(The following content is sourced from A1 Research, translated by Chain News, with the original title: The Hidden Mechanics Behind Ethereum’s Rally: Understanding Market Structure and Systemic Risk)

The movement of Ethereum's price appears simple: retail enthusiasm is high, prices are rising, and optimistic sentiment accumulates. But beneath the surface lies a structurally complex dynamic involving funding markets, Delta neutral trading desks, and recursive leverage demands, revealing the deep fragility of the current cryptocurrency market.

We are witnessing an extraordinary phenomenon: leverage has essentially become liquidity itself. The scale of long positions deployed by retail participants is fundamentally reshaping the risk allocation of neutral capital, bringing about a new type of market fragility that most market participants have yet to understand.

Retail long machine: When everyone wants to make the same trade.

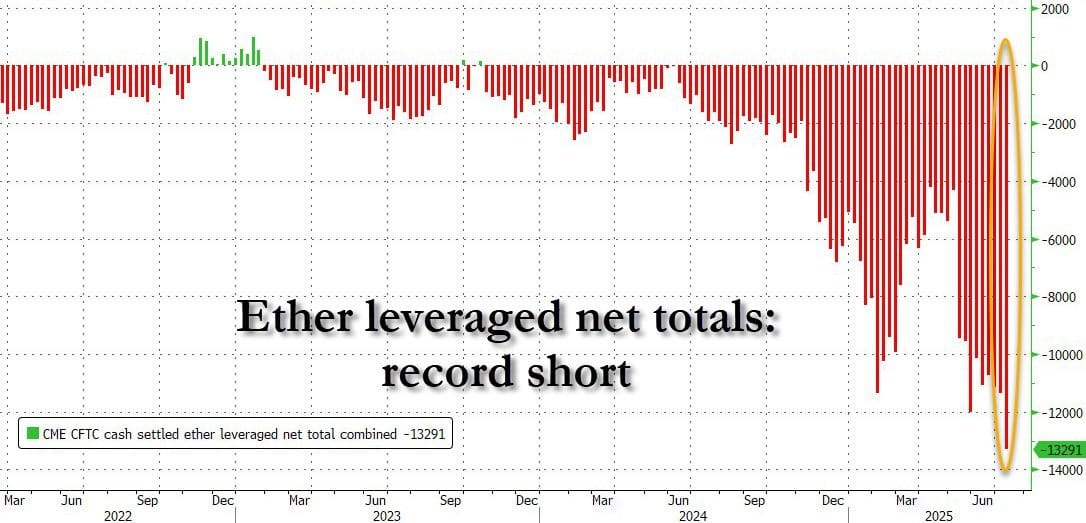

Retail demand is concentrated in ETH perpetual contracts, where leverage is easy to obtain. Traders flood in with proportions far exceeding organic demand for spot. The number of people betting on ETH's rise is actually greater than those truly buying ETH.

These positions need counterparties. But the demand has become so aggressive that the shorts are increasingly taken up by mature institutional players executing Delta neutral strategies. These are not directional bears; they are funding rate harvesters, entering not to bet against ETH but to profit from structural imbalances.

In reality, this is not a traditional short-selling. These trading desks short perpetual contracts while holding equal amounts of spot or futures longs. The result is a net exposure to ETH price of zero, but they can earn from the funding rate premium paid by retail longs to maintain leverage.

With the evolution of Ethereum ETF structures, this arbitrage trade may soon be enhanced by the addition of a passive income layer (staking rewards embedded in ETF wrappers), further increasing the appeal of Delta neutral strategies.

This is truly a brilliant trading strategy, really. As long as you can handle its complexity.

