Author: 0xWeilan

In the June report, we pointed out that due to sufficient washout and a significant amount of chips entering the hands of institutions, the next rally may be completed quickly in the short term. We originally expected this breakthrough to occur in August or September, but if expectations for rate cuts drive proactive buying, or structural allocation accelerates, there is a possibility that the rally could be brought forward to July.

The market rose as expected, and we saw this expectation realized rapidly in July. BTC rose 8.01% for the month and tested the historical high of $120,000.

Behind this are the exuberant corporate purchases and continuous inflows from ETF and stablecoin channels forming material support. However, expectations for rate cuts and the actual situation of the tariff war have changed significantly, suppressing the rapid surge in prices and temporarily interrupting the unfolding of Altseason. There are still many uncertainties regarding whether rate cuts can occur in September.

Since 2023, U.S. individual investors and businesses have gradually increased their allocation to crypto assets represented by BTC, and by November 2024, after Trump is elected as the 47th President of the United States, BTC will be established as a national strategic reserve, prompting a series of crypto-friendly policies to be implemented, marking a complete departure from the wild years for crypto assets and the blockchain industry.

However, deep participants in the crypto market face a starkly contrasting situation. On one hand, BTC is being increasingly accumulated by new funds, pushing prices to new levels; on the other hand, Altseason seems never to return, with Ethereum, seen as the cornerstone of the blockchain industry, being driven down to $1,300 in April, below the price at the beginning of this bull market, causing insiders to lament the 'collapse of faith.' However, ETH rebounded rapidly by 48.80% in July.

EMC Labs believes that the crypto industry is at a historical turning point, with complex structural changes and secretive trends that insiders have never seen before, thus presenting significant challenges. The factors determining asset prices have undergone enormous changes, transitioning from previously supply-demand cycle reductions and speculative booms to a new asset allocation logic in the chessboard of all asset types.

We are in the midst of a massive industrial transformation.

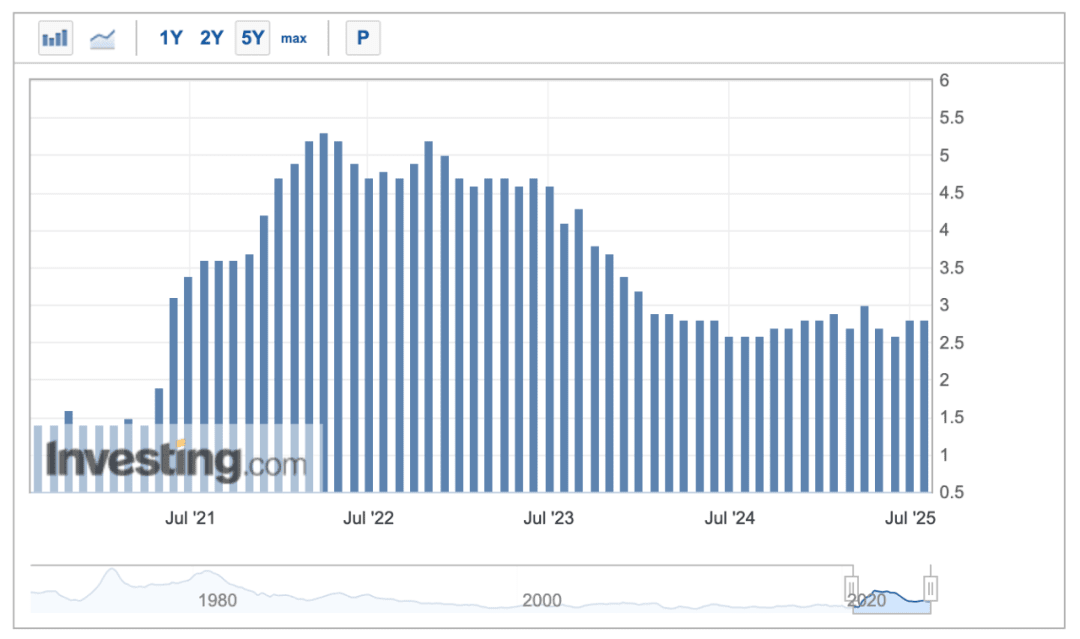

Macroeconomic Finance: Inflation rebound vs. weak non-farm employment.

