Holdings are highly concentrated: MSTR accounts for 2.865% of the total BTC held by listed companies, while outside the Top 10, holdings are relatively low.

· Project homogeneity is severe: most reserve projects lack sustainable advantages, and long-term NAV premiums or relatively quality projects may fade.

· Valuation bubble emerging: NAV multiples generally >2× (only a few <1×), stock prices are sensitive to announcements while bear market risks can quickly erode premiums.

· Metaplanet profits from a zero-interest convertible bond + SAR financing, leveraging a 20% dividend tax and a 55% Bitcoin trading tax differential.

· SPAC/PIPE/convertible bonds/physical commitments are mainstream, with TwentyOne and ProCap achieving full reserves upon listing through multi-step mergers.

· SharpLink's financing scale exceeds $838 million, with nearly full ETH staking, Joseph Lubin joins the board, and 10,000 ETH is delivered through OTC transactions with the Ethereum Foundation.

· BTCS innovatively borrows USDT from Aave to purchase ETH for staking while being sensitive to lending rates and on-chain liquidity.

· Crypto funds are positioning strategic reserve stocks through PIPE and other means, establishing dedicated funds; industry veterans serve as strategic advisors, providing practical support and expertise.

Introduction

The trend of publicly traded companies turning to cryptocurrency reserve strategies shows no signs of waning. Some companies see this as a last-ditch effort to save their businesses, while others simply replicate MicroStrategy's approach, but a few truly innovative projects have emerged.

This article will explore the dominant players in the Bitcoin and Ethereum strategic reserve space—analyzing how they provide alternatives to spot ETFs, deploy complex financing structures, achieve tax optimization, create staking yields, integrate DeFi ecosystems, and leverage unique competitive advantages.

Bitcoin

Panoramic Overview

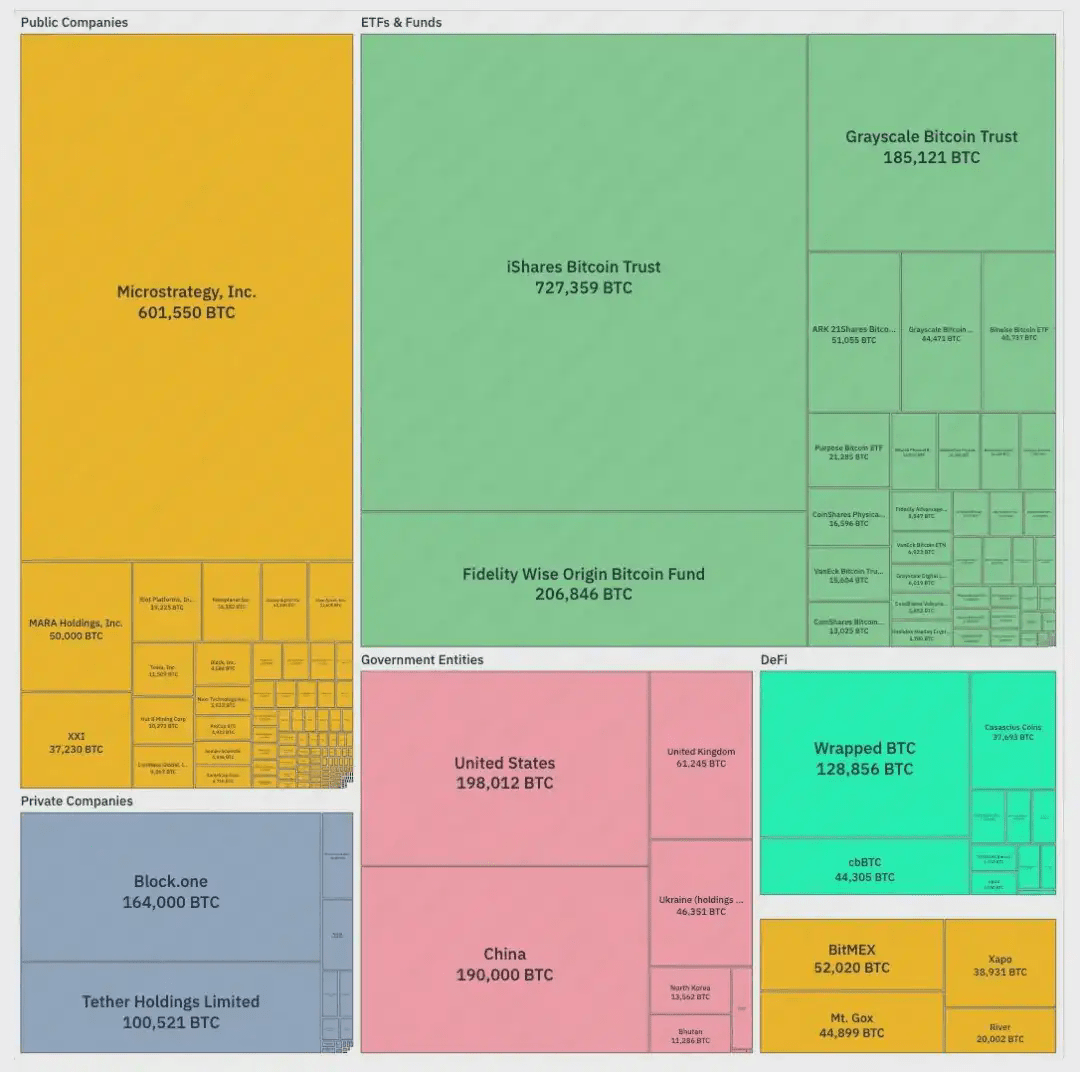

According to the rectangular treemap of BitcoinTreasuries.net, MicroStrategy has quickly risen to become the largest corporate holder among entities that publicly disclose their holdings—second only to the iShares Bitcoin Trust—controlling nearly 2.865% of the total supply of 21 million Bitcoin today.

Nevertheless, ETFs and trusts still dominate, led by iShares, Fidelity, and Grayscale. At the sovereign level, the United States and China hold the most Bitcoin, with Ukraine also maintaining a substantial reserve. Among private companies, Block.one and Tether Holdings rank at the top.

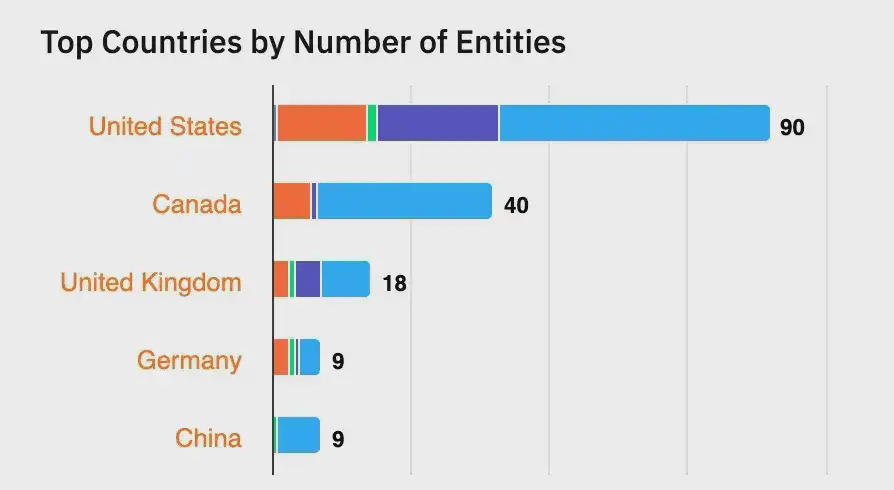

Among all entities holding Bitcoin, the United States and Canada rank at the top, followed by the United Kingdom. Notably, Japan's Metaplanet (ranked 5th) and China's Next Technology Holding (ranked 12th) are also noteworthy.

