Author: Jesse

Compiled by: Deep Tide TechFlow

Earlier this month, I wrote an article about cryptocurrency asset management companies. If you are not familiar with this topic, I suggest you read that article first, as it builds on most of the same concepts.

The trend of cryptocurrency asset management companies represents a shift in the way capital flows on-chain (or how value created on-chain flows to investors).

The more these companies invest in other altcoins (just last week, we acquired TAO and Litecoin), the more market bubbles seem to emerge. However, publicly traded companies participating in ecosystems or other on-chain applications may bring some value, at least for some of the highest quality assets in the cryptocurrency realm.

This article covers the following points:

The flexibility and market-oriented nature of cryptocurrency asset management companies make them superior to ETFs.

Cryptocurrency asset management companies represent the ultimate form of institutional crypto, aligning investor sales with technology adoption.

In many cases, relying solely on a treasury reserve model is insufficient; teams must balance the ability to build asset financing with the ability to extract asset value through DeFi or other infrastructures.

Hyperliquid is particularly well-suited to this trend, potentially being more attractive compared to Ethereum or Solana.

Asset Management Companies VS ETFs

When investors have no other choice, asset management companies are clearly the ideal choice. However, if there are other options (such as ETFs), do they still make sense?

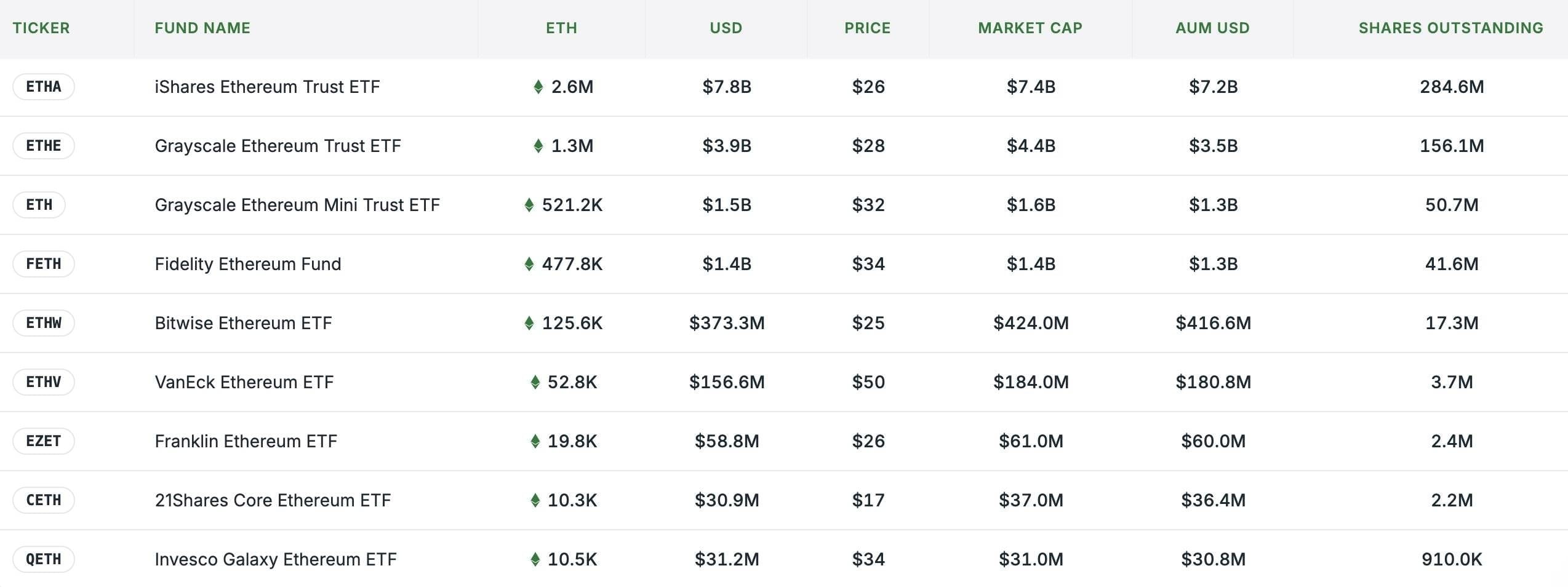

ETF listings do not mean the end of asset management companies. ETFs must be sold like any other investment product; the more popular and accessible the asset, the stronger the product's competitiveness. Therefore, the competition of ETFs ultimately heavily relies on trust or relationships rather than actual management advantages. For many investors, a simple asset exposure from a familiar brand may be more favored. Recently, there has been high demand for Ethereum ETFs, with total holdings approaching 5 million ETH.

That is to say, for specific cryptocurrency assets, asset management companies may be better than ETFs:

They can reach a wider variety of investor types; many investors may not be allowed to purchase ETFs or may prefer to buy fixed income, stocks, convertible bonds, etc. Asset management companies can build trades targeting these types of investors.

Asset management companies are able to maximize the productivity of core assets, creating value for shareholders—that is, compared to waiting for ETH staking ETFs to be approved, asset management companies can freely stake ETH directly.