In July, the U.S. capital market was primarily controlled by the interplay of three variables: 'when the Federal Reserve will restart rate cuts + how the tariff war will conclude + the performance of economic and inflation data.' A slightly frenzied forward-looking trading dominated the market, showing a tendency to actively go long for most of the time, followed by a correction at the end of the month after news settled beyond expectations.

The month was dramatic concerning the Federal Reserve's restart of rate cuts. On one hand, Trump continued to exert extreme pressure on social media, even visiting the Federal Reserve to intimidate Chairman Powell over exceeding repair costs; on the other hand, the Federal Reserve adhered to its dual mission of 'inflation + employment,' insisting on data orientation, and made 'hawkish' statements following the FOMC meeting. A divide appeared within the Federal Reserve, with governors Waller and Bowman clearly supporting an immediate rate cut, while governor Kugler unexpectedly resigned.

After the FOMC meeting on July 31, the pricing probability for a rate cut in September dropped to as low as 41%, but following the unexpectedly strong non-farm data released on August 1, this probability rapidly climbed to over 80%.

For most of the time, the S&P 500's performance was dominated by expectations of a September rate cut and strong corporate earnings. After July 28, as the probability of the September rate cut decreased, the market initiated adjustments after three consecutive months of significant growth. BTC also fell below $115,000, while Altcoins represented by ETH experienced even larger declines.

In remarks following the FOMC meeting, the Federal Reserve Chairman emphasized that tariffs could further impact inflation data over the next two months.

U.S. PCE data.

In July, Trump's announcement of tariff rates for more countries indeed exceeded market expectations. After two months of silence, the tariff war, now in its concluding phase, once again became a major factor affecting market pricing.

The current 'reciprocal tariff' system presents a four-layer structure of '10% baseline + 15–41% country gradient + EU special formula + 40% transshipment penalty.' The highest tier of 41% mainly targets regions with high geopolitical security risks; the mid-tier 25–35% locks down partners with large surpluses, high barriers, and limited negotiation progress; the 10% baseline is widely applicable and serves as a temporary plan for China.

Among the main trading countries/regions, the EU 15%, Canada 35%, Japan 15%, South Korea 15%, Mexico 10% (general goods)/25% (cars, etc.)/50% (steel, aluminum, copper) (still under negotiation), and China 30% (temporarily deferred for 90 days). This outcome exceeded market expectations, amplifying concerns about rising inflation, leading the market to downward price rebalancing around August 1.

In terms of economic and employment data, the overall U.S. economy is showing a trend of 'relative resilience + relatively strong growth.' The U.S. Q2 GDP annual rate released on July 30 was 3%, reversing the negative growth trend in Q1, surpassing expectations. In the financial reports released by large tech companies in July, it can also be seen that the AI wave is driving large enterprises to increase their investments, and AI investments have already begun to drive profit growth.

Of course, there are also concerns behind the data; the consumption recovery remains weak, and overall corporate investment is still sluggish.

The non-farm payroll data released on August 1 for July dealt a heavy blow to the market, resulting in a sharp decline in U.S. stocks. The data showed that only 73,000 jobs were added in July, significantly lower than the expected 110,000. Additionally, the May non-farm data was revised down from 144,000 to 125,000, and June from 147,000 to 134,000, with a total downward revision of 258,000 over two months. These figures greatly exceeded market expectations, causing panic over a 'soft landing' and downward pricing to complete the rebalancing.

Throughout the month, the market surged under expectations of rate cuts and no economic landing, but the release of tariff rates and non-farm employment data at the end of the month 'heavily impacted' the market's downward pricing.

For the entire month, the Nasdaq, S&P 500, and Dow Jones indices rose by 3.7%, 2.17%, and 0.08% respectively. BTC rose by 8.01%, while ETH rose by 48.8%.

In August, there remains a risk of further downward rebalancing in U.S. stocks. Following the weak non-farm data, the probability of a rate cut in September returned to 80%, yet concerns about inflation rebounding continue to trouble rate cut expectations. Additionally, while employment data hasn’t fundamentally impacted U.S. economic growth for the year, it remains a concern.

