Author: Sunny, Messari Research

Compiled by: Alex Liu, Foresight News

In recent years, traditional finance (TradFi) has gradually lost the source of growth narratives. Artificial intelligence has been overallocated, and software companies are no longer as full of imaginative potential as they were in the 2000s and 2010s.

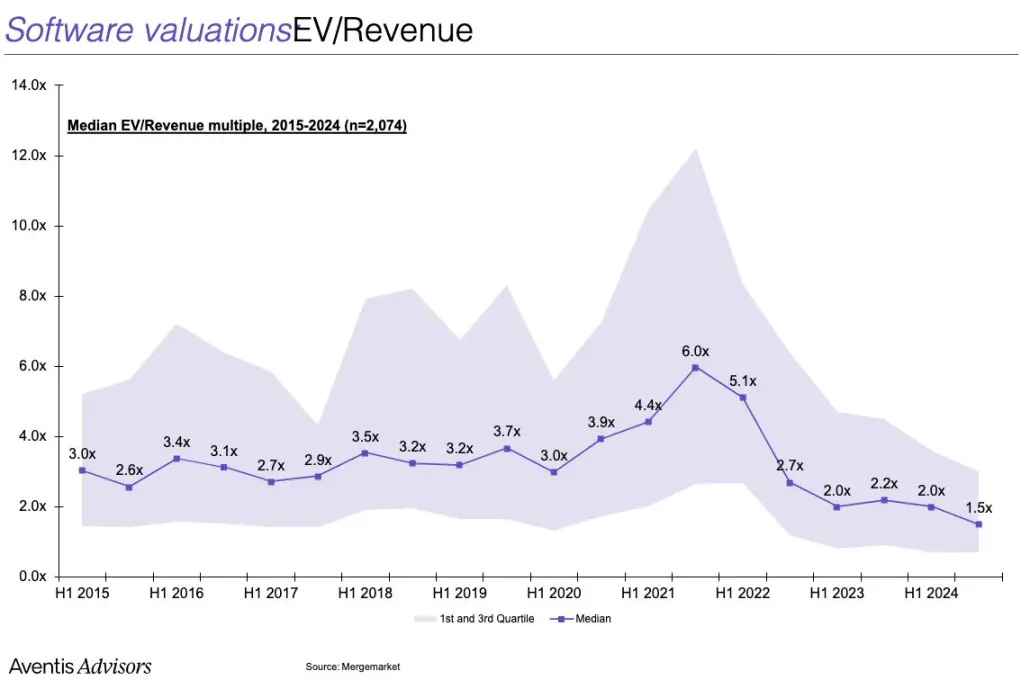

For growth investors who raise funds to bet on disruptive innovation narratives, the reality is: AI asset valuations are generally inflated, and other 'growth stories' are hard to tell anew. The once-prominent FAANG stocks are gradually transforming into moderate 'compound growth stocks' that pursue profit maximization. The median sales multiple (enterprise value/sales) of current software companies has fallen below 2 times.

Thus, cryptocurrencies have once again stepped into the spotlight.

Bitcoin has broken its historical high; the U.S. President has 'strongly advocated' for crypto assets at a press conference; a series of regulatory tailwinds have brought this asset class back into the mainstream spotlight for the first time since 2021.

Unlike the last cycle's NFTs and Dogecoin, the main characters in this cycle are digital gold, stablecoins, 'tokenization', and payment system reform. Stripe and Robinhood claim that the next focus is on cryptocurrency business; Coinbase has successfully entered the S&P 500 index; Circle has presented a sufficiently compelling growth narrative to capital markets, causing investors to ignore valuation multiples and focus on potential stories.

But what does all this have to do with ETH?

For crypto natives, the battle for smart contract platforms has long been divided: Solana, Hyperliquid, and countless high-performance new chains and Rollup platforms pose a real threat to Ethereum's dominance.

We know that Ethereum has not yet truly solved the value capture problem, and we also know that it is facing structural challenges.

But Wall Street is not aware of this. In fact, most practitioners on Wall Street know almost nothing about Solana. In terms of recognition, older coins like XRP, LTC, LINK, ADA, DOGE may hold more presence in their minds than SOL. After all, these people have almost completely faded out of the crypto market in recent years.

What they know is that ETH is 'lindy' - it has withstood the test of time; it has been tested through multiple market fluctuations; for a long time, it has been the main 'Beta' asset besides Bitcoin. What they see is that ETH is currently one of only two crypto assets with a spot ETF. What they prefer is a relatively cheap asset with an upcoming catalyst, a 'value pit'.

