There is no doubt that this round of crypto bull market started first in US stocks.

When the 'crypto treasury reserve strategy' becomes a trendsetter in US stocks, and coin-stock linkage occurs, how should we assess the quality of a stock? Is it based on who has the largest amount of crypto assets, or who has the funds to continuously buy crypto assets?

If you have been frequently following analysis on crypto US stocks, you should have seen a term repeatedly appearing --- NAV, which stands for Net Asset Value.

Some people use NAV to analyze whether crypto stocks are overvalued or undervalued, while others use NAV to compare the stock price of a new crypto reserve company with that of MicroStrategy; yet the more critical wealth secret lies in:

If a publicly traded US company adopts a crypto reserve strategy and holds $1 worth of cryptocurrency, its value is greater than $1.

Companies that hold these cryptocurrency assets can continue to increase their holdings or buy back their shares, leading their market value to often far exceed their NAV (Net Asset Value).

However, for ordinary investors, most projects in the crypto space are rarely evaluated using serious metrics, let alone using them to assess stock values in traditional capital markets.

Therefore, I also plan to create a popular science segment on the NAV metric to help players focused on coin-stock linkage better understand the operational logic and evaluation methods of crypto stocks.

NAV: How much is your stock actually worth?

Before diving into the discussion of crypto stocks, we need to clarify a fundamental concept.

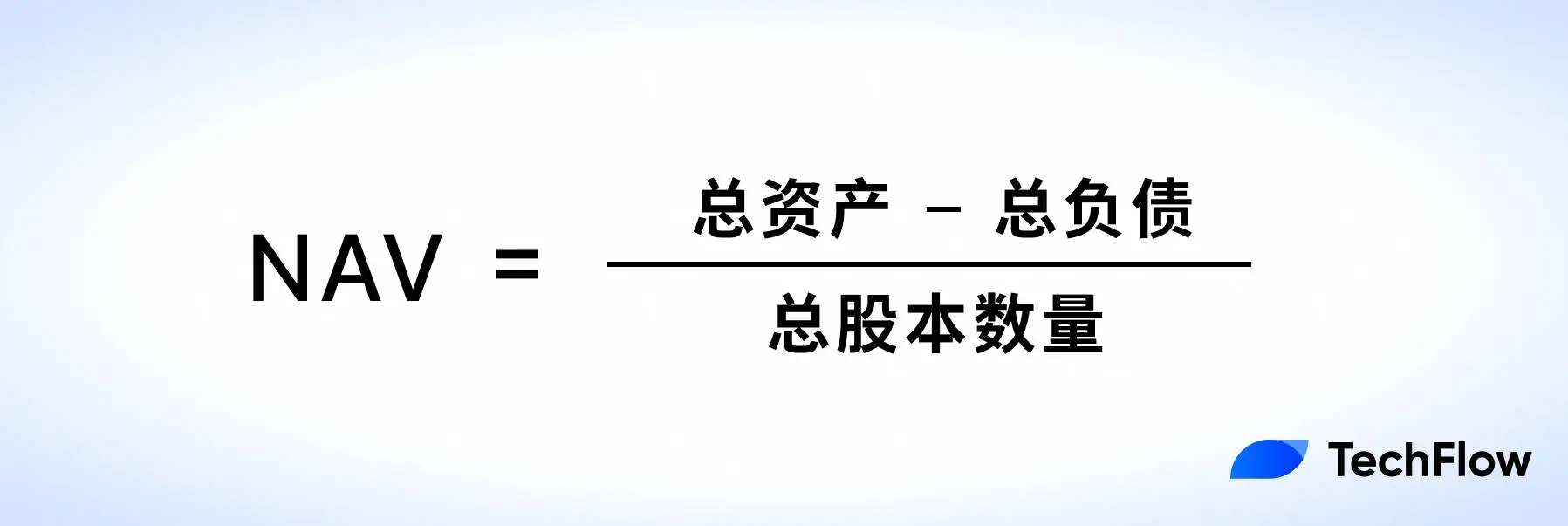

NAV is not a metric specifically designed for the crypto market, but rather one of the most common methods in traditional financial analysis for measuring company value. Its essential role is to answer a simple question:

How much is a company's stock actually worth?

The calculation of NAV is very straightforward, which is the value that shareholders can receive per share after the company's assets are subtracted from liabilities.

