Written by: Yue Xiaoyu

With the listing of compliant stablecoin leader Circle, a benchmark effect has emerged, and domestic attention has also turned to stablecoins.

Various stablecoin payment conferences are emerging one after another, companies are organizing to learn, and of course, the crypto community is actively discussing, with scholars debating.

Behind the hustle and bustle, who has actually made money?

In fact, based on the overall process, the development of stablecoins can be divided into three stages, and these three stages have different roles that can make money.

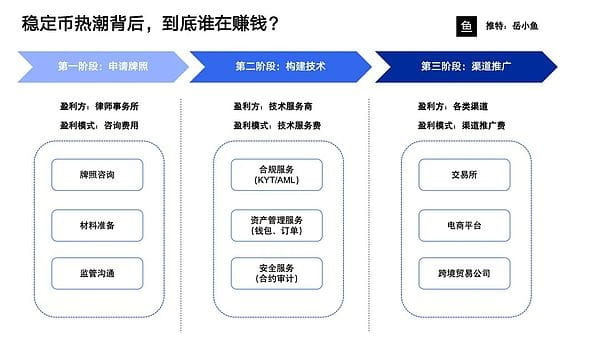

Phase one, applying for a license.

Compliance comes first, and currently everyone is applying for licenses in Hong Kong.

The biggest problem with Hong Kong regulation is its excessive strictness and numerous requirements; many companies do not know how to meet regulatory demands.

At this time, law firms emerged to provide legal consulting services to companies applying for licenses, helping them submit materials and communicate with regulators.

So at this stage, law firms have made money first.

Phase two, building technology.

Compliance and technology can proceed in parallel; many companies apply for licenses while building technical systems, so once the license is approved, they can immediately launch their stablecoins and seize the opportunity.

If the project is initiated after the license is obtained, it will miss the window of opportunity and be far too late.

Doing stablecoin payments is quite complex, requiring compliance services, asset management services, token issuance services, liquidity management services, security services, and so on.

Specifically includes KYB, KYT, AML, order management, address management, clearing and settlement, deposits and withdrawals, contract audits, on-chain security, and so on.

However, traditional Web2 companies actually lack relevant experience and talent accumulation in blockchain development, so they need to cooperate with Web3 technology service companies.

Therefore, at this stage, many crypto technology service providers also began to attract clients and directly generate income.

Phase three, channel promotion.

If a license is obtained and technology is well-established, then business can be conducted directly.

However, currently, the vast majority of companies are still in the first and second phases, with the third phase at most in negotiation.

However, once the business is launched, it will lead to a situation of a 'battle of hundreds of cryptocurrencies.'

For stablecoins, liquidity is key.

Various stablecoins need to find their own business scenarios and expand their usage scale.

Thus, channel promotion is very important, and it is necessary to find high-volume channels for cooperation.

A typical example is Circle, where USDC rapidly rose mainly due to the strong support and liquidity provided by Coinbase.

This is a clear development path; for Hong Kong stablecoin players, it is necessary to bind various channels to seize the market.

In this stage of the battle of various cryptocurrencies, the most profitable are various channels, including exchanges, e-commerce platforms, cross-border trade companies, and so on.

After going through the aforementioned three phases, only then can stablecoins truly make money.

In the end, one stablecoin will emerge to become the leader in the Hong Kong region or the Chinese-speaking area, squeezing out the space for other competitors and gaining the vast majority of market share through a siphon effect.

Once a solid market share is established, the next step is to increase profitability; this is when stablecoin issuers start to make money.

Referring to domestic battles in ride-hailing, shared bicycles, and food delivery, they all follow such paths.

Initially, it was a chaotic battle, and the last players standing would take all; after a subsidy war, they need to recuperate and reduce subsidies while increasing prices to make a profit.

At this time, profits are also quite terrifying; stablecoin issuers rely on large asset volumes to be profitable.

Apart from various project parties, for ordinary users, a more direct benefit is that new stablecoin forces can seize the market and liquidity through subsidies, allowing us retail investors to profit.

In summary, the craze for stablecoins can be described as 'the bigger the water, the bigger the fish'; we need to grasp our own piece of the pie.