In their eyes, Coinbase, Kraken, and Robinhood all choose to build products on Ethereum. With a bit of due diligence, they can see that Ethereum has the largest on-chain stablecoin pool. They start doing 'moon math' - and then realize Bitcoin has hit a new high, while Ethereum is still over 30% away from its 2021 peak.

For them, this 'relative undervaluation' is not a risk, but an opportunity. They prefer to buy an asset that is still at a low point and has a clear target price, rather than chasing a currency that is 'too late' on the chart.

And they may have already entered the market. Now, the compliance restrictions on institutional investment are no longer a major issue. As long as there is enough incentive, any fund can strive to allocate crypto assets. Despite cryptocurrency Twitter (CT) swearing for the past year that they would 'never touch ETH again', from this year's market performance, ETH has outperformed other mainstream assets for more than a month straight.

As of now, SOL/ETH has fallen nearly 9% this year; after hitting a bottom in May, Ethereum's market cap ratio has begun the longest rise since mid-2023.

So the question arises: if the entire crypto community believes ETH is a 'cursed coin', how can it still outperform?

The answer is: it is attracting new buyers.

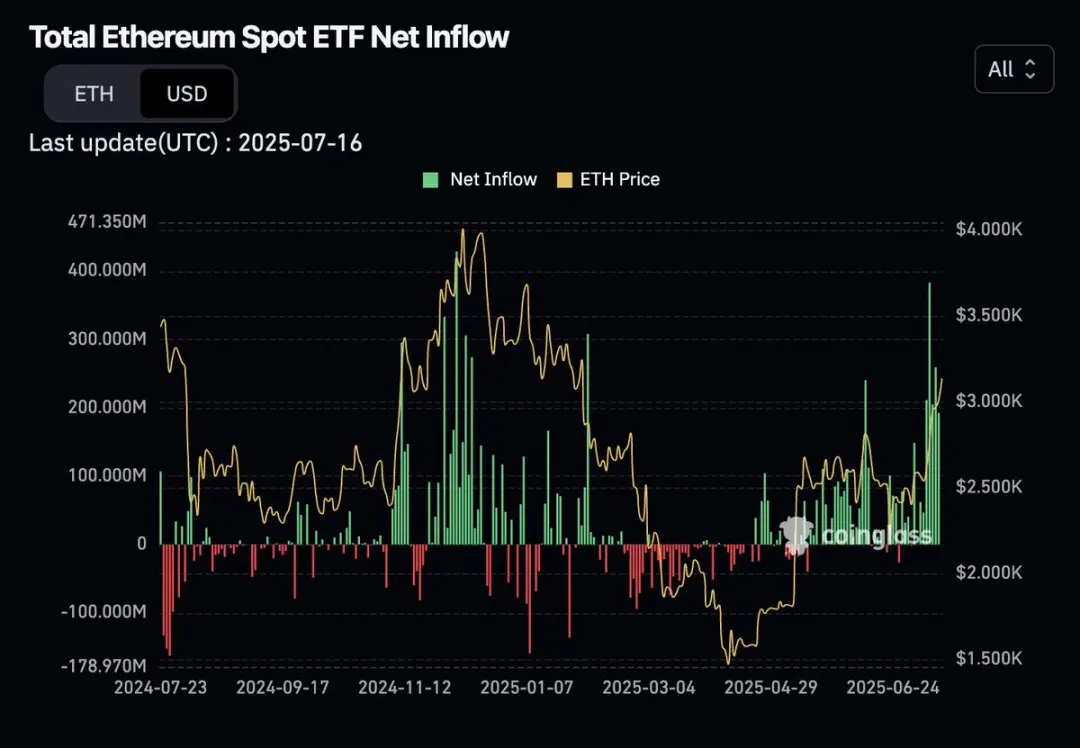

Since March, the net inflow data for Ethereum's spot ETF has been in an 'up only' mode, rising without falling.

Ethereum 'accumulators' mimicking the MicroStrategy model are taking off, injecting structural leverage into the market.

At the same time, some crypto-native users may realize that their allocations are insufficient and start to transfer funds from BTC and SOL, which have already surged over the past two years.

It should be clear that we are not saying that the Ethereum ecosystem has solved its problems. Rather, the asset ETH is beginning to gradually 'detach' from the Ethereum network.

External buyers are reshaping the market narrative for ETH, shifting from 'decline is certain' to a paradigm of 'valuation reassessment'. Shorts will eventually be squeezed, and at that point, native funds may also join the rally, leading us to a market frenzy centered around ETH, which will peak at some point.

If this situation occurs, a new historical high for ETH may not be far away.