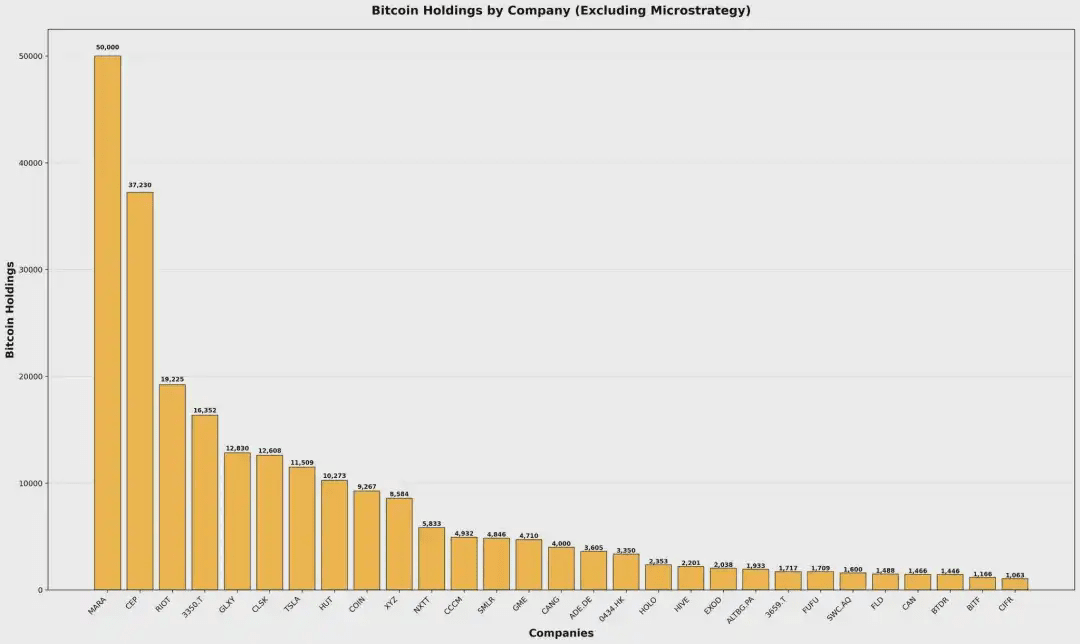

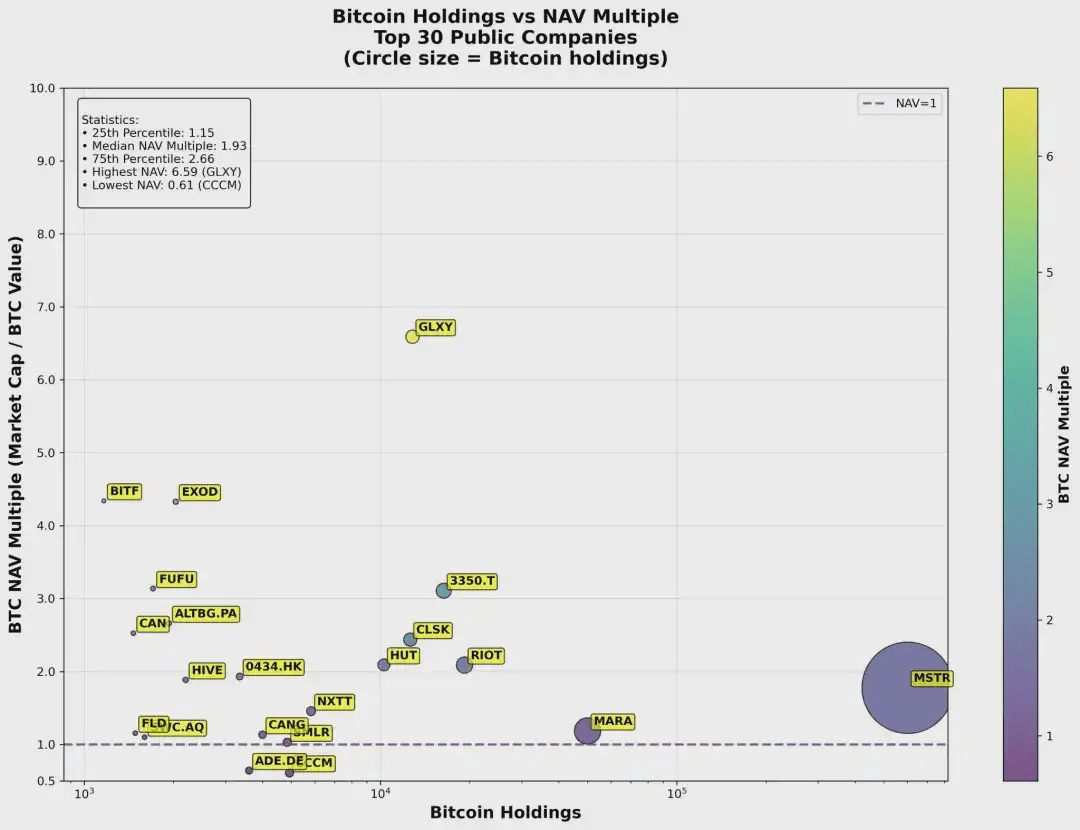

The following list shows the Bitcoin holdings of the top 30 publicly traded companies, with MicroStrategy significantly leading the pack.

Even excluding MicroStrategy, MARA and Twenty One Capital still rank highly, but the distribution of holdings remains highly concentrated—most companies outside the top ten hold Bitcoin in moderate quantities compared to leaders.

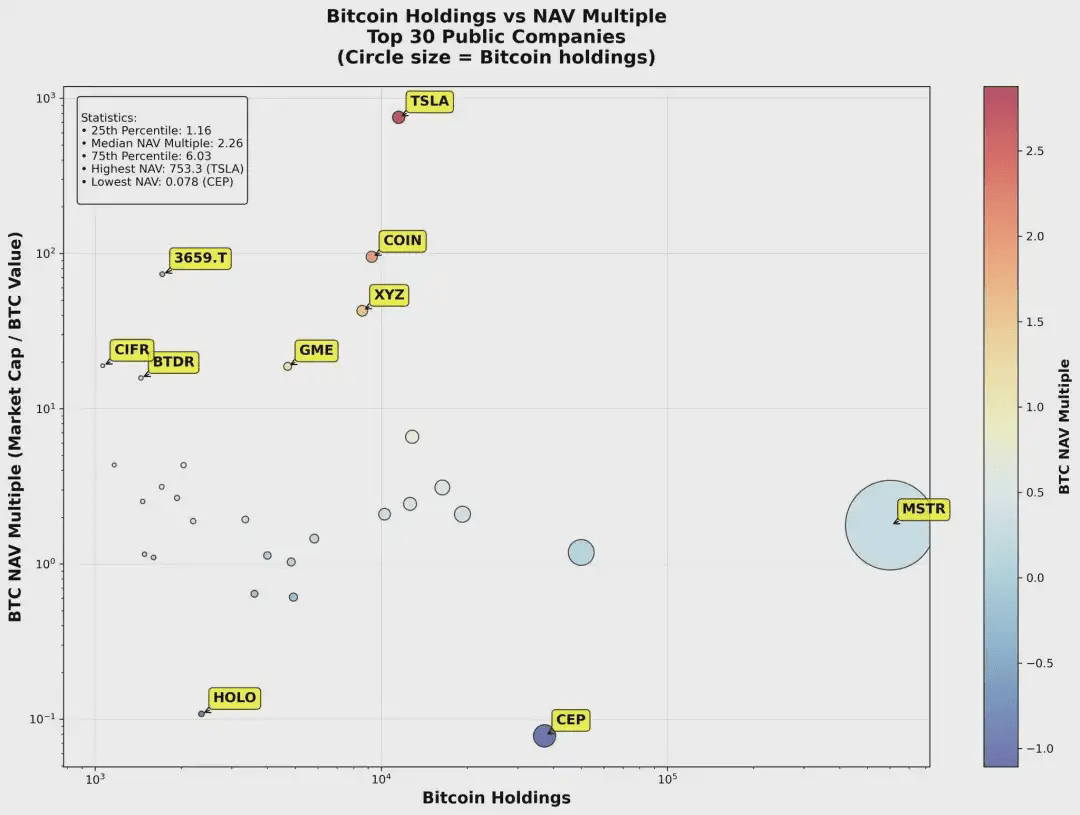

When evaluating the Bitcoin reserves of publicly traded companies, two indicators are particularly worth noting:

Present value to cost ratio

Comparing the current dollar value of Bitcoin holdings with the initial payment cost. A higher ratio indicates substantial unrealized gains—enhancing return rates while providing a buffer against market volatility.

Bitcoin Net Asset Multiple (BTC NAV Multiple)

The calculation method for mNAV is to divide the company's market value by the dollar value of its Bitcoin reserves; some companies use enterprise value (EV) instead of market value when reporting mNAV.

This multiple reflects investors' premium assessment of the core business beyond the company's crypto assets.

