1. Introduction.

This week, the crypto market welcomed two heavyweight catalysts—the legislative push of Washington's 'Cryptocurrency Week' and the intensive deployment of Ethereum by institutions, together forming the 'policy turning point' and 'capital turning point' for the crypto industry in the second half of 2025. The deep logic of this round of crypto cycles is shifting from Bitcoin to Ethereum, stablecoins, and on-chain financial infrastructure. We believe that the clarification of U.S. policies and the institutional expansion of Ethereum signify that the crypto industry is entering a structurally positive phase, and the focus of market allocation should gradually shift from 'price games' to 'rules + infrastructure institutional dividend capture.'

2. U.S. 'Cryptocurrency Week': Three major bills release signals, compliant assets will welcome value reassessment.

In July 2025, the U.S. Congress officially launched 'Cryptocurrency Week,' marking the first time in U.S. history that a legislative agenda systematically promotes comprehensive governance of crypto assets. Against the backdrop of dramatic changes in the global digital financial landscape and constant challenges to traditional regulatory models, the introduction of this series of bills is not only a response to market risks but also a signal of the U.S. attempting to seize a leading position in the next round of financial infrastructure competition.

The most milestone significance is the (GENIUS Act), which establishes a complete regulatory framework for stablecoins, covering key elements such as custody requirements, audit disclosures, asset reserves, and clearing processes. This means that the stablecoin system, which has long operated outside traditional financial regulation and relied on 'market trust,' will first be incorporated into the U.S. sovereign legal structure. The Senate's overwhelming passage (68 votes in favor, 30 against) also demonstrates the strong bipartisan support for this bill, which can be seen as an institutional 'calming pill' for the entire crypto industry. Once the House passes and sends it to the President for signature, this bill will officially take effect, marking the U.S. as the first major economy to establish a unified financial regulatory framework for stablecoins.

Another key bill (the CLARITY Act) focuses on the classification of crypto assets as securities or commodities. Its core intention is to clarify 'which crypto assets belong to securities and which do not' and to delineate the regulatory boundaries between the SEC and CFTC. The controversy over whether ETH, SOL, and other tokens should be classified as securities has led to a significant number of companies and projects migrating out of the U.S. market. If this bill passes smoothly, it will end the long-standing unresolved state of the 'regulatory gray area' for crypto assets, providing predictable legal basis for project parties, exchanges, and fund managers, greatly releasing the vitality of compliant innovation.

More politically symbolically significant is the (anti-CBDC surveillance state act). This bill prohibits the Federal Reserve from issuing a central bank digital currency (CBDC), preventing the government from establishing real-time surveillance capabilities over personal financial activities through a digital dollar framework. Although this bill has not yet been passed by the Senate, it reflects the U.S. Congress's emphasis on financial privacy and market freedom. It effectively sends another signal: the U.S. does not intend to dominate the digital financial transformation through state monopoly, but rather to support a crypto asset ecosystem driven by the market, technology-neutral, and open and interconnected.

In summary, these three major bills point in the same direction of 'regulation-driven innovation' and emphasize 'clear boundaries and reduced uncertainty' as their means. Their core demand is no longer 'restriction' but 'guidance.' Once the legislation enters the implementation stage, it is expected to bring several direct consequences: first, the barriers preventing institutional investors from entering on a large scale due to compliance risk concerns will gradually be lifted, allowing pension funds, sovereign wealth funds, and insurance companies to legally deploy crypto positions; second, the role of stablecoins as 'on-chain dollars' will be confirmed by policy, exponentially amplifying their efficiency in scenarios like cross-border settlement, decentralized finance, and RWA; third, compliant exchanges and custody banks will receive policy backing, reshaping the trust structure of the global crypto market.

On a deeper level, this series of legislations is a strategic response to the new round of reshaping of financial order in the U.S. Just as the dollar became the global settlement currency relying on the Bretton Woods system after World War II, stablecoins are becoming the vehicle for the digital expansion of dollar influence, and the U.S. Congress is attempting to inject institutional legitimacy into them through regulatory means. This is a game of financial geopolitical power layout, as well as a direct response to China's central bank digital currency (e-CNY) and the EU's MiCA regulatory framework. Whoever first completes the construction of a regulatory system will set the standards and hold the discourse power in the future global financial network.

