Written by: Deep Tide TechFlow

Whenever the market is good, FUD is inevitable.

Today, a piece of news has once again raised concerns about ETH's price:

Validators on the Ethereum network are queuing to unstake ETH.

As a representative of the PoS consensus mechanism, staking ETH is technically used to maintain the security of the entire Ethereum network, and economically can also gain additional income generated from staking, locking the liquidity of ETH in the staking pool.

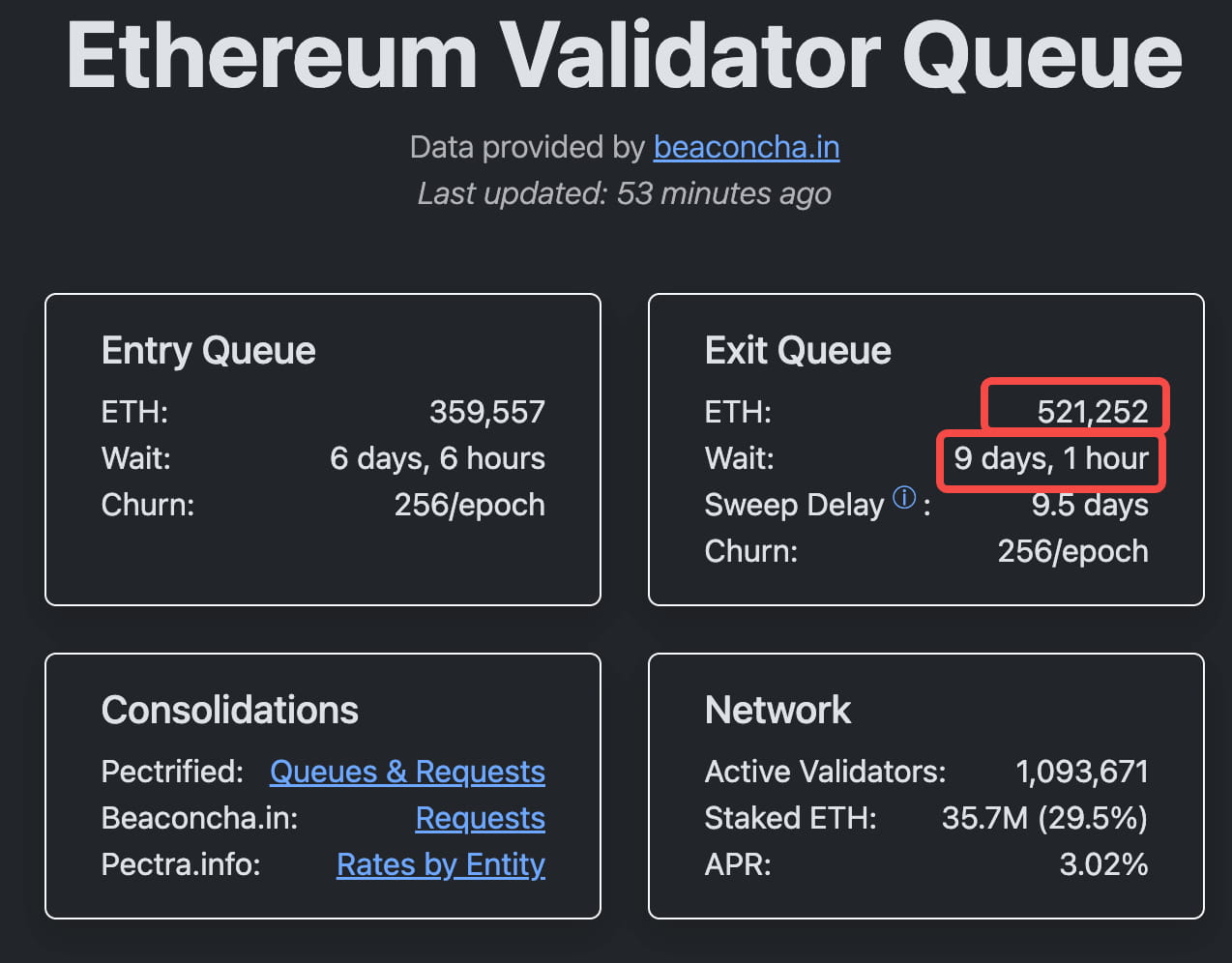

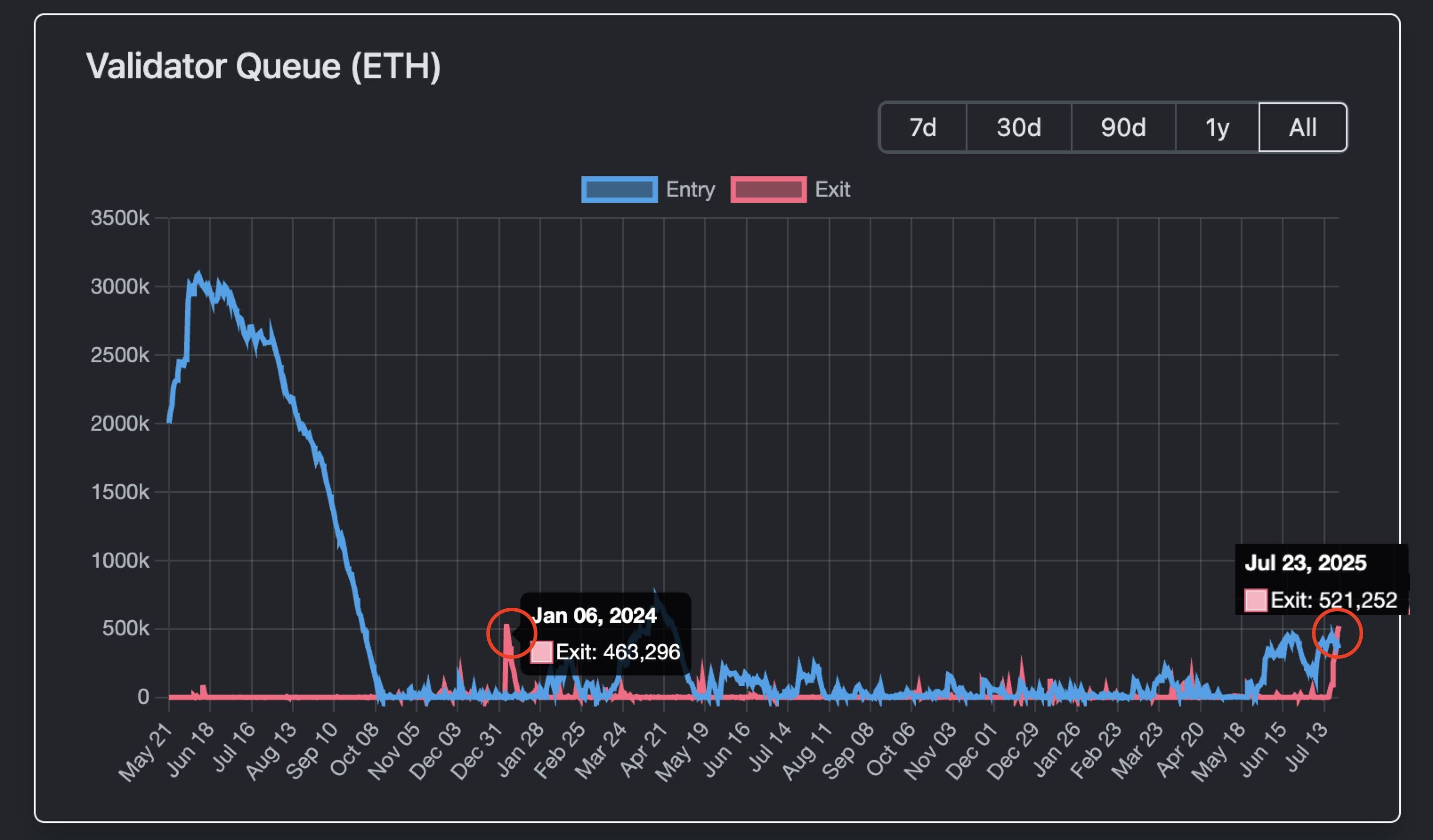