To better understand the core logic of NAV, we can use a traditional example to illustrate. Suppose there is a real estate company with the following financial status:

Assets: 10 buildings, total value of $1 billion; Liabilities: Loans of $200 million; Total shares: 100 million shares.

Then the company's net asset value per share is: $80/share. This means that if the company liquidates its assets and pays off all its debts, shareholders theoretically can receive $80 per share.

NAV is a very general financial metric, particularly suitable for asset-driven companies, such as real estate companies, investment funds, etc. The assets owned by these companies are usually quite transparent, and their valuations are relatively easy, so NAV can well reflect the intrinsic value of their stocks.

In traditional markets, investors typically compare NAV with the current market price of the stock to judge whether a stock is overvalued or undervalued:

If stock price > NAV: The stock may be at a premium, indicating investor confidence in the company's future growth potential;

If stock price < NAV: The stock may be undervalued, with insufficient market confidence in the company, or uncertainty in asset valuations.

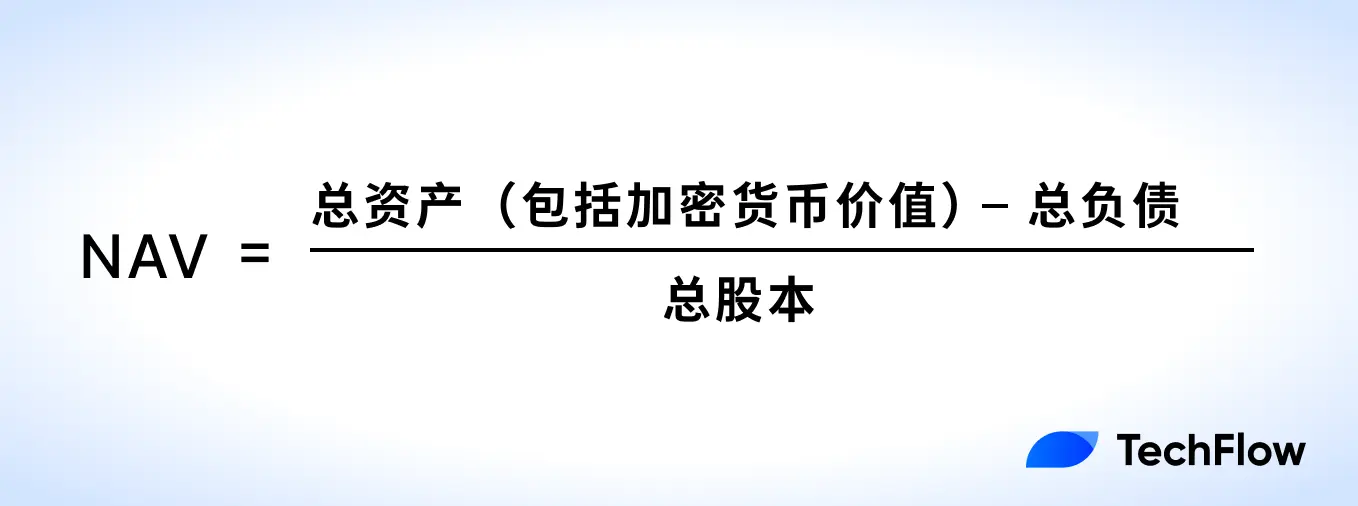

When NAV is applied to crypto US stocks, its meaning undergoes some subtle changes.

In the field of crypto US stocks, the core role of NAV can be summarized as:

To measure the impact of the crypto assets held by a publicly traded company on its stock value.

This means that NAV is no longer just the traditional formula of 'assets minus liabilities', but it is necessary to particularly consider the value of the cryptocurrency assets held by the company. The price fluctuations of these crypto assets directly affect the company's NAV and indirectly affect its stock price.

Companies like MicroStrategy emphasize the value of their Bitcoin holdings in the calculation of NAV, as this portion of assets occupies the majority of the company's total assets.