When mNAV > 1, the market values the company higher than its Bitcoin holding value, indicating that investors are willing to pay a premium for every unit of 'Bitcoin holding.'

The key is that mNAV > 1 can achieve anti-dilution financing: when mNAV > 1, the company can issue new shares → purchase Bitcoin → increase the net asset value of Bitcoin → drive enterprise value (EV) growth, while increasing the per-share Bitcoin holding.

Analysis of the NAV multiples of the top 30 companies shows significant differences among groups, such as Tesla (TSLA) and Coinbase (COIN). Since these companies do not primarily focus on Bitcoin reserves and have other core businesses, their NAV multiples are correspondingly higher.

Excluding non-Bitcoin reserve companies, most companies actually trade at high NAV multiples—many exceeding 2. Only four are below NAV = 1, while large holders like MSTR and MARA do not exhibit the extreme multiples seen among smaller companies.

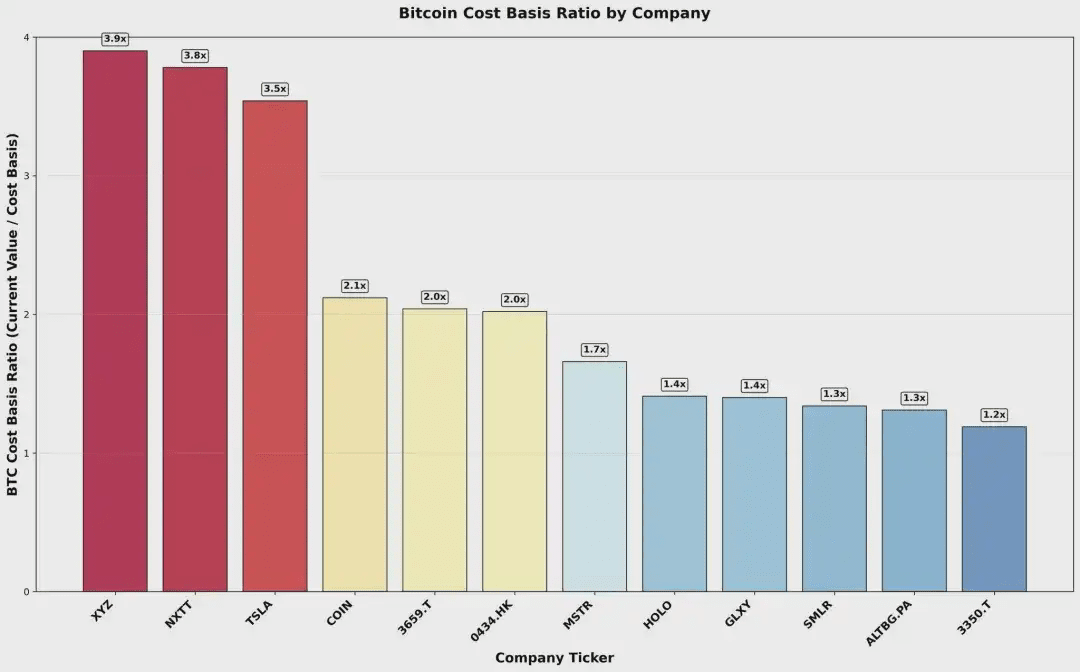

According to data from BitcoinTreasuries.net, companies that provide comprehensive public disclosures indeed exhibit high cost basis ratios, reflecting substantial unrealized gains—likely because companies with more substantial gains are more inclined to disclose relevant information.

Metaplanet Inc. (MPLAN)

