The past and present of PayFi, redefining Web3 payments.

Since the internet's inception, it has evolved from the 'read-only' era of Web1.0 to the 'read + write' interactive era of Web2.0, gradually moving towards Web3.0, a new era based on blockchain technology, user-centered, decentralized, and achieving value self-ownership. This evolution is not only a technical iteration but also a profound transformation of network philosophy, value distribution, and user rights. In this grand narrative, payments—the foundational function sustaining economic activity—are also undergoing a 'redefinition' driven by underlying technology and ideology.

1. The evolution of PayFi: An inevitable progression of value interconnection.

The traditional payment system is rooted in centralized trust models. Banks, credit card companies, and other intermediaries act as 'gatekeepers' of value flow. This model significantly promoted commercial circulation during specific historical periods but also exposed many inherent pain points: high transaction costs, especially cumbersome processes and layered fees in cross-border payments; slow settlement speeds, which may take several days for international remittances; lack of transparency, with users lacking clear control over the fund flow process; and a high dependence on infrastructure, leaving billions of people globally unable to access basic financial services. The dominant position of Web2 platforms has also brought about centralized control over user data and content, as well as potential censorship and abuse of power issues.

Bitcoin, as the first widely recognized cryptocurrency, defined itself in its white paper as a peer-to-peer (P2P) electronic cash system designed to enable online payments without third-party intervention. This marked the emergence of the concept of decentralized payments. However, Bitcoin's extreme value volatility severely limits its potential as a medium for daily transactions.

Subsequently, the emergence of stablecoins greatly alleviated the price volatility issues of crypto assets, making them one of the main payment methods in the blockchain field. Stablecoins like USDC and USDT play the role of 'on-chain dollars' on the blockchain, widely used in payment, trading, and DeFi scenarios, becoming important tools in the digital economy.

It is against this backdrop that the concept of PayFi (Payment Finance) emerged. Lily Liu from the Solana Foundation is considered the proposer of the PayFi concept, defining it as 'the process of creating new financial markets around the time value of funds.' PayFi is not an entirely independent concept but integrates innovative applications of Web3 crypto payments, decentralized finance (DeFi), and real-world assets (RWA). It aims to leverage blockchain technology to innovate payment systems, achieving more efficient and lower-cost transactions while combining financial services with payment functions to provide new financial experiences and application scenarios.

The evolutionary trajectory of PayFi clearly reflects the development path of Web3 payments from theory to practice, from a single function to an integrated ecosystem. It starts from Bitcoin's vision of peer-to-peer payment, using stablecoins to address value volatility issues, further absorbing the advantages of DeFi in liquidity, programmability, and yield generation, while integrating RWA to bring real-world assets on-chain. The core objective of PayFi is to promote the application of digital assets in real-world scenarios and to enhance financial transaction efficiency by unlocking the time value of funds (TVM). It is not merely simple payments but integrates payments, financing, investment, and other financial activities into a unified decentralized framework.

From a technical architecture perspective, PayFi is generally understood to contain multiple layers: a settlement layer based on high-performance blockchains (such as Solana, Stellar, or Layer2 solutions); an asset issuance layer responsible for issuing payment mediums (stablecoins, etc.); a currency acceptance layer connecting fiat and crypto assets; and a front-end application layer aimed at users. Additionally, there is a supporting layer responsible for custodial, compliance, and financing functions. This layered architecture provides a technological foundation for the robust development of PayFi.

2. Web3 VS Web2: Reshaping power and value.

The core difference between Web2 payments and Web3 payments lies in the fundamental differences in underlying trust mechanisms and value transfer methods. This is not just a technical detail but also a redefinition of user rights and system architecture.

The deeper logic is that Web3 payments build a network of 'machine trust' through blockchain technology. Transaction rules are written into smart contracts and executed automatically, rather than relying on manual processes. Users' identities (via DID) and assets (via tokens) truly belong to the users, stored on the users' blockchain addresses rather than being hosted on centralized platforms. This model fundamentally challenges the data and value distribution monopoly of Web2 platforms, granting users greater autonomy and value capture ability.