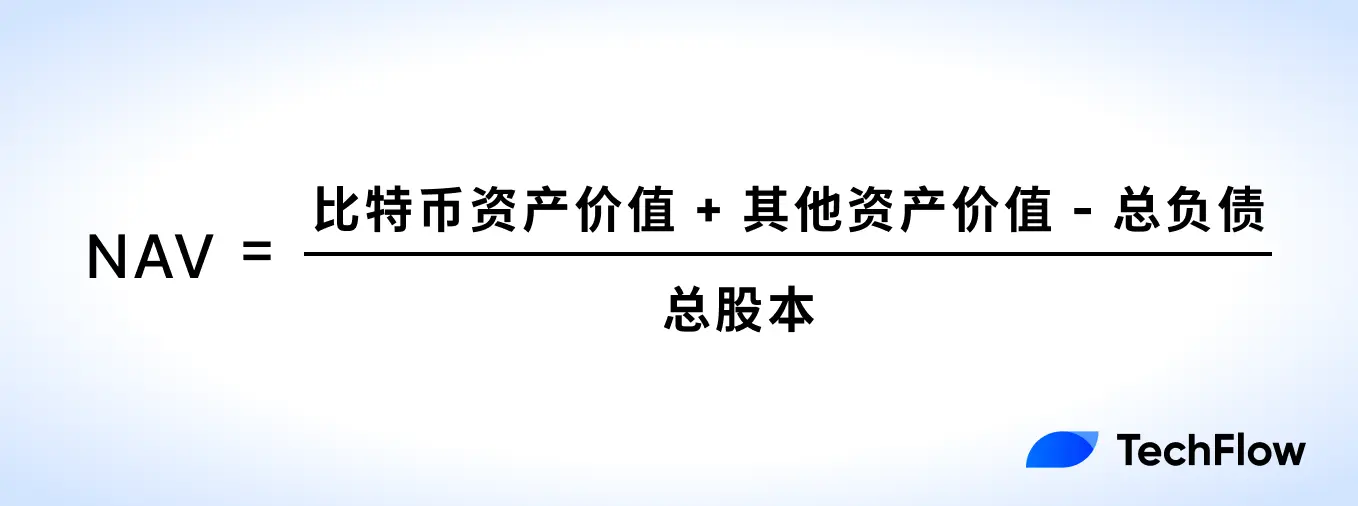

Thus, the above calculation method is slightly extended:

When cryptocurrency assets are included in the calculation of NAV, some changes you must consider are:

The volatility of NAV has significantly increased: due to the drastic price fluctuations of cryptocurrencies, NAV is no longer as stable as real estate or fund assets in traditional markets.

The value of NAV is 'amplified' by crypto assets: cryptocurrency assets often gain a premium in the market, meaning investors are willing to pay a price higher than their book value to purchase the relevant stocks. For example, a company holds $100 million in Bitcoin assets, but its stock price may reflect the market's expectations of Bitcoin's future appreciation, leading to a market value of $200 million.

When the market is bullish on Bitcoin's future price, the company's NAV may be assigned an additional premium by investors; conversely, when market sentiment is low, the reference value of NAV may decline.

If you still don't understand NAV, let's use MicroStrategy as an example.

As of the time of publication (July 22), publicly available data shows that MicroStrategy holds 607,770 Bitcoins, priced at $117,903, with a total Bitcoin asset value of about $72 billion, other assets around $100 million, and company liabilities of $8.2 billion.

MicroStrategy's total share capital is about 260 million, and according to the above calculation, its NAV is approximately $248 per share. This means that with BTC held as a crypto reserve, MicroStrategy's stock should be valued at $248.

However, in the last trading day of US stocks, MicroStrategy's actual stock price was $426.

This reflects market premiums; if the market believes Bitcoin will appreciate in the future, investors will factor this expectation into the stock price, causing it to be higher than NAV.

This premium reflects that NAV cannot fully capture the market's optimistic expectations for crypto assets.

mNAV: A thermometer for crypto US stock sentiment

Aside from NAV, you often see analysts and KOLs discussing another similar indicator --- mNAV.

If NAV is the basic metric for measuring how much a stock is worth, then mNAV is a more advanced tool that aligns with the dynamics of the crypto market.