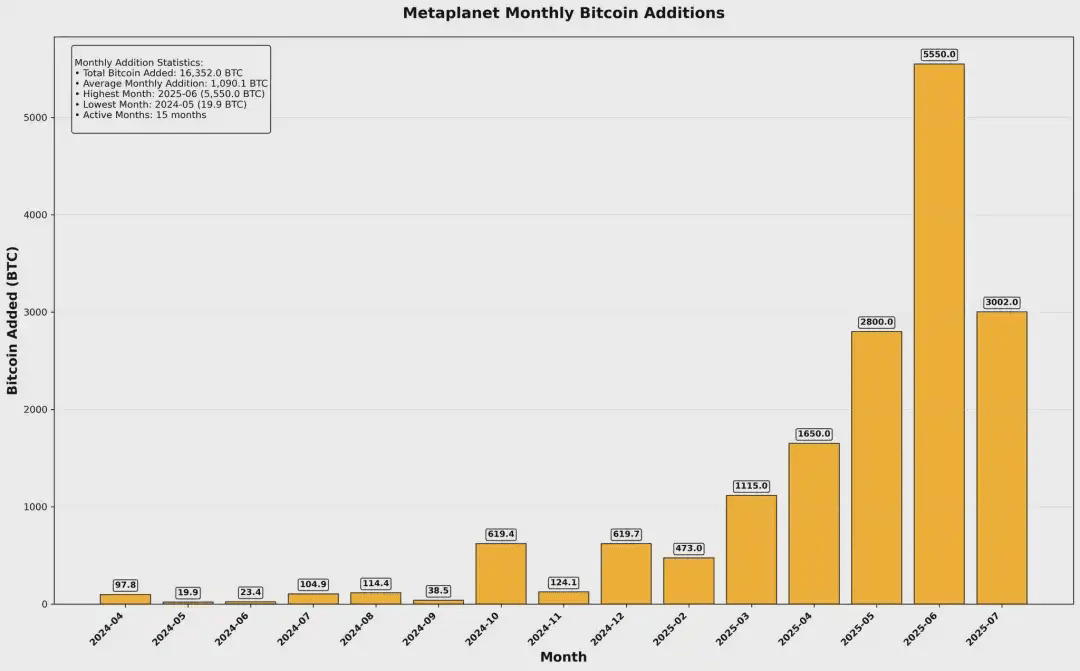

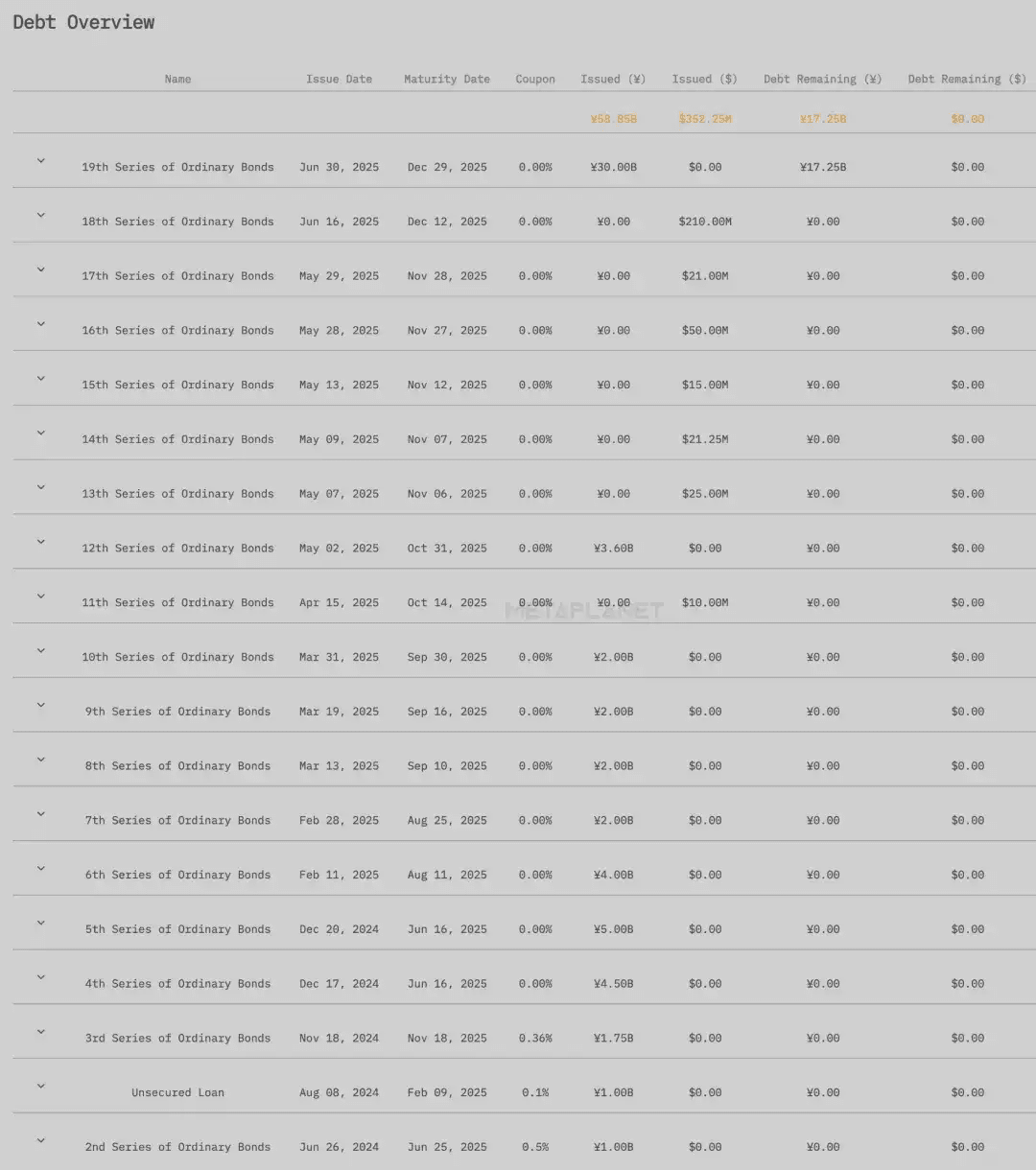

Among the many publicly traded companies emulating MicroStrategy's strategy, one Japanese company stands out—Metaplanet. To date, it has accumulated 16,352 Bitcoins, ranking among the top five publicly traded companies holding Bitcoin, and has significantly accelerated its acquisition pace in recent months.

bitcointreasuries.net, IOSG

As it describes itself: 'Raising $500 million in equity capital', 'Japan's largest equity issuer in 2025', 'the largest zero-cost financing in history.'

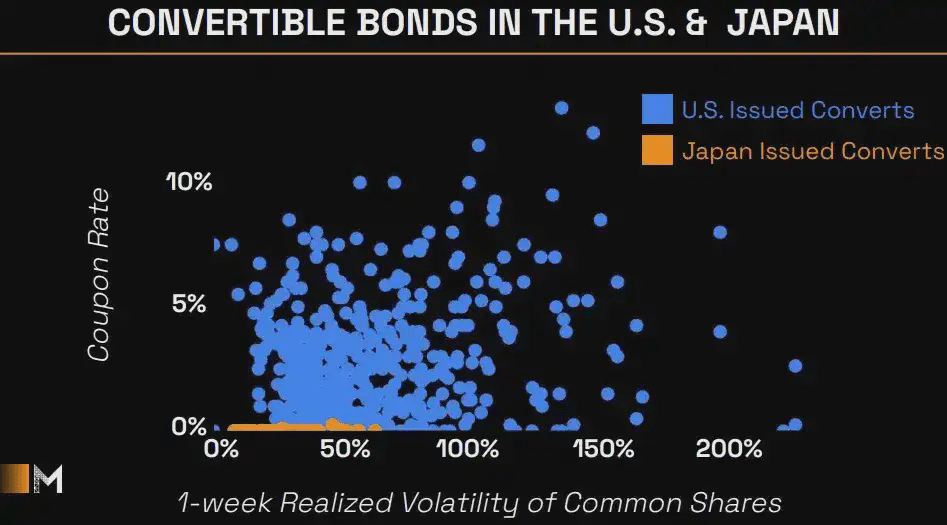

Japan's interest rates have long remained low, only being raised to 0.25% in July 2024, and again to 0.5% in January 2025, currently maintaining at 0.5%. This interest rate differential is also evident in the convertible bond market: as illustrated by Metaplanet's charts, convertible bonds issued in the U.S. typically come with higher coupon rates, while Japanese issues feature very low rates and minimal volatility.

Although Japan's market interest rates are generally low, Metaplanet's 'zero-interest financing' is not cost-free—the company balances costs by granting stock appreciation rights (SARs) as compensation.

Metaplanet initially raised cash by issuing zero-interest bonds for six months at par. To ensure repayment capability, the company granted corresponding stock appreciation rights (SARs) to the EVO fund based on the same board resolution.

Bond covenants stipulate that at maturity, Metaplanet must use cash paid for the above SARs at floating exercise prices to redeem the bonds as the sole source of funding.

Through this arrangement, Metaplanet avoids any regular interest expenses.

The EVO fund's revenue sources include dual protections:

1. Principal protection: Bonds are fully repaid in cash at maturity, avoiding the risk of a decline in the underlying stock.

2. Upside gains: When Metaplanet's stock price exceeds the floating exercise price, the EVO fund obtains the difference in profits between the market price and the exercise price by exercising the SARs.

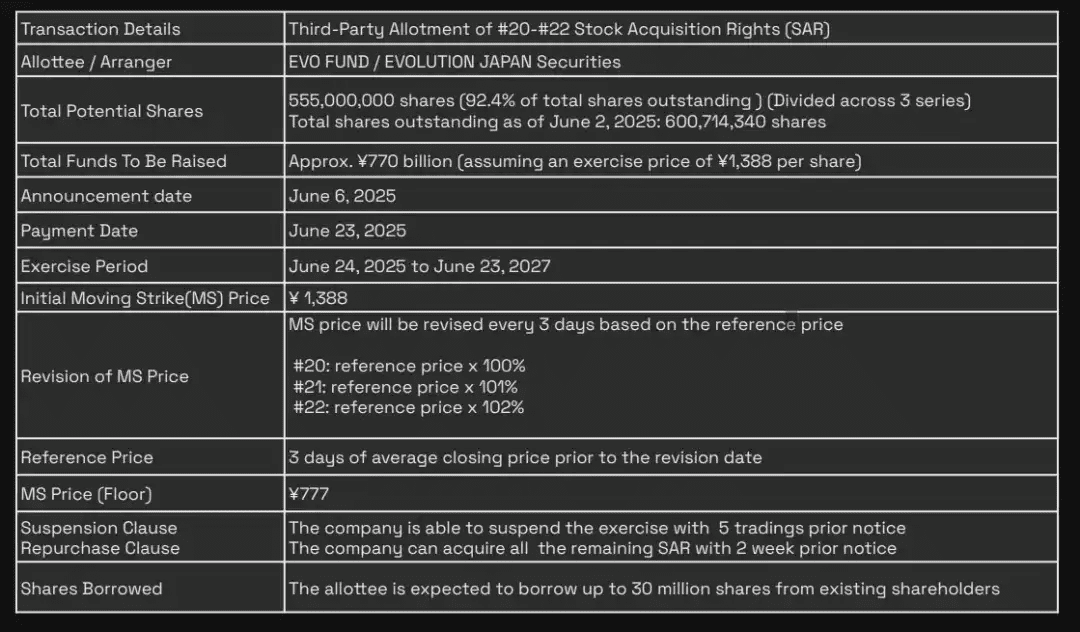

Launched on June 6, 2025, the '5.55 Billion Plan' (SAR numbers #20-#22) is Metaplanet's largest single financing scheme to date. A total of 555 million stock appreciation rights (SARs) were issued, equivalent to 92.4% of 600.7 million outstanding shares, with a maximum financing potential of 770 billion yen after exercise. The initial floating exercise price for this right is set at 1,388 yen per share, adjusted every three trading days based on the average closing price of the previous three days at 100%/101%/102%, but not lower than a guaranteed minimum price of 777 yen.

The EVO fund can be exercised at any time between June 24, 2025, and June 23, 2027, during which Metaplanet will issue new shares and obtain exercised funds. To control equity dilution and market impact, Metaplanet may announce a suspension of exercise five trading days in advance or notify buybacks of unexercised shares two weeks in advance.

Tax advantages represent another core value: in Japan, capital gains and dividends on stocks are subject to a single tax rate of about 20%, while profits from spot Bitcoin trading are classified as miscellaneous income, subject to a progressive national tax rate of 5%-45%, plus a 10% local resident tax (and applicable surcharges), with a combined tax rate of up to 55%. For investors in higher tax brackets seeking Bitcoin exposure, Metaplanet becomes a highly attractive alternative—especially since Japan has not yet approved the listing of spot Bitcoin ETFs.