Based on this, PayFi takes the programmability of Web3 payments and the deep integration with DeFi/RWA to the extreme. It is not only a tool for achieving low-cost and fast transfers but also an ecosystem capable of providing real-time financing, yield generation, and asset management services built on payment processes. This integration transforms 'payments' from an isolated link into a bridge connecting real-world assets and on-chain financial services, unlocking the time value of funds. This marks a paradigm shift in payments from simple bookkeeping and settlement functions to value transfer infrastructure with rich financial attributes.

3. Major companies' layouts: Entry of giants and paradigm confirmation.

Web3 payments, particularly the blueprint of 'payments as finance' depicted by PayFi, have immense transformative potential, attracting the attention of various giants. This includes not only the deepening expansion of crypto-native forces but also the noteworthy entry of traditional payment, finance, and internet tech giants. Their involvement is not only a strong endorsement of the value of the Web3 payment arena but also signals that this field is accelerating from early exploration to mainstream application.

Traditional payment and financial giants' 'defense and evolution'.

Visa & Mastercard: These two credit card giants are not sitting idly by. They have already begun experimenting with the use of stablecoins (like USDC) for settlements and exploring how to connect their vast global merchant networks with blockchain payments. For example, Visa has partnered with several crypto platforms to issue cards that support cryptocurrency spending and test USDC settlements on its network, significantly reducing the complexity and cost of cross-border transactions. This is a typical strategy of 'embracing innovation to avoid being disrupted.'

PayPal: As a pioneer in online payments, PayPal launched its own stablecoin, PYUSD, and allows users to buy, sell, hold, and transfer specific cryptocurrencies on its platform, even for payments at some merchants. This marks its strategic extension from the Web2 payment domain into the Web3 realm, attempting to integrate the advantages of crypto payments into its existing ecosystem within the user experience and compliance framework.

SWIFT: Even as the core of traditional international interbank communication and payment instructions, SWIFT is actively exploring the interoperability of central bank digital currencies (CBDCs) and tokenized assets, trying to find its position in the new financial infrastructure.

Internet technology giants' 'cross-industry and empowerment'.

China's internet giants: Against the backdrop of a settled domestic payment market, cross-border e-commerce and overseas business have become new growth points. The pain points of traditional cross-border payments—high costs, slow speeds, and exchange rate risks—are particularly prominent for them. Therefore, leveraging policy windows in places like Hong Kong to explore using stablecoins and other Web3 payment tools to optimize international capital settlements has become a strategic choice. JD.com, through its Hong Kong subsidiary, is precisely looking at the disruptive potential of stablecoins in improving cross-border payment efficiency and reducing operational costs, attempting to 'overtake' in the overseas payment arena.

Overseas tech giants: Meta (formerly Facebook) ambitiously pushed the Diem (originally Libra) stablecoin project, aiming to build a global, low-cost payment network, especially targeting unbanked populations. Although it was thwarted by regulatory pressures, its attempts profoundly revealed the desire of tech giants with vast user bases and social scenarios to enter the payment and even financial sectors, as well as the potential of Web3 technology in realizing this vision.

The 'ecological closed loop' of crypto-native exchanges.

Coinbase & OKX, etc.: These large centralized exchanges naturally possess users, assets, and trading scenarios. They actively layout payment operations, such as Coinbase Commerce providing cryptocurrency collection services for merchants, and OKX launching OKX Pay. Their logic is to build a complete ecological closed loop from deposit, trading, storage, to payment consumption by integrating fiat deposit and withdrawal channels, stablecoins, custodial wallets, and payment solutions. Acquiring payment licenses serves both the compliance of trading operations and lays the foundation for the expansion of their payment businesses.

4. Deep insights from major players' strategies: From 'testing the waters' to 'strategic positioning'.

Actions of major companies are far from simply 'riding the wave'. They see the strategic value contained in Web3 payments, particularly in the PayFi concept.