Therefore, 'Cryptocurrency Week' is not only a moment for the market to reassess the valuation logic of crypto assets but also a systematic confirmation of the policy towards technological trends. This institutional pricing signal will inject more stable expectation anchors into the market, while also providing investors with pathways to identify 'regulatable and sustainable' assets. We believe this rule certainty will gradually transform into valuation certainty, and compliant assets, especially stablecoins, ETH, and their surrounding infrastructure, will become the core beneficiaries of the next round of structural reassessment.

3. ETH institutional arms race: ETF entry, staking mechanism transformation, and asset structure upgrade advancing on three fronts.

Recently, with ETH's strong rebound, market confidence is gradually being restored, and behind this is a new 'capital arms race' around Ethereum quietly unfolding. From Wall Street financial giants continuously increasing their positions through ETF channels to more and more publicly listed companies adding ETH to their balance sheets, Ethereum is undergoing a profound restructuring of its market structure. This not only signifies that traditional capital's recognition of ETH has entered a new phase but also marks Ethereum's accelerated evolution from a highly volatile, high technical barrier decentralized asset to a mainstream financial asset with institutional-level allocation logic.

Since the launch of the Ethereum spot ETF in July 2024, it was once viewed as a significant catalyst for ETH price breakthroughs, but the actual performance disappointed the market for a time. Negative factors such as the ETH/BTC exchange rate dipping, sluggish prices, and continuous sell-offs by the foundation meant that ETH did not immediately unleash upward momentum after the ETF listing, but instead fell into a deep correction. Especially in the context of the Bitcoin ETF's great success, ETH appeared rather forlorn.

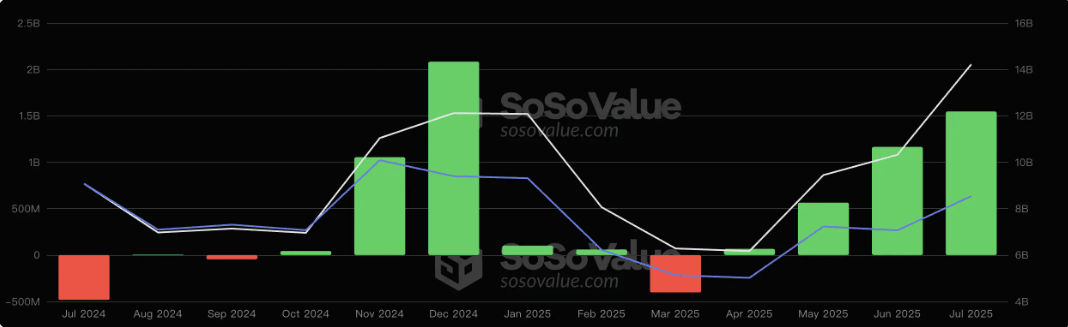

However, by mid-2025, this situation began to quietly reverse. From on-chain data and ETF capital inflows, the institutional accumulation process for ETH is proceeding quietly yet firmly. According to SoSoValue statistics, since the launch of the ETF, the Ethereum spot ETF has attracted a cumulative net inflow of $5.76 billion, accounting for nearly 4% of its market capitalization. Although the price once retreated, the capital inflow has remained stable, indicating long-term institutional funds' recognition of ETH's allocation value. This trend has started to accelerate in the last two months, with several Ethereum ETF products recording monthly net inflows exceeding $1 billion, and traditional financial players like Bitwise, ARK, and BlackRock significantly increasing their holdings.