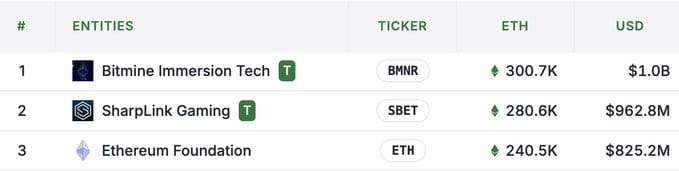

This is why, despite multiple ETH ETFs, the amounts of ETH accumulated by @BitMNR($BMNR) and @SharpLinkGaming($SBET) have surpassed many ETFs (both sizes fall between those mentioned above, Bitwise and Fidelity). The amounts of ETH they are currently accumulating also exceed those of the Ethereum Foundation:

The second point is crucial for every asset management company because the best companies are deeply integrating into DeFi. Currently, the frontrunners seem to be Sharplink in the Ethereum space and @defidevcorp ($DFDV) in the Solana space. By its name, DFDV clearly indicates its positioning, while Sharplink directly promotes Ethereum as 'DeFi on Nasdaq.'

Original tweet link: Click here

Ecosystem Asset Management Companies: A New Form of Institutional Cryptocurrency

Companies that invest in and use native assets of the chain or DeFi infrastructure are nearing the ultimate form of institutional cryptocurrency adoption.

Previously, institutional entry into cryptocurrency could be divided into two paths: investment (such as Grayscale products or through funds) and technology application/adoption (such as enterprise blockchain or L2 payment cooperation). Now, entities holding blockchain tokens are beginning to truly utilize these tokens.

Companies that have cryptocurrency asset management businesses are also the ultimate regulatory arbitrage tool between traditional finance and cryptocurrency finance. Previously, pools of funds needing regulated counterparties could use asset management companies as operational tools for DeFi yields or other needs (to some extent, asset management companies using DeFi could replace the role of investment banks).

We have seen asset or region-specific asset management companies:

Original tweet link: Click here

However, we have yet to see them expand their services beyond just operating infrastructure or staking underlying assets for yield. If an operating company successfully scales the application of RWA with DeFi first, or if they are used as a vehicle to cross previously fragmented pools of funds through DeFi, I would not be surprised.

The special case of HYPE

For mature assets, the above discussion about ETFs and fund companies should reflect the trends we see in the market. Its model is roughly as follows:

ETF listings and/or asset management company financing → Each new company needs differentiation → They are pushed onto the chain in pursuit of returns → The acquisition of tokens is no longer a differentiating point; asset utility and DeFi profitability are the most important factors.

This makes companies inclined to invest in tokens that can yield higher quality, sustainable returns. For most assets where economic value occurs on-chain, such as ETH and SOL, companies can formulate strategies around how to capture value. (Conversely, it is hard to understand how or why an asset company lacking yield opportunities could survive in the long term.)

This is very beneficial for HYPE as an asset for asset management companies, as the token is closely related to the value generated from its product usage. Fees collected from traders on Hyperliquid accumulate and are used to regularly buy back HYPE tokens from the market. Besides the many more subtle mechanisms of HYPE's value, this is also the most straightforward for investors.

For equity holders of asset management companies, this provides a strong rationale for choosing to hold an asset that generates cash flow through cryptocurrency trading activities (and in a tax-advantaged manner) for the long term.

But another key reason HYPE makes a case for asset management companies is that, aside from adopting the core DEX, the development level of asset management companies is still not sufficient.

Compared to other assets, HYPE has little institutional presence, and the core DeFi protocols of the ecosystem are just beginning to launch and gain attention.

For today's asset management companies, the first point is the most important. Previous discussions about ETFs particularly support the case for HYPE. However, Hyperliquid ETFs seem unlikely to become the primary way for institutions to invest in HYPE, especially considering the early appeal of companies focused on HYPE (such as @HyperionDeFi, @HYLQstrategy, and @SonnetBio). Additionally, ETFs also need to fund liquidity, much of which has already flowed to these asset management companies. This may be one of the biggest differences between institutional market entry and market demand.

If a company can become the steward of the ecosystem, rather than just a traditional investor's asset exposure, then this opportunity becomes more attractive. The Hyperliquid ecosystem is still in its early development stages, offering a company an open opportunity to become a key player in DeFi protocol and infrastructure design/operation.

We have already seen this phenomenon in the market: The launch of @kinetiq_xyz LST was split into a dedicated procurement for asset management company partners for institutional HYPE (iHYPE).

Original tweet link: Click here

Aside from product design or development, the company may also invest in early protocols within the ecosystem. This is also a great complement for companies that are raising funds, as they can sell exposure to underlying assets, operate infrastructure for the ecosystem, and provide investors with venture-like returns.

This contrasts with the following situation: $SBET and DeFi protocols: Although they hold more ETH than the Ethereum Foundation, the underlying DeFi they use may have become rigid or managed by a DAO. For example, Lido's staking has already expanded for institutional users. New asset management firms are less likely to become design partners for the new Lido. ETH staking is still profitable, but its agency mechanism is lower compared to building with the next Lido, which is closer to the reality of ultra-liquid asset management.

In any case, the farther a company is from the underlying DeFi protocols it uses, the fewer opportunities there are to capture value. This also explains why DFDV is promoting a franchise model, where they own the underlying infrastructure of other companies in various regions to build a brand and raise funds to purchase SOL.

Summary

Most token asset management companies will not gain a premium during a bear market, while those that do have competitive common assets will need to delve deeper into the ecosystem to demonstrate that they truly offer unique value.

From this perspective, power laws (Deep Tide Note: In power law distributions, the probability of most events occurring is small, while a very few events have a high probability of occurring.) may benefit some companies focused on specific assets. Those companies that cannot fully grasp the native demand of non-cryptocurrency assets will need to turn to other assets or on-chain activities. If they fail to do so, their modes of failure may vary greatly depending on the company and asset, which may be worth exploring in another article.