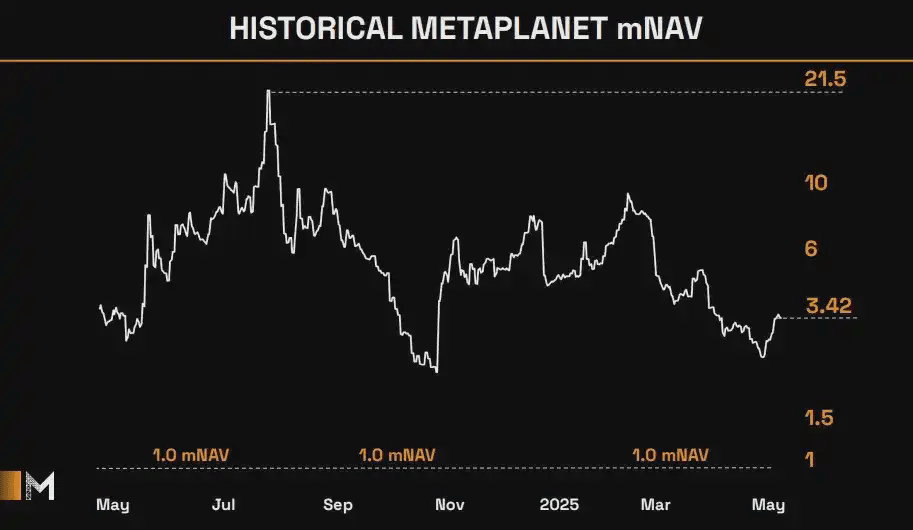

Metaplanet has historically traded at a high mNAV multiple—usually over 5×, even rising to 20× at one point, far exceeding other major holders. While this premium reflects investor confidence in its financing structure, tax advantages, and optimized Bitcoin yields, it also brings higher risks and may imply that its stock price is overhyped.

Other Bitcoin reserve enterprises: riding the SPAC wave.

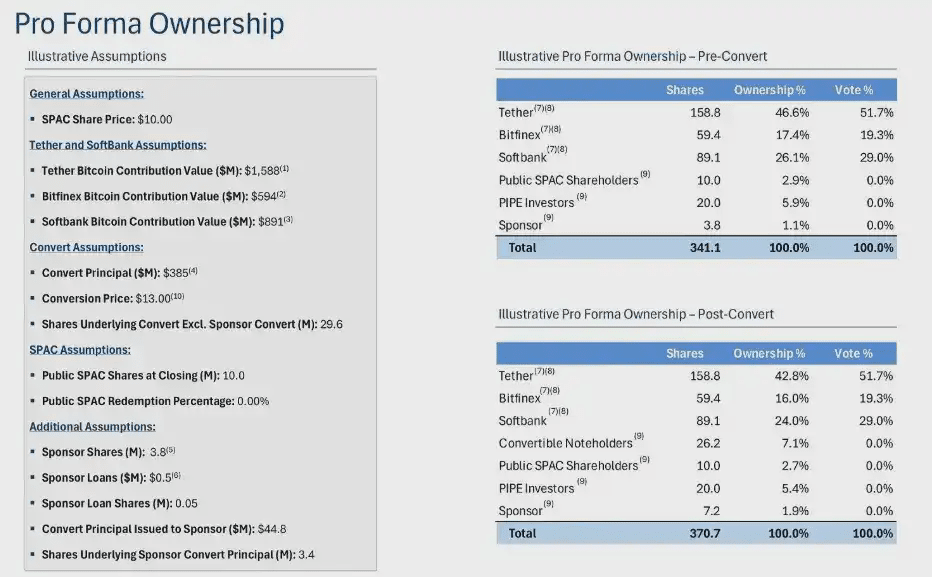

Many companies are racing to emulate MicroStrategy's Bitcoin reserve strategy. Notably, SPAC companies like Twenty One Capital (ranked 3rd) and ProCap Financial (ranked 13th) have leapfrogged to become top holders through complex fundraising structures immediately after completing their mergers.

Twenty One Capital, Inc.

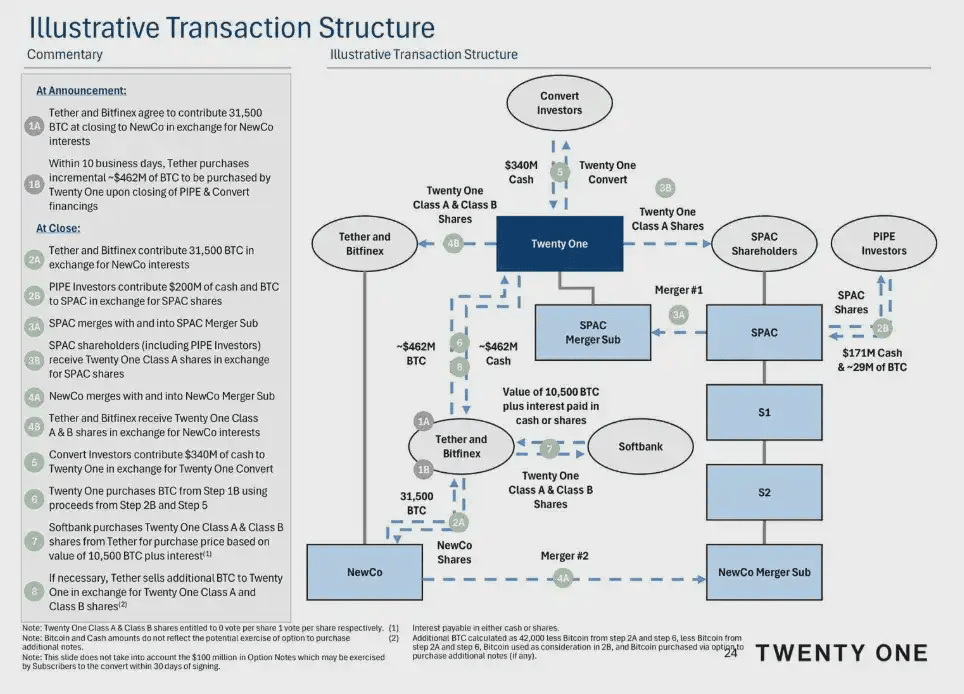

Co-founded by Strike CEO Jack Mallers. Twenty One's SPAC path integrates physical Bitcoin commitments, PIPE, and convertible bond financing, along with a two-step merger structure, enabling the company to list on NASDAQ with a fully funded reserve of 42,000 Bitcoins on its first day.

The transaction began with Tether and Bitfinex committing to provide 31,500 Bitcoins to a private entity called NewCo, while Tether additionally invested $462 million to purchase Bitcoin. A $200 million PIPE funded the SPAC trust, which was then merged into its subsidiary and issued Class A shares to SPAC and PIPE investors.

Meanwhile, NewCo completed the merger with the same merger subsidiary through stock swaps, exchanging Class A and Class B shares. Simultaneously, a $340 million convertible bond financing was directly injected into Twenty One. Twenty One then used the funds from PIPE and convertible bonds to repurchase the Bitcoins previously promised from Tether and Bitfinex. SoftBank, as a strategic anchor, subscribed for equity equivalent to 10,500 Bitcoins, and if the final reserve does not reach the target of 42,000 Bitcoins, Tether will be responsible for covering the shortfall.

After completing the SPAC merger, Twenty One's control will mainly be held by Tether and its affiliated exchange Bitfinex, while SoftBank Group will hold a significant minority stake.

Tether and Bitfinex each committed large amounts of Bitcoin in exchange for newly issued shares before the merger, ultimately holding controlling shares (Tether 42.8%, Bitfinex 16.0%). SoftBank then purchased equity equivalent to 10,500 Bitcoins at the same price, obtaining a similar proportion of shares (24.0%). In contrast, the cash of the SPAC trust (approximately $100 million) and the PIPE and convertible bond holdings are comparatively less.