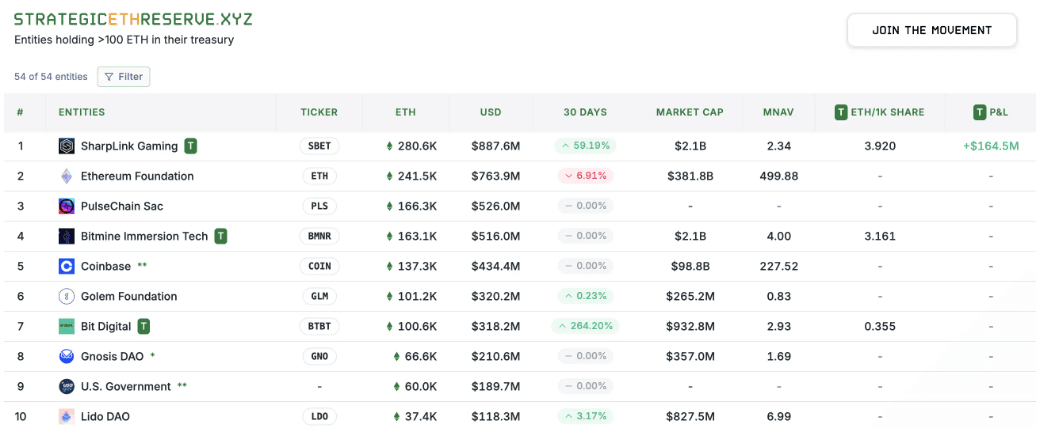

At the same time, a more symbolic change comes from the rise of publicly listed companies' 'strategic reserves of Ethereum.' Companies such as SharpLink Gaming, Siebert Financial, Bit Digital, and BitMine have announced that they will add ETH to their balance sheets, marking a turning point for ETH from being a 'speculative asset' to a 'strategic reserve asset.' Notably, SharpLink currently holds over 280,000 ETH, surpassing the Ethereum Foundation’s current 242,500 ETH, becoming the world's largest single institutional holder of ETH. This fact has, in some ways, already completed a partial transfer of 'discourse power' at the symbolic level.

From the current structure of institutional participation, it can be clearly divided into two camps: one is the 'Ethereum native camp' represented by SharpLink, gathering early Ethereum ecosystem participants such as ConsenSys and Electric Capital; the other is the 'Wall Street approach' represented by BitMine, which directly replicates the Bitcoin reserve logic, using leverage, financial operations, and financial report disclosures to create capital amplification effects. This north-south encirclement type of institutional building model is causing ETH's value anchor and price support system to move away from traditional retail speculative emotions towards an institutionalized, long-term, structured mainstream capital framework.

The far-reaching impact of this trend lies not only in price but also in the potential reconstruction of the governance rights, discourse power, and ecological dominance of the Ethereum network itself. In the future, if companies like SharpLink or BitMine, which are heavily invested in ETH, continue to expand their holdings, their potential influence on Ethereum's development direction will be significant. Although these companies currently face financial pressures and are accumulating ETH more out of speculative hedging and capital operations rather than demonstrating a deep commitment to Ethereum's ecosystem, their entry has already created a magnifying effect in the capital market: ETH is being revalued, and the market narrative is shifting from the crowded tracks of DeFi and L2 to a new space of 'reserve assets + ETF + governance rights.'

It is worth noting that, unlike the Bitcoin reserve story with Michael Saylor (CEO of MicroStrategy) as a 'spiritual leader' continuously reinforcing cognition and advocating for accumulation, Ethereum has yet to have a representative figure with both a faith background and traditional capital appeal. The emergence of figures like Tom Lee has sparked market associations, but has not formed sufficient narrative penetration. The lack of endorsement from such figures has also somewhat slowed down the path of trust transformation for Ethereum among institutional investors.

However, this does not mean that Ethereum lacks responses at the institutional level. Vitalik Buterin and the Ethereum Foundation have recently been vocal, emphasizing Ethereum's technical resilience, security mechanisms, and decentralization principles, while also beginning to strengthen the 'dual-track' governance mechanism in the ecosystem, aiming to embrace institutional capital while avoiding governance power being controlled by a single force. In a recent public article, Vitalik proposed that the interests of users, developer-led initiatives, and institutional compliance must be balanced, and decentralization must possess 'operability' rather than merely existing as a slogan.

In summary, ETH is undergoing a comprehensive change in its capital structure: moving from a retail-dominated open market to an institutionalized market structure driven by ETFs, publicly listed companies, and institutional nodes. The impact of this transition will be profound, as it will not only determine the future construction path of ETH's price center but may also reshape the governance structure and development rhythm of the Ethereum ecosystem. In this arms race, ETH is no longer just a representation of the technology stack, but is becoming a key target in the wave of digital capitalism, serving both as a value-bearing tool and a focal point of power struggles.

4. Market Strategy: BTC builds a high-level platform, while ETH and mid-to-high quality application chains welcome the catch-up logic.

As Bitcoin successfully broke through the $120,000 mark and gradually entered a platform phase, the structural rotation pattern of the crypto market has become clearer. Under the dominant logic of BTC, Ethereum and high-quality application chain assets are beginning to welcome their own valuation repair period. From capital flows to market performance, the current market shows a typical structure of 'large-cap platform oscillation + mid-cap rotation attack,' with ETH and a batch of L1/L2 protocols that combine narrative and technical support becoming the most valuable direction for speculation after Bitcoin.