Efficiency revolution: The near real-time and low-cost characteristics of blockchain payments pose a dimensionality reduction attack on existing payment systems.

New financial paradigm: The combination of payment with DeFi and RWA opens up tremendous space for innovation in financial services, such as instant settlement, programmatic financing, and automated market making.

User sovereignty trend: Although some giants still adopt centralized or semi-centralized models, the idea promoted by Web3 of returning user data and asset ownership is an irreversible trend. They must consider how to adapt to this trend.

Globalization accelerator: For enterprises with international ambitions, Web3 payments offer a way to bypass traditional complex financial intermediaries, enabling more efficient global capital flow.

The explorations and investments of these giants not only bring funds, technology, and users to Web3 payments, but more importantly, they are educating the market through practical applications, promoting the maturation of regulatory frameworks, and accelerating the transition of Web3 payments from 'niche geek tools' to 'mainstream infrastructure'. Every action they take in the PayFi arena contributes to the eventual realization of this payment revolution, collectively validating the immense potential of Web3 payments to reshape the global financial landscape.

The product structure of OKX Pay: old wine in a new bottle.

"The industry's first true implementation of the fusion of non-custodial and compliance in a payment application," this is how OKX founder Star Xu positions OKX Pay, providing decentralized payment paths through centralized exchange ecosystems. Users can enjoy the convenience of the OKX platform account system while also completing on-chain payments through non-custodial wallets, creating a hybrid experience of 'self-management + platform endorsement'. Let's break down the underlying logic of the product.

1. Multisig + ZK Email + AA: The 'security + usability' combination behind OKX Pay.

The multisignature mechanism (Multisig), standardized in the Bitcoin protocol since 2012, is one of the mainstream non-custodial asset security strategies. It reduces the systemic risk of losing or stealing a single private key by splitting transaction authorization among multiple signature holders (i.e., multiple private keys or recovery permission setters). In simple terms, an account can be jointly controlled by multiple people, and assets can only be utilized when everyone 'signs off'. OKX Pay uses a dual-signature method, one being the user's Passkey signature, and the other provided by OKX as the 'account guardian'.

Passkey signatures build upon asymmetric cryptography and incorporate device and biometric recognition to help users use on-chain services without mnemonic phrases, providing a very user-friendly experience. Meanwhile, OKX signatures integrate ZK Email and Account Abstraction (AA) into the product architecture to enhance identity privacy and transaction flexibility, aiming to solve issues of high user entry barriers, difficult key management, and fragmented payment experiences.

ZK Email (Zero-Knowledge Email): By utilizing zero-knowledge proof mechanisms, it realizes the encryption and privacy protection of user identity verification information, allowing users to perform on-chain identity operations without exposing specific email addresses, making it one of the friendlier entry mechanisms in the Web3 world. It simplifies the management of access permissions for on-chain identities and lowers the bar for traditional mnemonic phrases. In simple terms, by using encrypted email, friends can input your email to send you money. You receive an encrypted email and just click to complete the payment. Technical details like wallet addresses and private keys are all handled automatically in the background, eliminating worries about misdirecting transfer wallet addresses.

Account Abstraction (AA): By 'abstracting' the Ethereum account model, it allows wallets to implement smart contract-controlled permissions, customize transaction logic, and multi-factor authentication, greatly enhancing the flexibility and programmability of transactions, and users do not need to directly sign complex transaction data. In simple terms, it makes 'wallets become customizable smart accounts'.

In summary: ZK Email allows you to use your wallet as simply as an email, and AA makes your wallet as smart and secure as an app. OKX Pay packages all these to make on-chain payments truly suitable for ordinary people.

2. Compliance integration: Finding balance between on-chain payments and regulation.

Although OKX Pay uses self-custodial wallets and on-chain settlement, it still incorporates embedded compliance designs in critical areas such as user access, transaction analysis, and merchant reviews, including mechanisms like real-name authentication (KYC) and anti-money laundering (AML). This may seem contradictory, but in essence, OKX Pay adopts a 'connectable and regulatory' strategy: the platform does not directly control user assets but can impose restrictions on high-risk behaviors within the ecosystem through means such as 'service entry', 'ecosystem access', 'account binding', and 'limit management'.