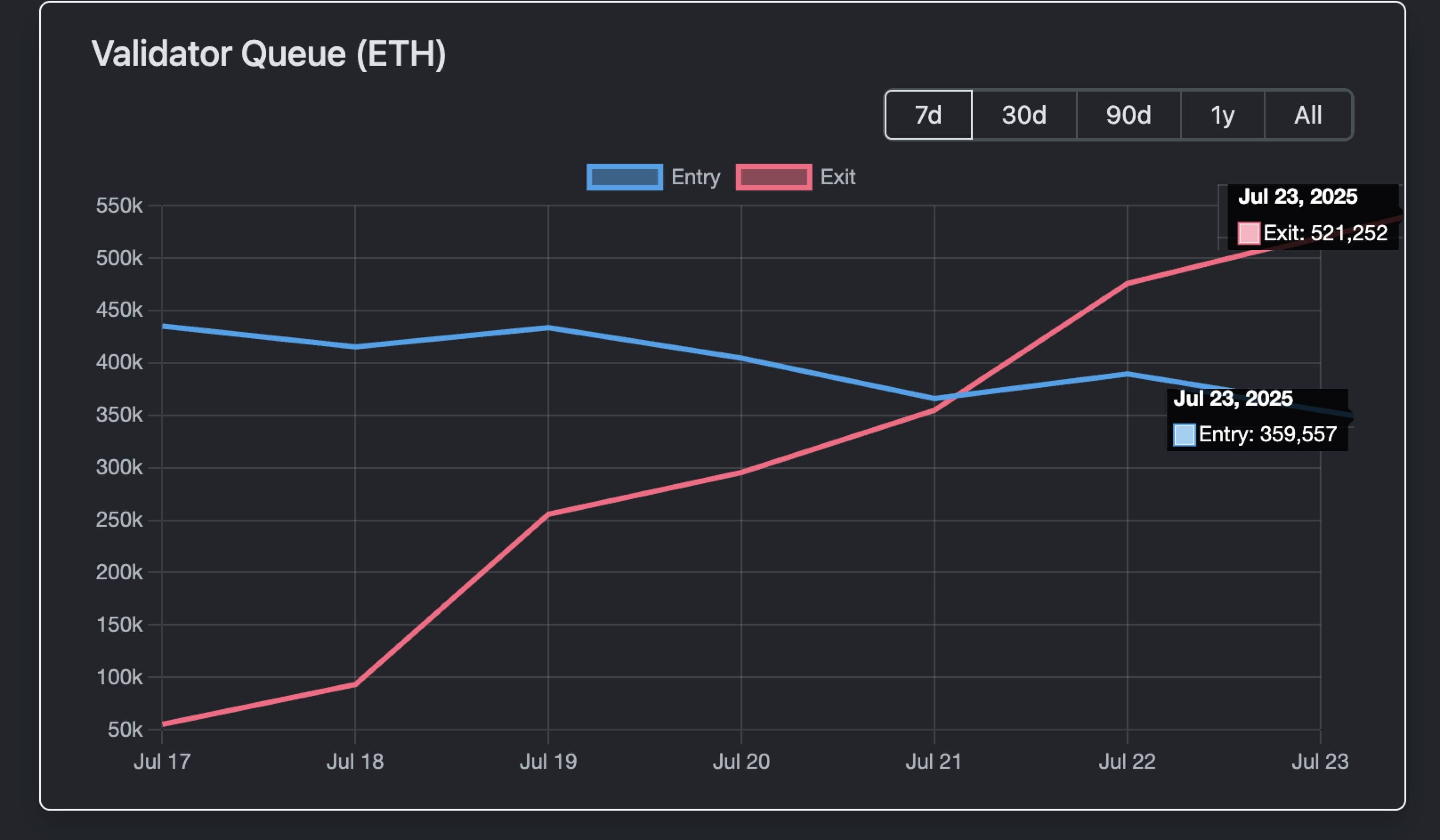

However, according to the data from the Validator Queue, as of July 23, approximately 521,252 ETH were queued for unstaking, valued at about 1.93 billion USD, with a waiting time of over 9 days and 1 hour for unstaking.