1. BTC enters the high-level platform construction phase: supported downwards, but lacks strength upwards.

Bitcoin, as the main driving asset of this round of market, has basically completed the main upward wave driven by the spot ETF, halving cycle, and institutional reserves. The current trend has entered a sideways consolidation phase, and although it is still within the technical upward channel, the upward momentum is weakening in the short term. From on-chain data, both the number of active BTC addresses and the transaction volume have seen a certain degree of decline, while implied volatility in the options market continues to decline, indicating that market expectations for a short-term breakthrough are decreasing.

At the same time, traditional institutions' enthusiasm for allocation has not significantly diminished. According to the latest report from CoinShares, BTC ETF still maintains a slight net inflow, indicating that bottom support remains, but as expectations have been largely fulfilled, the subsequent upward pace of BTC is likely to slow down or even enter a phase of horizontal consolidation. For institutions, Bitcoin has entered a 'core allocation' phase, rather than continuing to chase short-term profits.

This also means that market attention is gradually shifting from Bitcoin to other growth-oriented crypto assets.

2. ETH's catch-up logic forms: From 'lost leader' to 'value undervaluation' reassessment.

Compared to Bitcoin, Ethereum's performance since the second half of 2024 has been seen as 'disappointing,' with its price having a large correction and its ratio to BTC dropping to a three-year low. However, it is precisely during this low phase that ETH has gradually completed the revaluation and optimization of its holding structure. Currently, institutional recognition of ETH is rapidly increasing, with not only continuous net inflows into the spot ETF but also a trend of publicly listed companies reserving ETH, even surpassing the foundation's holdings.

From a technical perspective, ETH's price has broken through the previous downtrend line, began establishing an upward channel, and has consecutively reclaimed several key technical moving averages. Combined with capital and sentiment indicators, ETH has entered a new cycle of market sentiment switching. During BTC's consolidation period, the cost-effectiveness of ETH as a secondary mainstream asset is gradually rising, complemented by the expansion of the L2 ecosystem, stable staking rewards, and enhanced security, the market is re-evaluating its long-term value foundation.

From an asset allocation perspective, ETH not only possesses 'valuation undervaluation' advantages at this stage, but it also begins to have similar institutional recognition and narrative completeness as BTC, combining both technological and institutional advantages, making it the preferred catch-up target under capital rotation.

3. The rise of high-quality application chains: Solana, TON, Tanssi, and other chains are welcoming structural opportunities.

Beyond BTC and ETH, the market is accelerating its shift towards mid-to-high-quality application chain assets that have 'real narrative support.' Chains like Solana, TON, Tanssi, and Sui, with their multiple advantages of 'high performance + strong ecosystem + clear positioning,' have quickly attracted concentrated capital in this round of rebound.

Taking Solana as an example, the current ecosystem activity has significantly rebounded, with multiple on-chain applications returning to users' views, and emerging narratives like DePIN, AI, and SocialFi are gradually taking root within the Solana ecosystem. Tanssi, as an emerging infrastructure protocol in the Polkadot ecosystem, is gaining widespread attention from institutions and developers by solving long-standing issues such as 'complex application chain deployment, high operating costs, and fragmented infrastructure' with its ContainerChain model. Its collaboration with platforms like Huobi HTX also indicates an acceleration in its marketization process.

In addition, as Ethereum shifts towards a more modular and data-availability-optimized path, intermediate layer protocols (such as EigenLayer and Celestia) and L2 Rollup solutions (such as Base and ZkSync) are gradually releasing value, becoming an important 'valuation center' between public chains and application layers. These protocols or platforms combine scalability, security, and innovation, becoming new frontiers for concentrated capital breakthroughs.

4. Market strategy outlook: Focus on 'value rotation' and 'narrative advance.'

Overall, the capital rotation logic of this round of the crypto market has become clear: BTC peaks—ETH catches up—application chains rotate. The strategic focus for this stage should revolve around the following points:

(1) BTC positioning for retention, not a primary offensive direction: core holdings remain unchanged, but it is not advisable to chase higher prices, and potential policy or macro disturbance risks should be monitored.

(2) ETH as a core rotation configuration target: Technical recovery + strengthened institutional narrative, suitable for mid-term configuration, and if ETF funds accelerate inflows, there may be further upward space.

