAP, the value capture ability of TREE will enter a positive feedback loop.

Compared to similar protocols like UMA or API3 (currently valued at approximately $480 million and $120 million respectively), Treehouse's differentiation lies in its accuracy and scalability in vertical domains. If its Ethereum staking rate data is adopted by mainstream protocols like Aave and Frax, then TREE's "data tax" model could open up a new valuation paradigm. After all, in the traditional financial world, the Intercontinental Exchange (ICE) earns over $300 million annually from operating LIBOR — what the blockchain may need is a decentralized ICE.