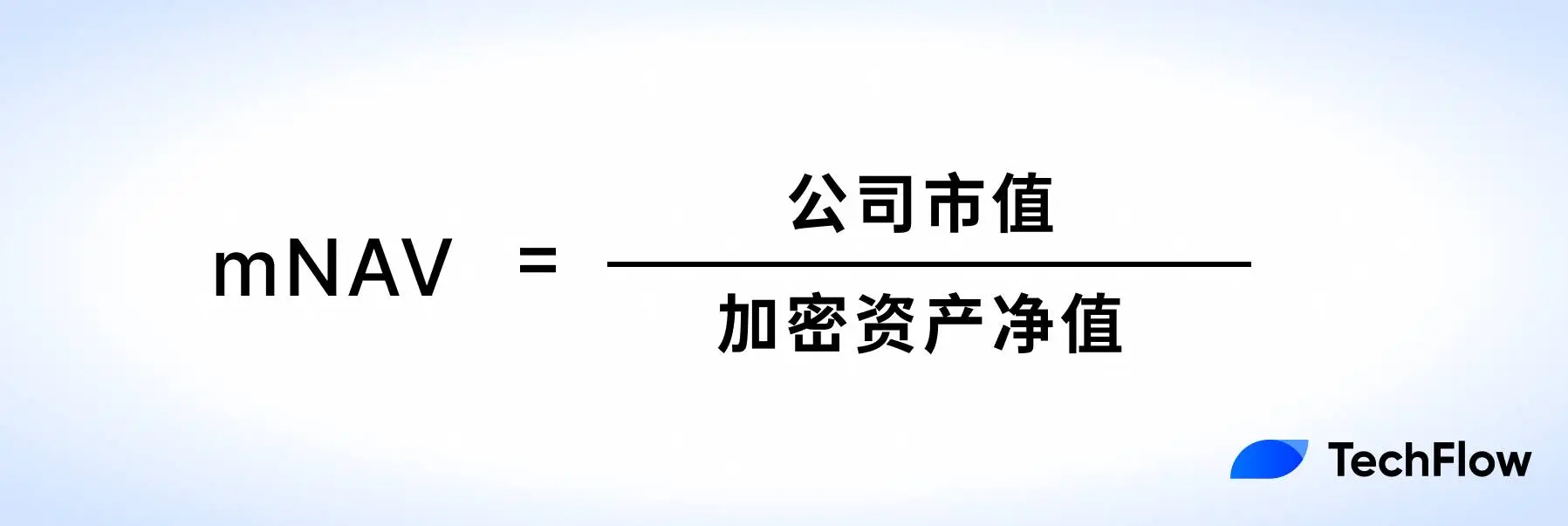

As mentioned earlier, the focus of NAV is to reflect the company's current net asset status (mostly crypto assets), without involving market expectations for these assets; mNAV is a more market-oriented indicator used to measure the relationship between the company's market value and its net value of crypto assets. Its calculation formula is:

Here, 'Net Value of Crypto Assets' refers to the value of the company's cryptocurrency assets minus the related liabilities.