(3) Focus on mid-to-high quality public chains and modular protocols: Chains with technological innovation, strong ecological foundations, and capital supporters (such as SOL, TON, Tanssi, Base, Celestia) have sustainable upward potential.

Advance the narrative, proactively seek new opportunities at the margins: Focus on early layout targets in DePIN, RWA, AI chains, ZK directions, these narratives are in the capital pre-positioning stage and may become the core of the next phase of rotation.

The final conclusion is that the current market has shifted from a single asset-driven phase to a structural rotation phase, with BTC's main upward wave pausing and the rotation of ETH and high-quality new public chains becoming the key driving force of the second half of the market. Strategically, one should abandon the habitual thinking of 'chasing high leaders' and shift towards a mid-term trend layout of 'valuation rebalancing + narrative diffusion.'

5. Conclusion: Regulatory clarity + ETH main ascent, the market enters an institutional cycle.

With the advancement of the three key bills during the U.S. 'Cryptocurrency Week,' the industry has welcomed an unprecedented period of policy clarity. This clarity in the regulatory environment not only eliminates the compliance uncertainties that have lingered for many years but also lays a solid foundation for the institutional and formal development of the crypto asset market. Alongside the acceleration of the strategic reserve arms race for core assets like Ethereum, the market is gradually entering a new cycle dominated by institutions.

In the past, the volatility and uncertainty of the crypto market were largely due to regulatory ambiguity and policy fluctuations. Crises such as the collapse of FTX and the Luna incident exposed deep risks due to the lack of industry regulation and planted shadows in the minds of investors. Now, with the implementation of regulations such as the (GENIUS Act), (CLARITY Act), and the anti-CBDC act, market expectations for compliance have significantly risen, the entry barriers for institutional capital have been steadily lowered, and the trust and liquidity of assets have been greatly enhanced. This not only helps to reduce systemic risks but also provides a 'bridge' for crypto assets to connect with traditional financial markets, achieving the legalization and standardization of market participants' identities and behaviors.

In this catalyzing institutional environment, Ethereum, as the leader of smart contract platforms, is entering a key window for its main upward wave. Ethereum not only has a clear technical roadmap and active ecological innovation, but its network security and decentralized governance structure are continuously optimized, making it one of the preferred digital assets for institutions. The combined push from strategic reserve trends and ETF funds signifies that Ethereum's value is beginning to receive a new assessment from the capital market. It is foreseeable that Ethereum will maintain a long-term healthy value growth trend under the dual drives of on-chain application growth and capital support.

More broadly, this linkage effect of clear regulation and the revival of mainstream asset values is prompting the crypto market to gradually break away from the previous 'bull-bear cycle trap,' evolving towards a more stable and sustainable institutional cycle. A significant characteristic of the institutional cycle is that market fluctuations are more guided by fundamentals and policy expectations, with asset price fluctuations no longer dominated by scattered emotions and regulatory news, but rather reflected as a benign interaction and steady growth between capital and technology. The deep involvement of institutional capital will also promote the improvement of market liquidity structure, shifting investment strategies from short-term speculation to medium- to long-term value investing.

In addition, the opening of the institutional cycle also signifies the diversification of market structure and the multidimensional upgrade of ecosystems. The technical innovations and governance reforms of the Ethereum ecosystem will continuously promote the diversification of on-chain applications, enhancing network utility, while regulatory clarity will accelerate the compliant development of more quality projects, fostering a deep integration of on-chain finance and traditional finance. This development pattern will reshape the investment logic of crypto assets, moving the market into a new norm of 'technology-driven + capital rationality + regulatory support.'

Of course, the institutional cycle does not mean that market volatility disappears, but that fluctuations will be more endogenous and predictable, requiring investors to pay more attention to the continuous tracking of fundamentals and policies. At the same time, the interplay between market governance mechanisms, decentralization, and centralized forces will also become important variables pushing ecological evolution.

In conclusion, the regulatory breakthroughs during the U.S. 'Cryptocurrency Week' and the capital trend of Ethereum's main ascent are opening an important chapter for the crypto market's maturity. The market is transitioning from the chaotic and disorderly phase of 'barbaric growth' to the institutionalized and standardized phase of 'rational development.' This not only enhances the investment value of assets but also promotes the overall upgrade of the crypto industry ecosystem, shaping the core foundation of the future digital economy. Investors should seize the opportunities of institutional dividends and the growth of core assets, actively laying out positions in Ethereum and quality application chains, embracing a healthier and more sustainable new era of crypto.