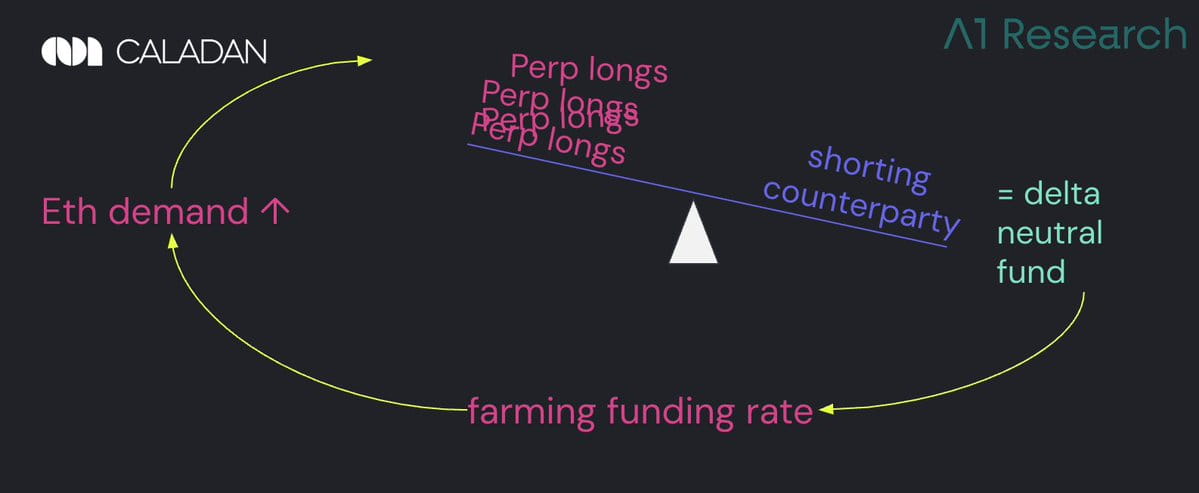

Source: @zerohedge Delta neutral strategies: How to stabilize profits.

Source: @zerohedge Delta neutral strategies: How to stabilize profits.

These trading platforms short ETH perpetual contracts to match retail demand while hedging through spot longs, profiting from the ongoing funding rate demand and capturing the spread from structural imbalances.

In a bull market, the funding rate turns positive. Bulls pay shorts. Delta neutral trading platforms earn liquidity provision rewards while hedging, forming profitable arbitrage trades that attract institutional capital.

However, this creates a dangerous illusion: the market appears to be liquid and stable, but this 'liquidity' entirely depends on a favorable funding rate environment.

The moment this incentive disappears, the foundation supporting the entire structure will also collapse. What once seemed like deep market depth will instantly turn into a vacuum, and as the supporting structure crumbles, prices are likely to experience severe volatility.

This dynamic is not limited to native cryptocurrency platforms. Even at the Chicago Mercantile Exchange (CME), which primarily involves institutional participants, the vast majority of short positions' fund flows are non-directional operations. Professional traders short CME futures because their investment mandates prohibit exposure to spot.

Options market makers hedge Delta through futures to enhance margin efficiency. Institutional trading desks hedge the order flow of corporate clients. These are structurally necessary trading strategies, rather than expressions of bearish sentiment. Open interest may increase, but rarely reflects the true market outlook.

Asymmetric risk structure: Why this is actually unfair.

Retail long positions face direct liquidation risks when prices reverse. In contrast, Delta neutral short positions are usually well-capitalized and managed by professional teams.

They use spot ETH as collateral, allowing them to short perpetual contracts under a fully hedged and margin-efficient configuration. This structure can safely withstand moderate leverage without triggering liquidations.

The difference lies in the structure. Institutional shorts possess endurance and risk management systems that can withstand market volatility. Leverage retail longs, however, have less buffer space, fewer tools, and zero tolerance for error. When market conditions change, longs will rapidly collapse while shorts hold their ground. This imbalance can trigger seemingly sudden but structurally inevitable chain liquidation effects.

Recursive feedback loop: When the market enters a self-referential state.

The demand for ETH continues to push long positions, requiring Delta neutral trading desks to fill the short counterparties, which allows the funding rate premium to persist. Protocols and yield products chase these premiums, redirecting more capital back into this cycle.

It's like a financial perpetual motion machine, except such a thing doesn't actually exist.

This creates continuous upward pressure, but it entirely depends on one condition: bulls must be willing to pay for leverage.