Specifically manifested as:

User identification through OKX login or account binding effectively still builds centralized user profiles.

High-frequency transfers, merchant collections, community creation, etc., require identity binding or risk control review.

The platform retains the ability to 'block entry' for malicious addresses, sensitive regions, and payments for illegal goods.

Although capital flows are on-chain, the platform can still suspend support for aggregators and recommendation pages.

This mechanism is known as 'platform-level compliance constraints', which completes certain regulatory functions based on ecosystem entry and API permissions, without utilizing user private keys. It represents a realistic intermediate form—a fusion model of 'Web2 legal logic + Web3 technical architecture'. Truly decentralized products with centralized compliance management.

SocialFi disguised as PayFi.

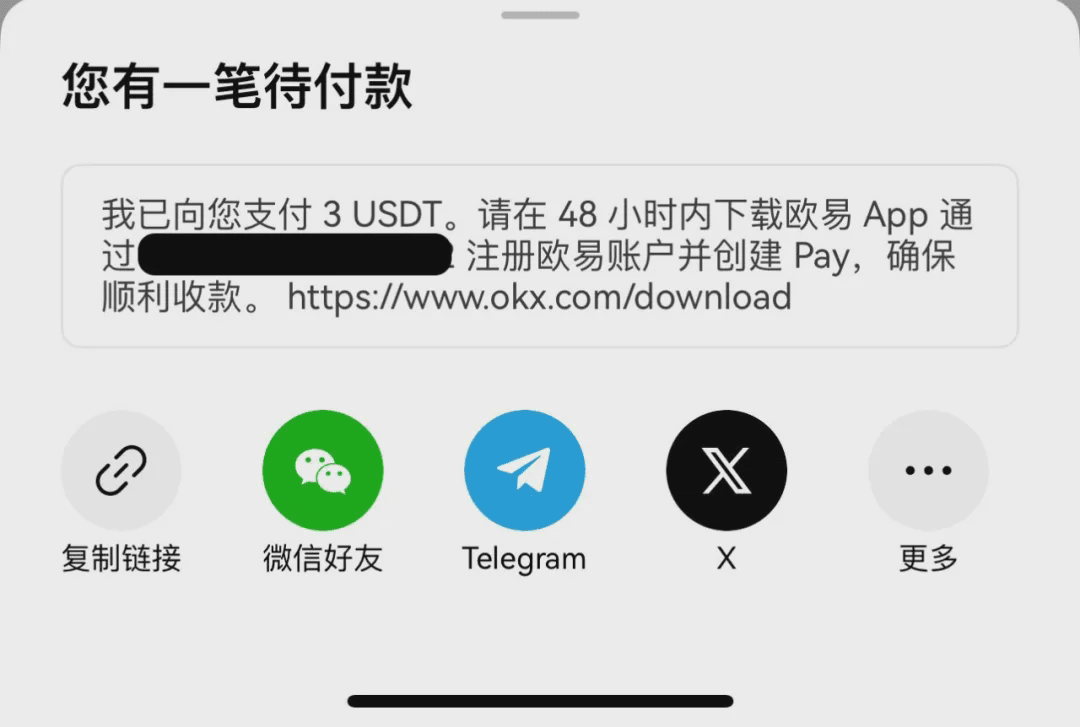

Currently, OKX Pay's PayFi component is focused solely on internal transfers among OKX users, without integration with third-party merchants, relying more on OKX's subsidies and support, including zero transaction fees on the X Layer chain and passive staking rewards. Its true value lies as an ecosystem enhancer, namely 'payment + red envelope fission', promoting deep binding of OKX users and communities through social payments.

During the transfer step, OKX Pay requests access to the user's contacts. If the phone number in your contacts matches an existing OKX account, the transfer can be completed with one click, saving the trouble of finding a wallet address. If the other party hasn't registered yet, the system will automatically initiate a 48-hour 'cooling-off period', temporarily suspending the transfer while guiding you to invite your friend to register for OKX and create an OKX Pay account.