This is also the longest queue that validators have queued for when choosing to exit in the past year.

Since each validator usually stakes 32 ETH, theoretically, this corresponds to more than 16,000 validators seeking to exit staking. The large-scale queue for unstaking brings a sense of danger.

Profit-taking?

Are the whales and institutions going to sell ETH to take profits?

The surge in Ethereum's unstaking may be partially related to the recent price increase.

Starting from the low point in early April 2025 (around the 1,500-2,000 USD range), ETH experienced a strong rebound, with a cumulative increase of 160% to date. Specifically, on July 21, ETH reached a high of 3,812 USD, the peak in the past seven months.

Such rapid increases often prompt some investors to choose to take profits, especially those early stakers who may decide to lock in profits after seeing gains rather than continuing to hold.

From a historical perspective, this model is not new.

From January to February 2024, after the ETH/BTC ratio rose 25% in a week, a similar scale of unstaking wave appeared, causing a short-term price drop of 10%-15%. However, it was also around the same period when Celsius declared bankruptcy, resulting in 460,000 ETH being unstaked in a short time, leading to about a week of queue congestion for validator exits on the entire ETH network.

Not selling pressure

Unlike before, although the queue for ETH unstaking is long this time and the amount being unstaked is large, it does not necessarily mean direct selling pressure.

First, let's look at the data from the Validator Queue. On July 23, there were 520,000 ETH queued for unstaking, but at the same time, 360,000 ETH entered the staking queue.

With both sides offsetting each other, the net ETH exiting the Ethereum network will significantly decrease.

Secondly, institutional behavior also plays a buffering role.

Data from July 22 shows that the total inflow of ETH spot ETFs from various institutions in the public market reached 3.1 billion USD, significantly greater than the 520,000 ETH (1.9 billion USD) queued for unstaking that day.

Moreover, this is just one day's net inflow of ETFs, not to mention that there is a 9-day queue period for validators to exit.

At the same time, unstaking does not necessarily mean selling.

In the current environment of ETH price increase, concentrated unstaking is also likely due to institutional adjustments to custody services or a shift toward crypto treasury strategies; to put it more clearly, it is about changing the custodian of ETH to seek higher returns, rather than taking ETH out to sell.

On-chain, part of the unstaked ETH is more likely to be used for DeFi and NFT-related activities. For example, providing liquidity as collateral, or yesterday, a whale was sweeping the floor of Crypto Punks.

In addition, the on-chain LST tokens often experience decoupling, which also provides arbitrage opportunities for ETH—recently, the ratio of stETH to ETH dropped to 0.996 (a discount of about 0.04%), and weETH also showed similar fluctuations. Arbitrageurs buy discounted LSTs and wait for a return to the 1:1 peg to profit, which increases the demand for ETH.

Overall, unstaking seems more like an internal adjustment within the Ethereum ecosystem rather than a direct selling signal.

However, there are various speculations on social media; concentrated unstaking, while not implying selling pressure, may indicate a phenomenon of 'changing positions.'

Some believe that BlackRock, which is committed to promoting cryptocurrency assets into the mainstream financial circle, has effectively become a large player in ETH. As of July data, BlackRock has accumulated over 2 million ETH (worth about 6.9-8.9 billion USD), accounting for about 1.5%-2% of the total ETH supply (approximately 120 million ETH).

This is not a secret, but a public asset management behavior of ETFs, so it is more like an institutional-level 'open position'—through ETFs holding and accumulating publicly, promoting institutional adoption of ETH rather than manipulating the market.

The logic of changing positions is that as Ethereum transitions from an internal value consensus to a broader consensus as a financial instrument, it is already a very obvious trend that Wall Street is ready to make a big move.

This speculation is not without reason; staking and unstaking may also represent a shift in the chip structure.

Regardless, Ethereum's growth potential will continue to support its leadership position in the crypto space, and this wave of unstaking may just be the starting point of a new cycle.