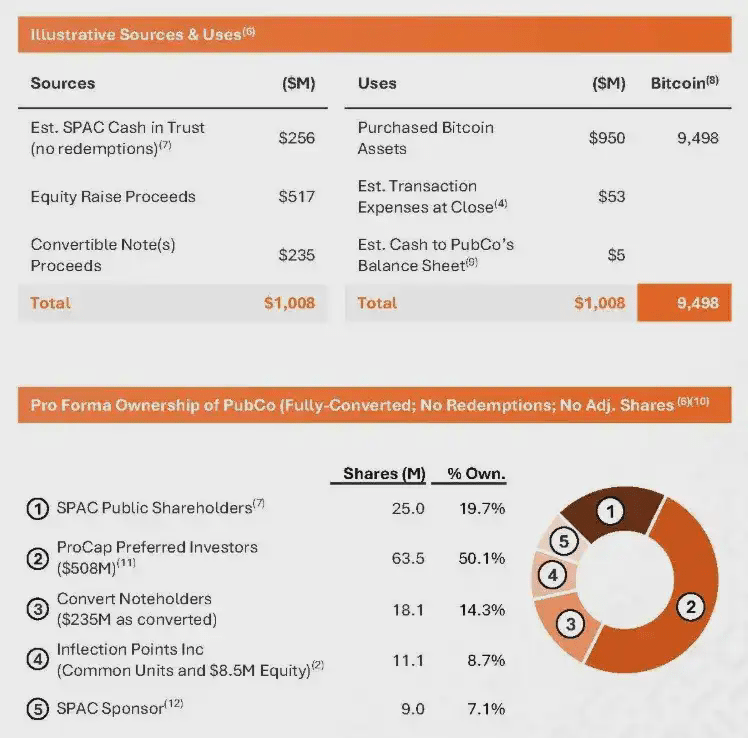

ProCap BTC (PCAP)

ProCap Financial raised a total of $1.008 billion to launch its Bitcoin reserve platform, of which $256 million came from SPAC trust (assuming minimal redemptions), $517 million from preferred stock PIPE, and $235 million from zero-interest, preferred secured convertible bonds. Nearly 95% of the total fundraising (approximately $950 million) was immediately invested in acquiring 9,498 Bitcoins.

ProCap BTC Investor Deck

Public SPAC shareholders swapped $256 million in trust for 25 million shares, accounting for 19.7%; led by Magnetar Capital, ParaFi, Blockchain.com Ventures, Arrington Capital, Woodline Partners, Anson Funds, RK Capital, Off the Chain Capital, FalconX, BSQ Capital, and others, $517 million in preferred stock PIPE was underwritten for 63.5 million shares, accounting for 50.1%; $235 million in zero-interest, preferred secured convertible bonds converted into 18.1 million shares, accounting for 14.3%; Inflection Points Inc. swapped its existing shares and invested an additional $8.5 million in equity subscriptions, acquiring 11.1 million shares, accounting for 8.7%; while the SPAC sponsors retained 9 million shares of promote, accounting for 7.1%.

Although SPAC projects generally perform poorly, Bitcoin reserve SPACs are still recognized for their transparency in holdings and cost basis. Their S-1/S-4 filing documents comprehensively disclose the cash contributions, equity allocations, and physical Bitcoin contribution values of each participant (for example, Twenty One Capital's $200 million PIPE financing corresponds to a $10 exercise price per share, and $385 million in zero-interest convertible bonds at a $13 conversion per share, clearly detailing the number of shares before and after conversion). Since these enterprises share a similar 'acquire and hold Bitcoin' business model, such disclosures provide reliable references for investors to assess the degree of equity dilution, holding costs, and reserve composition.

Compared to recent reliance on complex SPAC financing models, early adopters like Next Technology Holding accumulate Bitcoin reserves through more direct equity cash transactions.

Meanwhile, GameStop's actions are also noteworthy: on May 28, 2025, this game retailer with cash reserves of $4.8 billion announced that as part of its digital asset strategy, it had spent approximately $513 million to acquire 4,710 Bitcoins.

Cash-rich crypto platforms

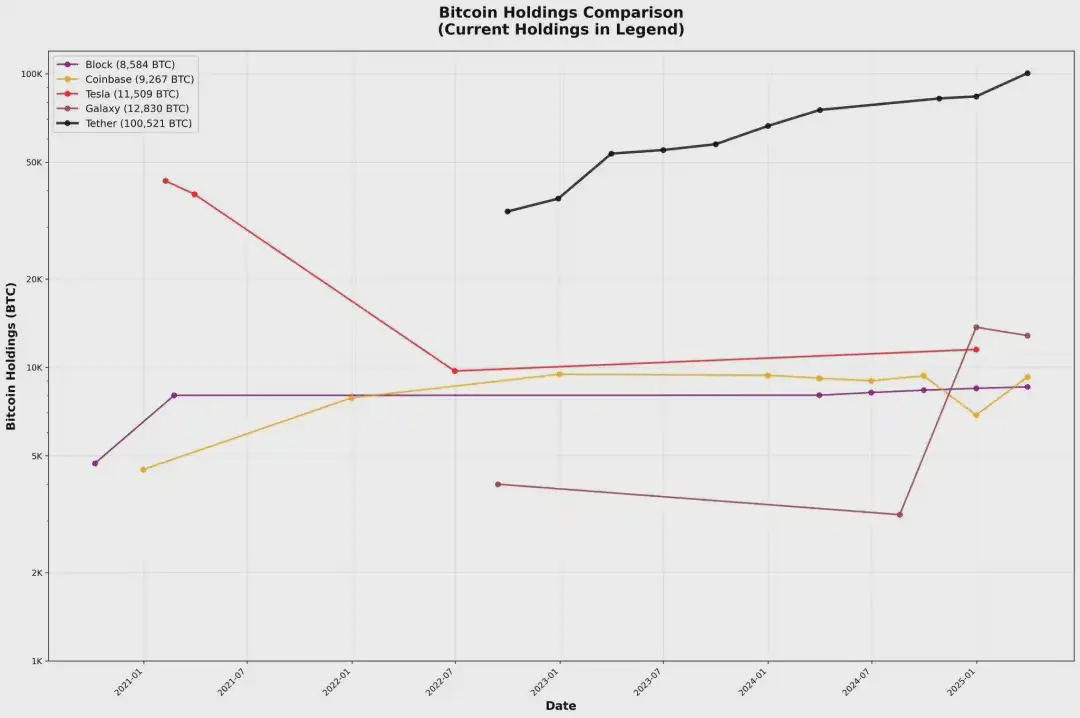

While many companies are emulating MicroStrategy's full Bitcoin strategy, there are also many native crypto platforms that continue to invest in digital assets steadily, with occasional one-time large buyers like Tesla.

Tether, the issuer of USDT, has actively incorporated Bitcoin into its reserves since the end of 2022, allocating up to 15% of its net profits each quarter for direct market purchases and renewable energy mining investments. As its CTO Paolo Ardoino stated: "By holding Bitcoin, we are adding a long-term asset with upside potential to our reserves," Tether also noted that this move "will enhance market confidence in USDT by diversifying reserves into digital asset value storage." As a result, Tether's Bitcoin reserves have seen quarterly growth since 2023—currently doubling to over 100,000 Bitcoins, accumulating approximately $3.9 billion in unrealized gains.

Block (formerly Square) made its first 'bet' in October 2020—purchasing 4,709 Bitcoins for $50 million, which accounted for approximately 1% of its assets at that time. In the first quarter of 2021, it added another $170 million (3,318 Bitcoins), raising its reserve to over 8,000 Bitcoins. Since then, Block has maintained its Bitcoin holdings. In April 2024, Block launched an enterprise-level dollar-cost averaging plan, using 10% of the gross profits from Bitcoin products to systematically purchase Bitcoin at the two-hour weighted average price through over-the-counter liquidity providers.

Coinbase officially established its corporate Bitcoin strategy in August 2021, with the board approving a one-time $500 million purchase of digital assets and committing 10% of quarterly net profits to an investment portfolio that includes Bitcoin.

In January 2021, Tesla's board approved a $1.5 billion purchase of Bitcoin, citing that "we believe in the long-term potential of digital assets as an investment, as well as their value as a cash alternative." Months later, CEO Elon Musk stated that Tesla sold about 10% of its Bitcoin "to prove liquidity," realizing $128 million in gains in the first quarter of 2021; in the second quarter of 2022, Tesla sold the remaining approximately 75% of its holdings, with Musk explaining that this was to "maximize cash position amidst production challenges due to the pandemic in China," while emphasizing that "this should not be viewed as a negative judgment against Bitcoin."

Ethereum

Many companies have joined the Ethereum reserve camp with the same enthusiasm as MicroStrategy's Bitcoin strategy—the driving force behind this is the bullish outlook on ETH, staking rewards, and the fact that ETH ETFs cannot currently participate in staking. As Wintermute founder Evgeny Gaevoy stated on July 17: "Clearly, there’s hardly any ETH available on Wintermute's OTC desk."