Whether a rate cut can occur as scheduled in September is drawing significant attention to upcoming inflation and non-farm employment data to be released in the next month.

Crypto assets: BTC is in an upward continuation, and Altseason may open.

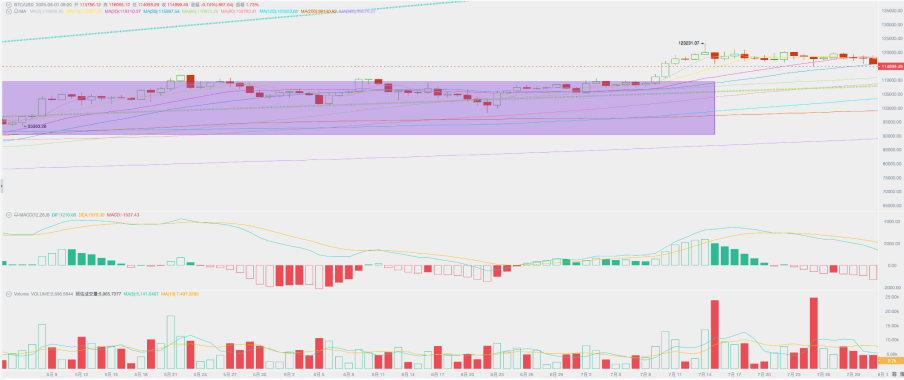

In July, BTC opened at $107,173.21 and closed at $115,761.13, with a low of $105,119.70. The month saw a historical high of $123,231.07, with an 8.01% increase and a volatility of 16.9%, alongside significantly increased trading volume compared to June.

BTC price daily chart.

In the June report, we pointed out that BTC had been oscillating for eight months in the 'Trump bottom' (the purple area in the chart above), with sufficient turnover, and that Q3 had the conditions to initiate the fourth wave of the market. The market broke through this area as expected in July and continued to rise for several trading days, but starting mid-month, with long-handed holders, especially ancient whales selling, combined with turmoil in the macro-financial environment, BTC's price failed to continue to rise and turned to oscillate and consolidate again.

From a technical indicator perspective, BTC is still operating above the 60-day moving average and the first upward trend line of the bull market (green dotted line in the chart above), with monthly trading volume increasing, indicating it is in a new round of upward continuation.

From a monthly cycle perspective, the MACD fast and slow lines are still in an expansion phase, indicating that the market is still in a strong upward momentum.

In terms of contracts, the continuous increase in open positions from the beginning to the end of the month indicates strong bullish sentiment in the market, but starting from the end of the month, both open positions and funding rates have shown significant declines. Under the backdrop of increased uncertainty, a certain scale of leveraged funds chose to exit for risk aversion.

Another significant event in July was the apparent re-initiation of Altseason within the crypto market, driven by strong corporate purchases, with ETH rising 48.8% for the month and the ETH/BTC trading pair breaking through technical resistance. We believe that with the approach of rate cuts and increased risk appetite, a re-opening of Altseason is highly likely.