However, the funding rate mechanism has an upper limit. In most exchanges (such as Binance), the funding rate for perpetual contracts is capped at 0.01% every 8 hours, which annualizes to about 10.5%. Once this cap is reached, even if long demand continues to rise, the shorts chasing yield will lose their incentive to enter.

The structure has reached saturation: arbitrage rewards are fixed, but structural risks continue to rise. When this imbalance unravels, the situation is likely to reverse quickly.

Why Ethereum is more prone to declines than Bitcoin: An analysis of the two major blockchain ecosystems.

Bitcoin benefits from non-leveraged buying created by corporate treasury strategies, and the BTC derivatives market has deeper liquidity. Ethereum perpetual contracts, on the other hand, are deeply integrated with yield strategies and DeFi protocols. A large influx of ETH collateral into structured products like Ethena and Pendle rewards participation in funding rate arbitrage.

Bitcoin is often seen as being naturally driven by the spot demand of ETFs and corporations. However, a significant proportion of ETF fund flows are mechanical hedges: traditional finance basis trading desks buy ETF shares while shorting CME futures to lock in a fixed spread between spot and futures.

This is similar to Delta neutral basis trading in ETH, only executed through regulated wrapper instruments and financed at a 4-5% dollar cost. From this perspective, ETH leverage becomes an income infrastructure, while BTC leverage becomes structural arbitrage. Neither is directional trading; both are yield-seeking strategies.

Cyclic dependency issue: When the music stops.

There is one question that may keep you up at night: this dynamic essentially depends on market cycles. The profitability of Delta neutral strategies relies on a continuous positive funding rate, which requires sustained retail demand and bullish market conditions.

Funding rate premiums do not exist permanently. They are fragile. When they compress, positions will begin to close. If retail enthusiasm wanes, the funding rate will turn negative, meaning that shorts will pay longs instead of collecting a premium.

Under scaled operations, this dynamic can create multiple vulnerabilities. First, as more capital flows into Delta neutral strategies, the basis will gradually converge. Funding rates will decline, and the profitability of arbitrage trades will consequently shrink.

If market demand reverses or liquidity dries up, perpetual contracts may fall into an inverted spread state — where perpetual prices are below spot prices. This will deter new neutral strategies from entering and may force existing trading teams to close their positions. Meanwhile, leveraged longs lack margin flexibility, and even a slight pullback could trigger chain liquidations.

When the neutral trading teams exit and a wave of long liquidations breaks out, a liquidity vacuum will form — there will no longer be genuine directional buying pressure below the price, only structural absent selling pressure. The originally stable arbitrage ecosystem will suddenly fall into a chaotic liquidation storm.

Misjudging market signals: The illusion of balance.

Market participants often misinterpret hedging fund flows as bearish signals. In reality, the high levels of ETH short positions often reflect profitable basis trading rather than directional views.

The seemingly robust depth of the derivatives market is, in most cases, actually provided by neutral trading platforms offering rented liquidity, aimed at capturing funding rate premiums. While ETF fund flows do bring some degree of organic spot demand, most of the trading activity in perpetual contracts is essentially structurally manufactured.

This market depth does not stem from a belief in ETH's future; it will exist as long as funding conditions remain profitable. Once profit margins disappear, liquidity will dissipate alongside it.

Market truth

The market can rely on structural liquidity for extended periods, creating a false sense of security. But when conditions reverse and the longs can no longer bear the funding costs, liquidation actions will not be gradual but will exhibit accelerated selling. One side will be completely liquidated, while the other will simply exit the market quietly.

For market participants, identifying such patterns is both an opportunity and a warning. Professional traders can profit by understanding the funding rate situation, while retail traders should distinguish between 'artificially created' and 'truly existing' market depth.

The derivatives market of Ethereum is not driven by a genuine belief in decentralized computing, but rather by structural operations based on funding rate arbitrage. As long as the funding rate remains positive, this system can operate smoothly; but when the flow of funds reverses, the market will realize that the seemingly balanced structure is merely a façade carefully disguised by leverage.

This article, The Truth of Ethereum's Bull Market: How Leverage and Arbitrage Institutions Create the Illusion of Liquidity, first appeared in Chain News ABMedia.