U.S. mortgages officially accept Bitcoin! The Lummis bill ignites a bull market, is Democratic obstruction the last chance to get on board?

1. Major policy changes: Cryptocurrency entering the U.S. mortgage market.

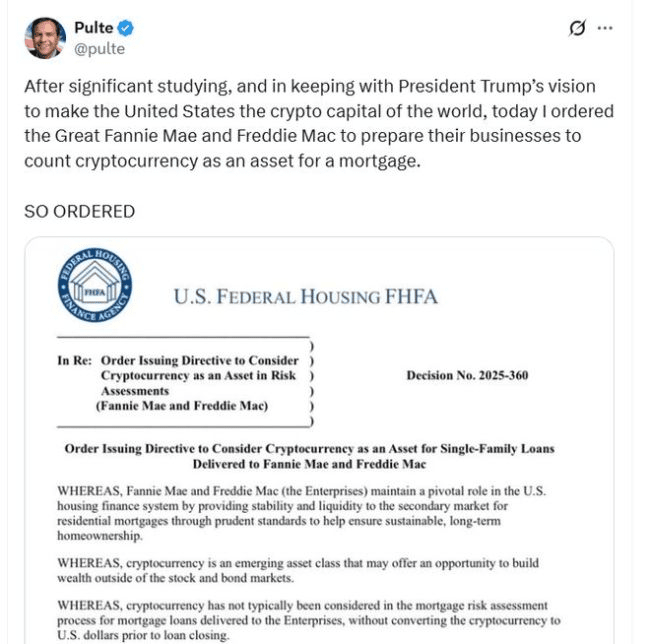

On June 25, 2025, William Pulte, director of the Federal Housing Finance Agency (FHFA), ordered Fannie Mae and Freddie Mac to include cryptocurrencies in mortgage collateral assessments, limited to mainstream coins stored on U.S.-regulated centralized exchanges (such as Bitcoin and Ethereum), and without needing to convert to USD. This directly echoes the Trump administration's 'Crypto America' strategy, aiming to address the market dilemma of mortgage issuance dropping to near historical lows (Q1 2025 data).

2. Controversy focus: Volatility risk vs. market expansion.

Republican support: Senator Lummis proposed the (21st Century Mortgage Act), allowing compliant crypto assets as reserves, but requiring volatility valuation adjustments (like discount rates).

Democratic opposition: Concerns that a 16% weekly drop in crypto assets (like Bitcoin in February 2025) could threaten mortgage stability.

Truth: Traditional banks' interests are impacted, Fannie Mae and Freddie Mac cover 50% of U.S. mortgages, and crypto mortgages will divert bank credit share.

3. Cryptocurrency market impact: Institutions begin hoarding coins.

BTC/ETH are the biggest winners: Policies only recognize mainstream coins on centralized exchanges, altcoins are marginalized.

New narrative: The concept of 'Bitcoin = digital real estate' is rising, mortgage lending may become a new path for cashing out in a bear market (refer to private institution Milo which has issued $65 million in crypto mortgages).

Short-term volatility: Following the announcement, Bitcoin rose 2.2% in one day to $107,000, but Ethereum fell, showing clear market differentiation.

4. Risks and opportunities coexist.

Positive outlook: If Trump is re-elected, policies may expand to stablecoins (like USDC) and tokenized real estate.

Risk: A crash may trigger forced liquidations, requiring over-collateralization (e.g., LTV 50%).

5. Action guide

Heavy investment in BTC/ETH: Compliant assets are preferred by institutions.

Positioning in real estate chains.

Projects: Such as Propy (blockchain property) and Milo (crypto mortgage platform).

Beware of political black swans: The Democratic Party may suppress the market before the election, but a downturn could present opportunities.

Not hoarding Bitcoin in 2025 is like not buying a house in 2013!#巨鲸

Follow Long Brother for daily market insights, guiding you through challenges in the market.