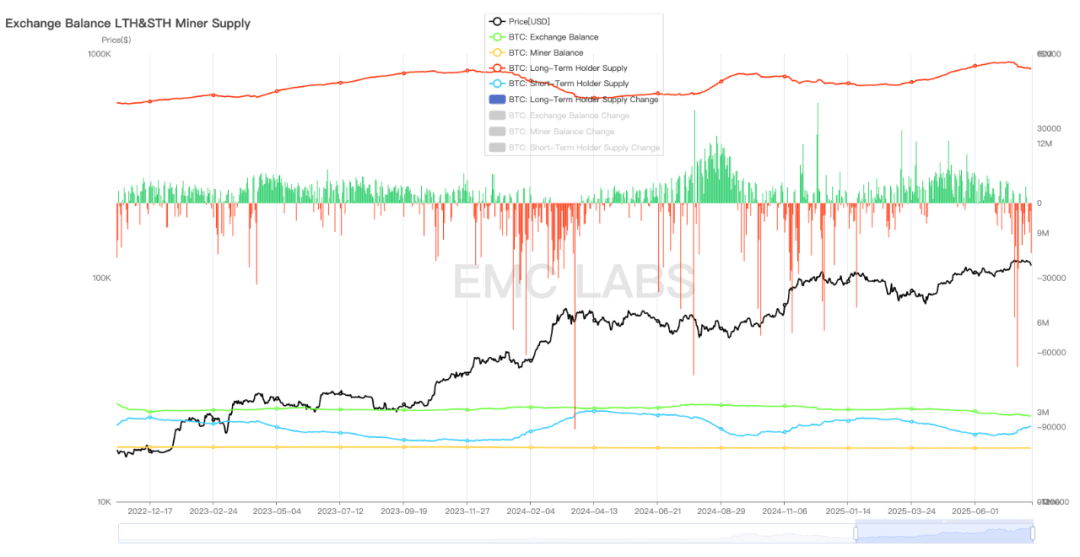

Chip structure: Long-handed holders initiate the third round of selling.

Accompanied by the buying power surge in July, long-handed groups initiated the third wave of selling in this bull market.

Long and short positions and their changes.

According to eMerge Engine data, long-handed holders reduced their positions by nearly 200,000 BTC in July, including 80,000 BTC from a wallet created during the Satoshi Nakamoto era. Correspondingly, short positions also increased rapidly.

BTC has shifted from long-handed to short-handed holders, increasing the market's short-term liquidity, which exerts pressure on prices. However, it can be observed that the short-term selling by ancient whales has a much smaller impact on market prices compared to the past, indicating a significant increase in market depth with the change in market participant structure.

Centralized exchanges continue to see BTC flowing out (over 40,000 BTC), indicating that institutional purchasing is ongoing. Institutional allocation is the direct driving force behind the upward price of BTC in this round of the bull market.

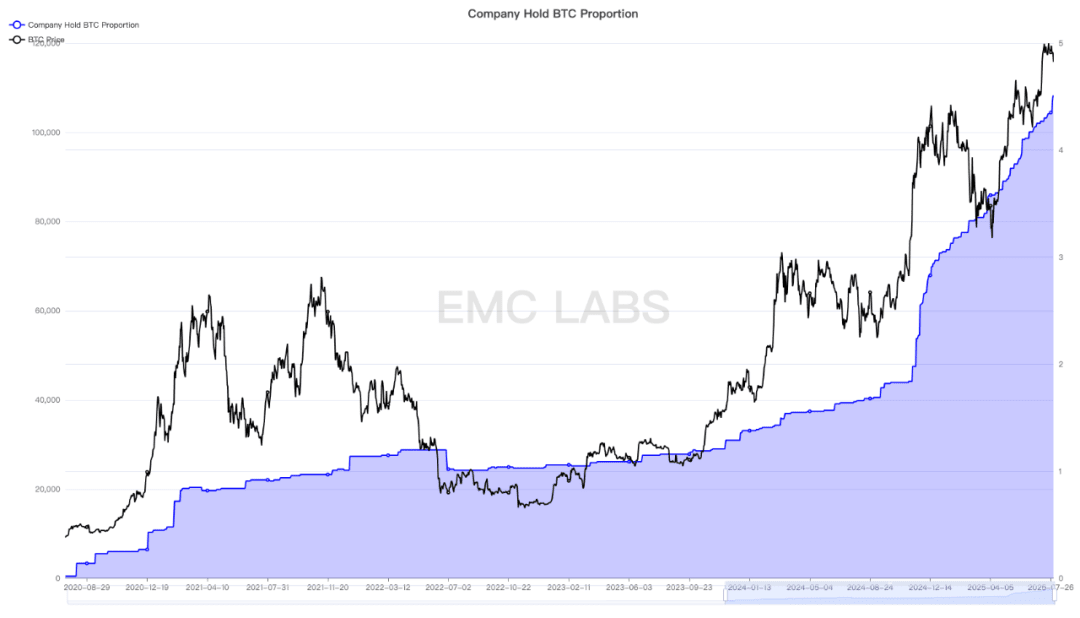

As of the end of July, publicly listed companies directly held more than 4.5% of the total supply of BTC.

Statistics of company-held BTC.