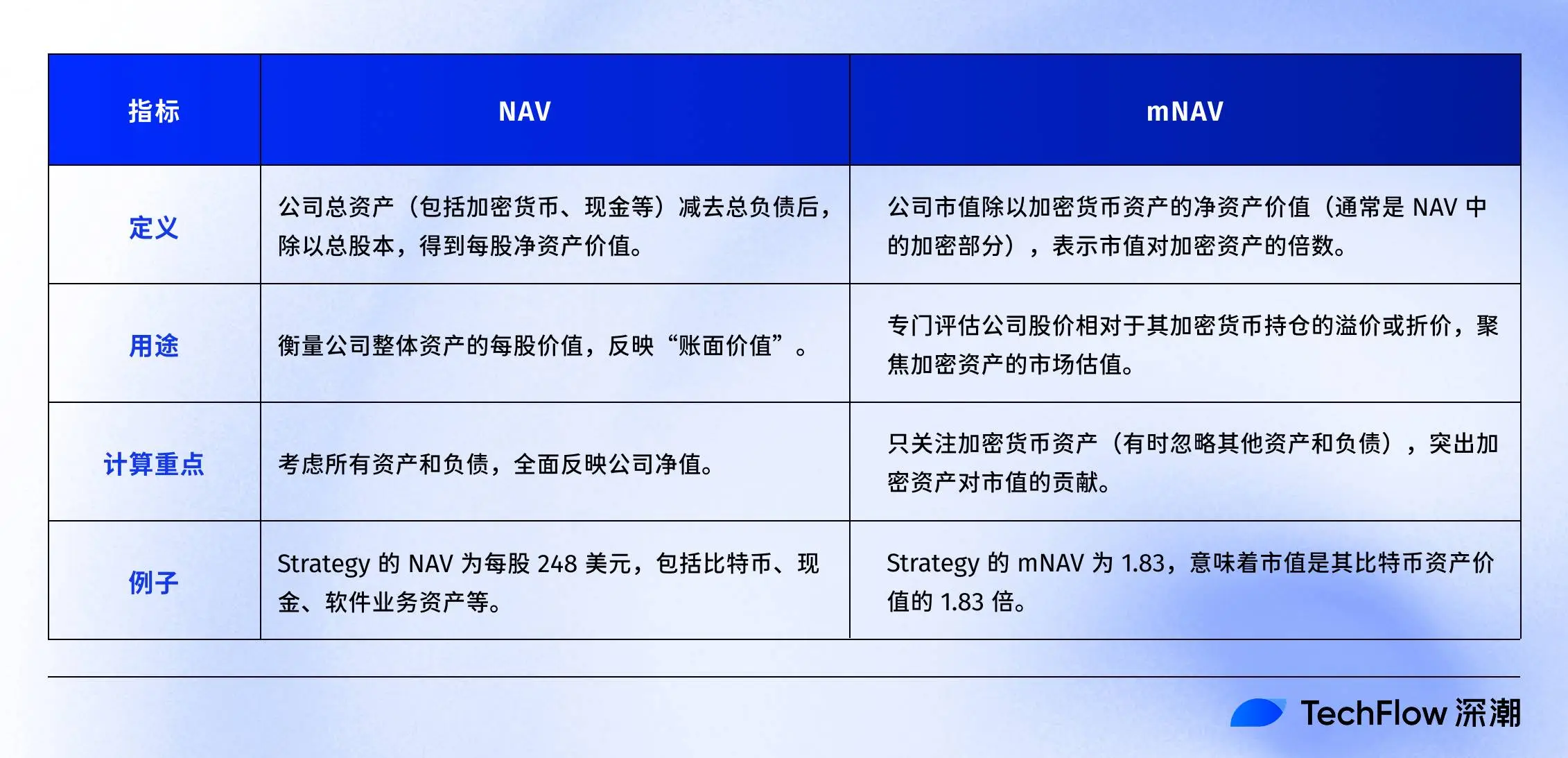

We can use a table to clearly compare the differences between the two indicators:

Also according to previous calculations, MicroStrategy's total market value is around $120 billion, while the net value (crypto assets + other company assets - liabilities) of the BTC it holds is around $63.5 billion, making its mNAV approximately 1.83.

This means that MicroStrategy's market value is 1.83 times the value of its Bitcoin assets.

Thus, when a company holds a large amount of cryptocurrency assets, mNAV can better reveal market expectations for these assets, reflecting investors' premiums or discounts on the company's crypto assets; for instance, in the above example, MicroStrategy's stock price is at a premium of 1.83 times its net crypto assets.

For short-term investors who pay attention to market sentiment, mNAV is a more sensitive reference indicator:

When Bitcoin prices rise, investors may be more optimistic about the future performance of crypto asset-driven companies. This optimistic sentiment is reflected through mNAV, causing the market price of the company's stock to exceed its book value (NAV).

mNAV greater than 1 indicates that the market assigns a premium to the company's crypto asset value; mNAV less than 1 means insufficient market confidence in the company's crypto assets.

Premiums, reflexivity flywheel, and death spiral

As mentioned earlier, MicroStrategy's mNAV is currently around 1.83;

As ETH increasingly becomes a reserve asset for listed companies, understanding the mNAV of these companies is also significant for identifying whether corresponding US stocks are overvalued or undervalued.