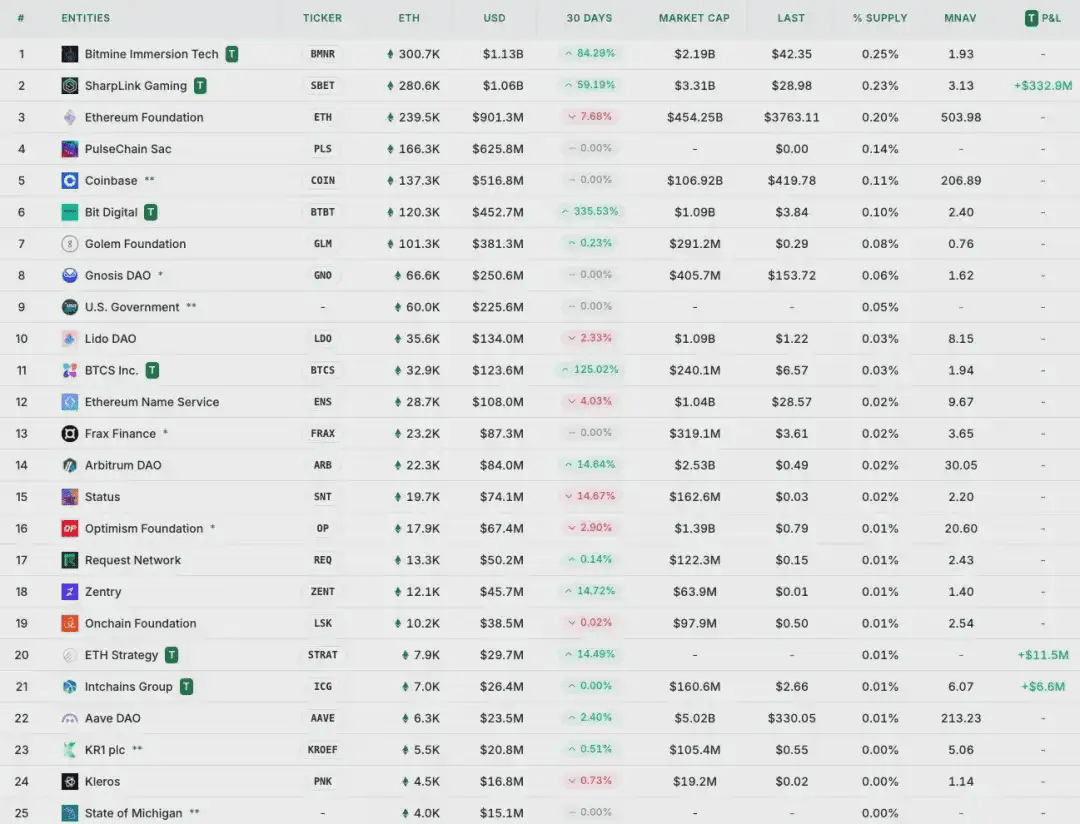

Companies participating in the Ethereum reserve strategy are marked with a 'T' symbol. Leading companies include BitMine, SharpLink, Big Digital, and BTCS, each significantly increasing their holdings in the last 30 days, reflecting their proactive ETH accumulation trend.

Although BitMine and SharpLink's holdings have surpassed the Ethereum Foundation, their individual positions remain moderate compared to MicroStrategy, which controls nearly 2.865% of the circulating Bitcoin supply—accounting for approximately 0.25% and 0.23% of the total supply, respectively. Furthermore, these Ethereum reserve projects mostly initiated between May and July of this year and are still very recent developments.

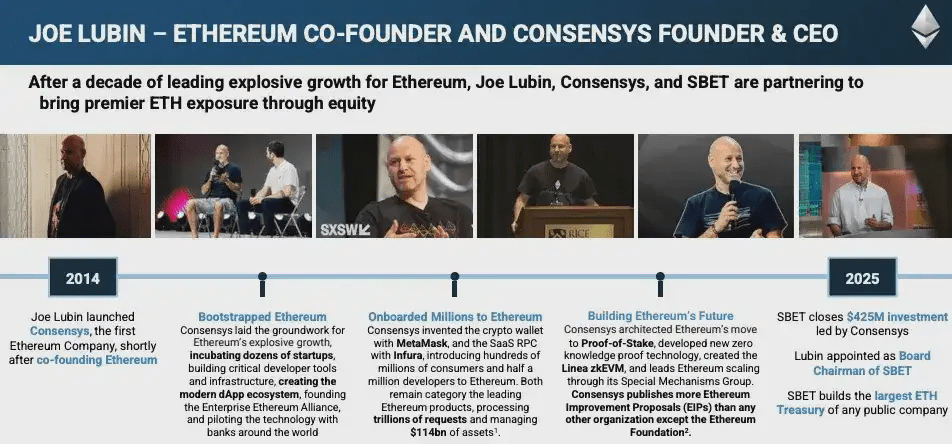

SharpLink Gaming (NASDAQ: SBET)

SharpLink Gaming is an iGaming affiliate company listed on NASDAQ, which announced the launch of its Ethereum reserve strategy through a $425 million private placement in 2025.

SharpLink built this strategy around two financing channels: large PIPE (private investment in public equity) and ATM (at-the-market) equity mechanisms. On May 27, 2025, SharpLink announced the completion of a $425 million PIPE led by major crypto venture capital firms like Consensys (a company of Joe Lubin) and ParaFi Capital, Electric Capital, Pantera Capital, Arrington Capital, GSR, Primitive Ventures, among others.

Upon completion of the transaction, Lubin joined SharpLink's board and serves as the chairman, responsible for guiding the strategic direction of the Ethereum reserve project.

After completing the PIPE, SharpLink initiated an ATM distribution mechanism to sell stock to the market based on demand. For example, by the end of June 2025, they raised approximately $64 million through ATM sales, and at the beginning of July 2025, they sold 24.57 million shares, raising about $413 million.

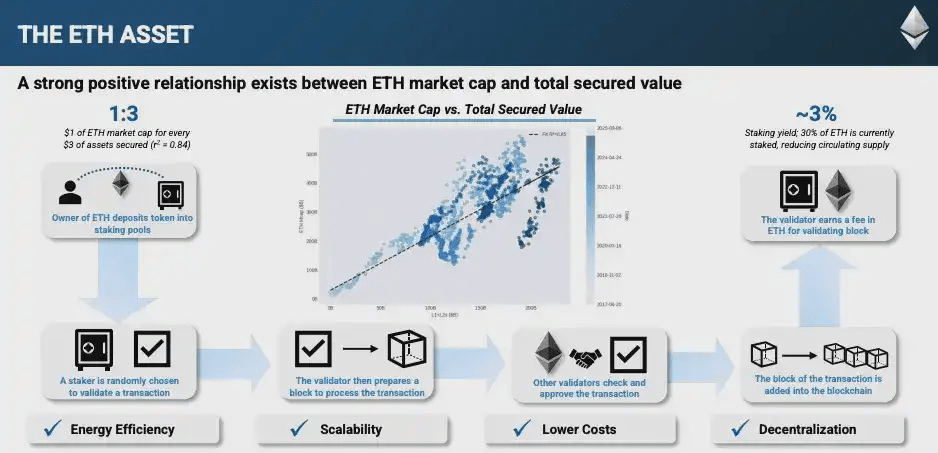

At the same time, SharpLink committed to using nearly 100% of its ETH holdings for staking to earn yields. As of mid-July 2025, approximately 99.7% of its Ethereum assets were participating in staking.

On July 10, 2025, SharpLink reached a final agreement with the Ethereum Foundation to directly purchase 10,000 ETH, paying a total price of $25,723,680 (equivalent to $2,572.37 per ETH). This was the first OTC transaction between the Ethereum Foundation and a publicly listed company.

SharpLink's Ethereum reserve value proposition is based on four core pillars: attractive staking yields, high total value collateral (TVS), operational efficiency, and broader network effects. Staking rewards not only provide a stable income buffer for reserve allocations but also help offset acquisition costs. To date, Ethereum's TVS has reached $800 billion, with a security ratio of 5.9×—the total value of on-chain collateralized ETH, ERC-20 tokens, and NFTs ($800 billion) divided by the value of staked ETH ($140 billion). In addition to these financial metrics, Ethereum boasts superior energy efficiency compared to proof-of-work networks, with thousands of independent validators achieving deep decentralization and a clear scalability roadmap through sharding and Layer 2 solutions.