Since the beginning of this year, the scale of direct purchases of BTC by listed companies and other institutions has exceeded that of the BTC Spot ETF channel, officially making them the largest buyers in the BTC market.

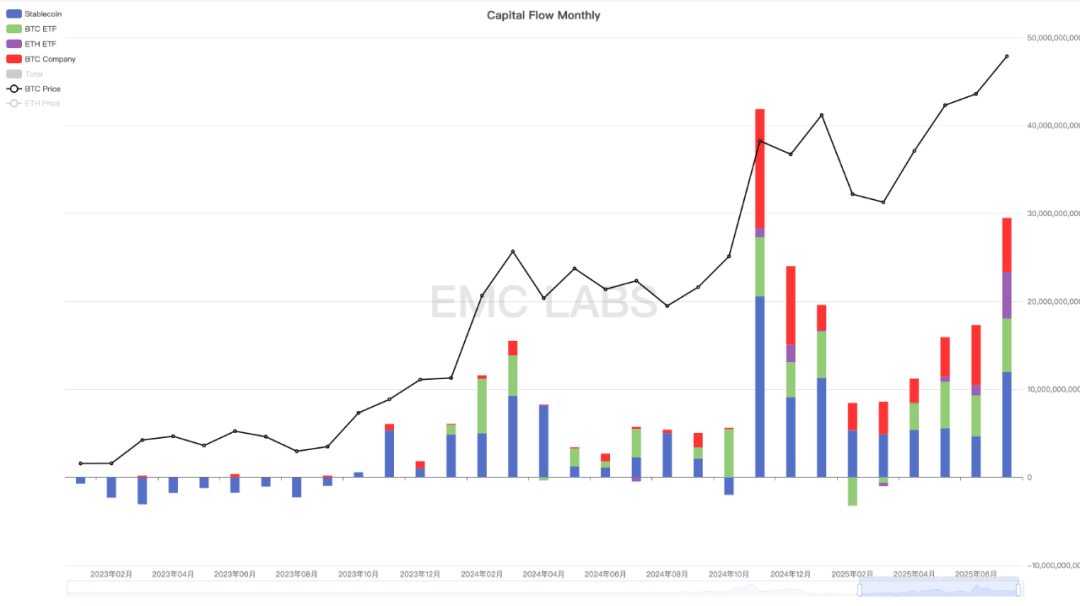

Capital flow: Over $29.5 billion inflow, making it the second-largest month in history.

This month, over $29.5 billion flowed into the crypto market, including $12 billion in stablecoins, $11.3 billion in BTC + ETH Spot ETFs, and $6.2 billion in corporate purchases. Corporate purchases are the single largest source of buying power in the BTC market that can be quantified.

Monthly statistics on capital flows in the crypto market.

The total inflow of $29.5 billion made July the second-largest inflow month in history, allowing BTC to break through the eight-month consolidation area, absorbing large selling pressure to push prices to new historical highs.

It's worth noting that total capital inflows have increased for five consecutive months, driving BTC to continue to rise from the six-month low set in April and reach new historical highs.

U.S. companies continue to accelerate their allocation to BTC, with more and more firms joining in, which is expected to remain the most important factor driving price increases for some time.

Moreover, this month saw ETH Spot ETF inflows reach $5.298 billion, the highest ever, approaching the $6.061 billion of the BTC Spot ETF channel. This is driven by the approaching rate cuts and the further expansion of crypto assets in the U.S., with more and more capital beginning to flow into ETH. At the end of the month, companies holding ETH accounted for 2.6% of the total circulating supply, although still lower than BTC's 4.6%, the growth rate is rapid, and the pricing power of ETH is shifting from on-exchange to off-exchange.

Conclusion

eMerge Engine shows that the BTC Metric is 0.75, indicating that BTC is in a bull market uptrend.

From a multi-dimensional analysis, BTC remains in the intermediate phase of the fourth wave of this bull market, and after fluctuations in August, it is likely to continue moving upward.

With ETH leading, as interest rate cuts approach, overall market risk appetite is increasing, and the likelihood of an Altseason is high.

Tariff conflicts, U.S. inflation, and employment data have become the biggest tail risks.