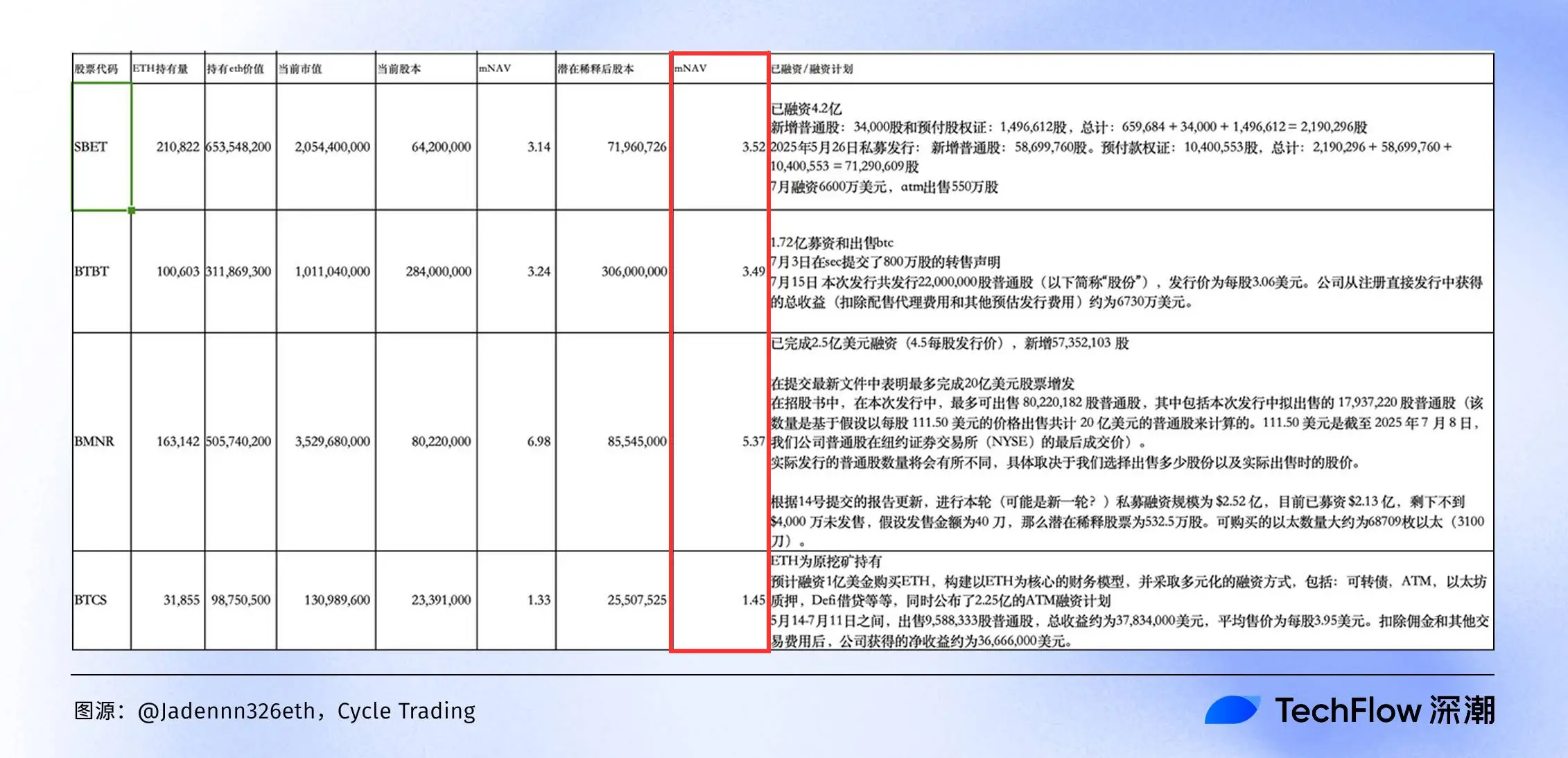

An analyst from Cycle Trading @Jadennn326eth has compiled a fairly detailed table, visually displaying the asset-liability status and mNAV values of major ETH reserve companies (data as of last week).

From this ETH reserve company mNAV comparison chart, we can see the 'wealth map' of the coin-stock linkage in 2025 at a glance:

BMNR ranks first with a 6.98 times mNAV, with a market value far exceeding its ETH holdings, but this may hide an overvaluation bubble—once ETH corrects, the stock price will also be first to suffer. BTCS has only 1.53 times mNAV, relatively lower premium.