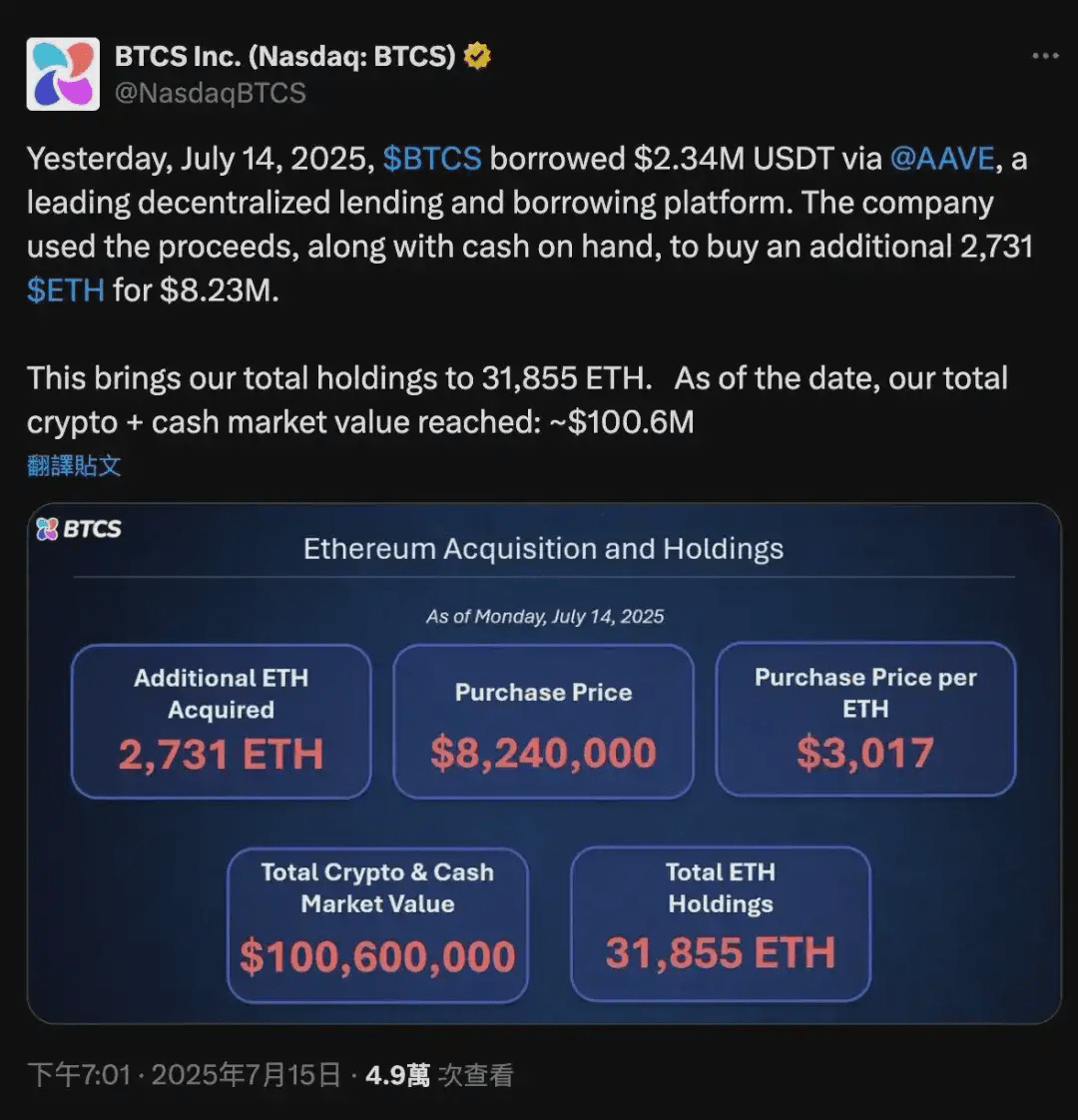

BTCS Inc. (NASDAQ: BTCS)

On July 8, 2025, BTCS (Blockchain Technology & Consensus Solutions) announced plans to raise $100 million in 2025 for its Ethereum reserve acquisitions.

BTCS has developed a hybrid financing model, combining traditional financing with decentralized finance: funding ongoing ETH accumulation through ATM equity sales, convertible bond issuance, and on-chain DeFi borrowing via Aave.

On the on-chain side, BTCS's strategy centers around Aave: the company borrows USDT against ETH as collateral on the Aave protocol, then uses the funds obtained to purchase additional ETH. Subsequently, BTCS stakes these ETH through its NodeOps validator network to earn rewards. CEO Charles Allen emphasized that this low-dilution, steady approach—'slow and steady wins the race'—aims to increase the per-share ETH holding at the lowest possible cost.

For instance, in June 2025, BTCS borrowed an additional $2.5 million USDT on Aave (bringing its total Aave debt to $4 million), using approximately 3,900 ETH as collateral. In July 2025, it borrowed another $2.34 million USDT (total Aave debt approximately $17.8 million), using about 16,232 ETH as collateral.

Most newly acquired ETH is used for staking. BTCS connects these ETH to its NodeOps validator network while operating independent validator nodes and RocketPool nodes.

BTCS’s on-chain strategy is quite innovative—integrating DeFi into the strategic reserve strategy. However, its cost advantages depend on the interest rate environment on the Aave platform, and leveraged operations carry inherent risks. Meanwhile, the surge in demand for ETH from other companies focused on reserve management may reduce on-chain liquidity. As a potential exacerbator of this trend, BTCS may support prices in the short term, but its long-term impact needs close monitoring—especially when its positions are sufficient to influence the Aave market.

Other Companies

BitMine Immersion Technologies (NYSE American: BMNR)

On July 8, 2025 (initial financing), the crypto mining company BitMine launched a 'light asset' Ethereum reserve strategy and completed a $250 million private placement (PIPE) to purchase ETH on the same day. Within a week, BitMine acquired approximately 300,657 ETH. The company publicly stated that its long-term goal is to 'acquire and stake 5% of all ETH.'

Bit Digital (NASDAQ: BTBT)

On July 7, 2025. Originally focused on Bitcoin mining, Bit Digital announced it has completed its transition to an Ethereum reserve strategy. According to its press release on that day, Bit Digital raised approximately $172 million through public stock offerings and liquidated 280 Bitcoins on its books, reinvesting the proceeds into Ethereum. As a result, the total amount of ETH held by the company reached approximately 100,603 (having accumulated continuously through staking since 2022).

GameSquare Holdings (NASDAQ: GAME)

On July 10, 2025, digital media/gaming company GameSquare launched an Ethereum reserve plan of up to $100 million. In the announcement on that day, GameSquare confirmed an initial investment of $5 million to purchase approximately 1,818 ETH at a price of around $2,749 each. The company raised an initial $9.2 million through a public stock offering in July, then announced an additional $70 million follow-on placement (with the option to upsize to $80.5 million) to further expand its ETH reserves.

Conclusion

The surge in corporate crypto asset reserves has far exceeded the scope of Bitcoin and Ethereum—many companies are expanding their reserve layouts to include SOL, BNB, XRP, HYPE, among others, seizing opportunities.

However, most projects suffer from severe homogeneity and lack sustainable competitive advantages, so their NAV premiums are likely to be eroded over time by more strategically advantageous competitors.

Truly advantageous companies often have stronger financing structures and strategic partnerships. For example, Metaplanet benefits from Japan's favorable tax treatment on stocks and the market environment lacking BTC spot ETFs; Twenty One adopts a complex financing structure to leverage all available channels to acquire Bitcoin—and has established strategic partnerships with Tether, Bitfinex, and SoftBank to become the third largest holder, maximizing its scale advantages. Meanwhile, SharpLink is led by Consensys and top crypto VCs, with Joseph Lubin joining its board, while BTCS is involved in the Ethereum DeFi ecosystem.

It is crucial for public investors to remain cautious: under significant hype, many companies are still at high NAV multiples, with their stock prices often fluctuating due to announcements—while investors typically lack the transparent, real-time information needed to assess company changes. Additionally, broader market risks, especially in a bear market, can quickly erode any premiums brought about by these strategies.

In the institutional realm, an increasing number of crypto funds are allocating crypto reserve stocks and even launching dedicated funds. Meanwhile, seasoned industry veterans are getting involved as strategic advisors.