"When traditional financial giants start playing with crypto, the retail investors' scythe should change direction!"

This statement is now a true portrayal of the Hong Kong digital asset market.

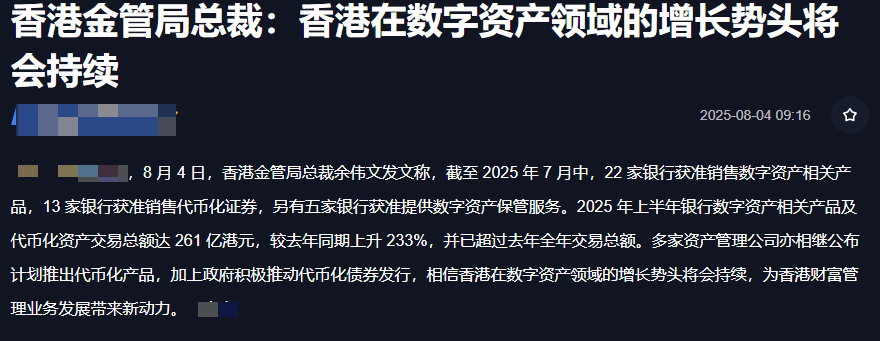

In recent years, people in the crypto space have been shouting for 'compliance', but what they got was not a regulatory crackdown, but Hong Kong entering the crypto market with 22 banks, 13 brokerages, and 5 custodians! In the first half of the year, the trading volume reached 26.1 billion HKD, a staggering increase of 233% year-on-year, surpassing last year's total in an instant—this is not growth; this is like launching a rocket to the sky!

I. Bank's involvement: The 'official add-on' for retail investors has arrived.

How difficult was it to buy cryptocurrencies before?

There was fear of hacks when withdrawing from exchanges, and remembering the private keys for cold wallets could be a headache, let alone the institutional funds that couldn't even find the door.

And now?

Now, 22 banks in Hong Kong are directly integrating digital assets into their apps—want to buy Bitcoin? Just a couple of taps on your phone; want to invest in tokenized stocks? Trade 24/7; worried about asset theft? The banks provide custody, and you don't even need to remember the private keys!

For example:

Standard Chartered Bank recently launched 'tokenized gold', where 1 gram of gold is transformed into a digital asset on the blockchain, allowing retail investors to buy it for 500 HKD and transfer it to DeFi platforms for mining and earning interest at any time. The 'big players' in traditional finance are now providing a 'retail-friendly add-on' to the crypto space!

My view?

Banks are not here to 'share the cake', but to 'make the cake'. What they bring is not just funds, but also compliance channels, risk control, and user trust—these three elements are exactly what the crypto space lacks the most.

II. The stablecoin war: Does HKD want to become the 'on-chain US dollar'?

On August 1, new regulations for HKD stablecoins took effect, and JD, Ant Group, Standard Chartered, and Lianlian Digital all rushed in to grab licenses!

Why is it so crazy?

Because once HKD stablecoins (like JD stablecoin, HKDR) are launched, they can do two things directly:

Cross-border payments: Trade settlement in the Greater Bay Area, instant transactions with zero fees;

Investment entry: Want to buy tokenized bonds in Hong Kong? You must subscribe using HKD stablecoins, with a stable annual return of 5%, which is 10 times better than keeping money in the bank!

Here comes the case:

A cross-border trader used to settle in USDT, fearing frozen accounts and price volatility; now he has switched to HKD stablecoin, where money runs on the chain and profits stay in his pocket. What's more, he can even deposit idle stablecoins into AAVE (a decentralized lending platform) to earn a 3% annual interest for free!

My prediction?

By the end of 2025, the circulation of HKD stablecoins will surpass USDT's share in Asia. It's not because HKD is so strong, but because the combination of 'compliance + returns' is a dimensional reduction attack on both institutions and retail investors.

III. Tokenized Bonds: The 'New Printing Machine' of the Crypto Space?

The Hong Kong government plans to issue 5 billion HKD in tokenized government bonds in the fourth quarter, with HSBC and Morgan Stanley joining in, intending to put corporate bonds on the blockchain as well.

How powerful is this thing?

Retail investors can buy: 100 million in bonds broken down into 10,000 shares, each worth 10,000 HKD. Previously, only institutions could play this game, but now retail investors can also share a slice of the pie;

T+0 trading: Traditional bonds take 3 days to sell, while tokenized ones can be done in 3 seconds, making high-frequency traders ecstatic;

Smart contract dividends: Interest is credited automatically, no worries about defaults, and credit ratings are guaranteed.

Case study:

A large investor in the crypto space used to have to find a brokerage to buy bonds and sign a bunch of contracts; now, using the HKEX's Diamond platform, he can purchase it with just a couple of clicks, and interest is displayed on-chain daily, more reassuring than watching candlesticks. Even better, he can collateralize the bonds to borrow USDT and continue trading cryptocurrencies—left hand steady returns, right hand a chance for wealth, this operation is legendary!

My conclusion?

Tokenized bonds are not 'toys of the crypto space', but a 'rebirth of traditional finance on the chain'. It will slowly direct trillions of dollars from the bond market into the crypto market, and 'risk assets' like Bitcoin and Ethereum will also benefit from this surge.

Is your wallet ready?

This wave of actions from Hong Kong essentially uses traditional finance's 'compliance bullets' to penetrate the 'trust wall' of the crypto market.

With banks entering the market, the rise of stablecoins, and the explosion of tokenized bonds—these three factors combined mean that the crypto market in 2025 will not just be about 'bull market or bear market', but rather a survival battle of 'who gets on the bus first, who makes money first'!

Here comes the question:

Would you use a bank app to buy cryptocurrencies?

Will HKD stablecoins replace USDT?

Are tokenized bonds an opportunity or a pitfall?

See you in the comments section, if likes exceed 1000, the next issue will unveil the wealth list of 'Hong Kong concept coins'!

(Follow me for insider info on the crypto space, delivered to you in real-time!)