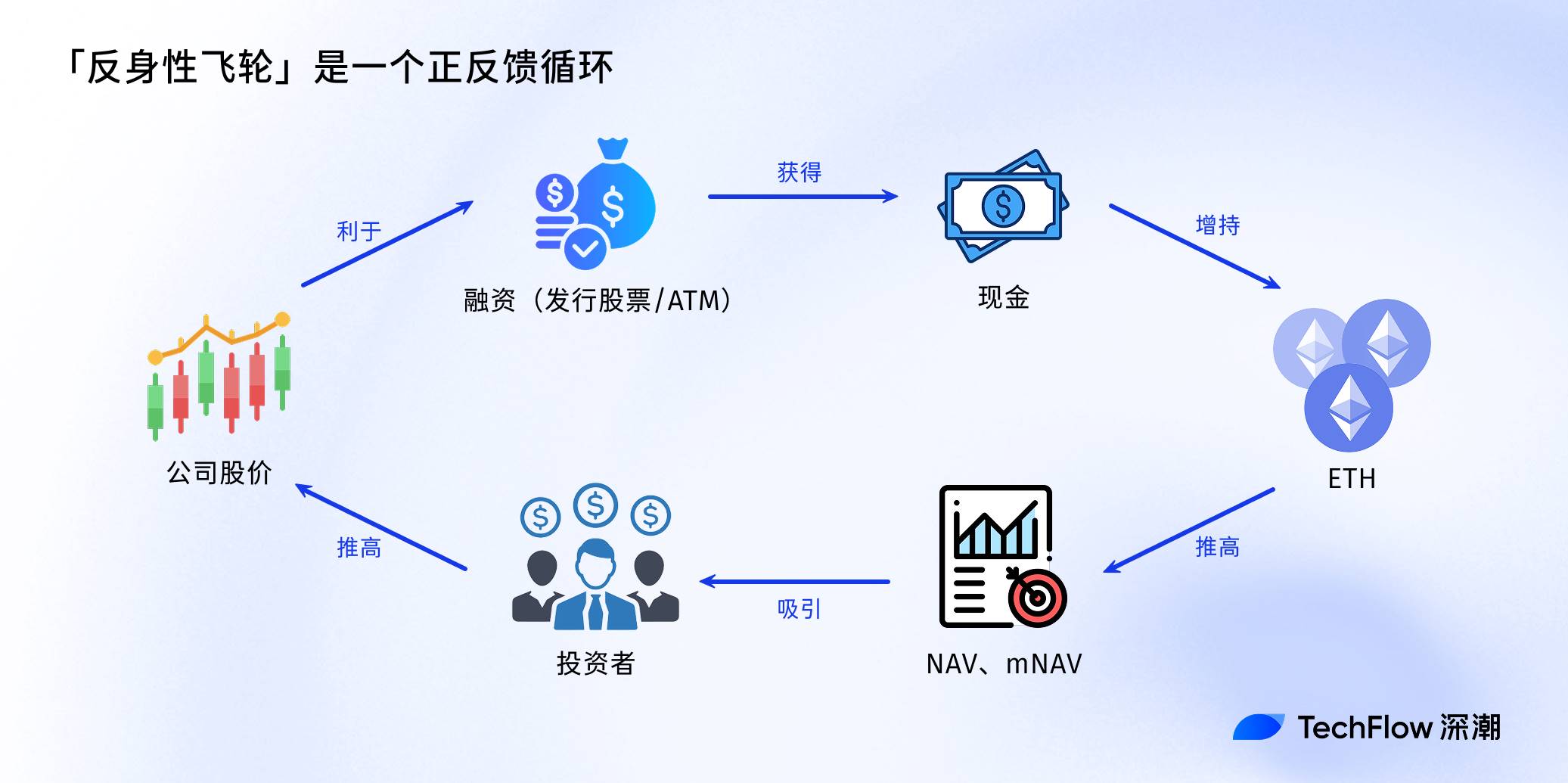

Having seen the data of these companies, we cannot help but discuss the 'reflexivity flywheel'.

This concept originates from financial magnate Soros's reflexivity theory, which became the 'secret engine' behind the soaring stock prices of these companies during the bullish market of 2025 linked to crypto stocks.

In simple terms, the reflexivity flywheel is a positive feedback loop: The company first issues stock or conducts ATM (At-The-Market) financing, gaining cash to buy ETH in bulk; the increase in ETH holdings raises NAV and mNAV, attracting more investors, driving up stock prices; a higher market value makes it easier for the company to refinance and continue increasing ETH holdings... thus forming a self-reinforcing, snowball-like flywheel effect.

Once ETH prices correct, regulations tighten (for instance, SEC reviews on crypto reserve models), or financing costs soar, the flywheel may reverse into a death spiral: stock prices collapse, mNAV plummets, and ultimately, it may also hurt the stock market's retail investors.

Finally, by now you should understand:

Indicators like NAV are not panaceas, but powerful tools in the toolbox.

Players pursuing coin-stock linkage should combine macro trends of Bitcoin/Ethereum, the company's debt levels, and growth rates for rational evaluation to find their own opportunities in what seems like an opportunity-laden but actually perilous new cycle.