This design is, in fact, a smarter way to attract new users. Compared to traditional 'referral code + reward' mechanisms or various promotional activities to draw people in (the cost per new user can be as high as 20 USD), OKX Pay's transfer invitations naturally carry social trust relationships, making them not only more natural but also cheaper, representing a 'zero-cost social acquisition' that closely aligns with Web3 ecosystem growth logic.

OKX's real ace up its sleeve is actually the KOL community built on Pay group chats, similar to a 'WeChat group' communication mechanism, where KOLs can create group chats and share QR codes, allowing users to join with one click. In this group, KOLs can send red envelopes and discuss crypto market trends while bypassing traditional chat software's regulation of sensitive words, allowing for freer communication and a closer fit to the Web3 atmosphere.

Insiders reveal that OKX specifically hired a product manager from a well-established SocialFi project, DeBox, to tailor this system to the WeChat community model. This move is very 'understanding of Chinese users'—low thresholds and high activity enhance user stickiness while requiring almost no operational investment. Compared to the overseas market dominated by Twitter discourse, this design, which leans towards 'familiar circles of influence', is clearly more compatible with the Chinese community ecosystem and better accommodates the growth demand for the integration of payments and social aspects.

Standing between structural dividends and regulatory gray walls.

Although OKX Pay opens the market with a combination of 'Web3 payments + social asset networks', its long-term development still faces multiple challenges from compliance, user behavior, business models, and geopolitical policies; hidden behind structural dividends are unresolved systemic issues in on-chain payments.

1. Business competition: Closed ecosystems, limited paths.

Although OKX Pay claims to create Web3 payment tools, its current use cases are still mainly limited to internal exchanges, functioning more like a partial functional plugin rather than a payment network that can step out of the exchange to serve a broader ecosystem. Compared to native payment protocols or traditional payment companies, it also lacks independent value and expansion paths.

Limitations of use cases: Currently, OKX Pay is mainly used for asset transfers, red envelopes, and tipping within the platform. These functions are merely small adjustments to the existing financial flow paths, rather than true innovations in payment experience.

Lack of external access: Unlike some native Web3 payment protocols (such as PayFi) that can be integrated by DApps or off-chain merchants, OKX Pay has not opened an SDK or system integration interface, nor has it progressed to support off-chain real payment scenarios.

User habits not established: Products like Binance Pay are also trying to expand payment functions, but overall, payment services from centralized exchanges have not yet become the primary choice for users. It is very challenging for OKX Pay to break through in this aspect.

Difficulty in interoperability between ecosystems: Different exchanges operate independently, and their payment systems are incompatible. Users' payment needs often depend on trust in the platform itself, lacking interoperability and network effects.

2. Legal compliance: Blurred boundaries, significant risks.

Although OKX Pay complies with basic KYC/AML requirements, once it enters the on-chain payment domain, it will face more complex regulatory issues. Compliance is not only a technical process issue but also relates to the platform's boundary of responsibility and legal risks.

Insufficient identity recognition: OKX's KYC can meet exchange compliance requirements, but whether it is sufficient to meet higher standards like cross-border payments and anti-money laundering remains to be confirmed. Especially when users transfer assets out of the platform for on-chain payments, the effectiveness of identity tracking may be compromised.

On-chain transparency brings privacy conflicts: On-chain payments are publicly traceable, and although they do not display real names, they can reconstruct user profiles when combined with off-chain data. Laws such as the EU's GDPR impose strict restrictions on this kind of 'identifiability'. Introducing mixing or zero-knowledge technologies to protect privacy in the future may raise regulatory concerns about 'facilitating money laundering'.

Unclear boundaries of platform responsibility.

If payments fail, transfers are incorrect, or fraud occurs, is OKX obligated to assume arbitration or compensation responsibilities?

In the absence of responsibility definitions like those of third-party payment institutions, can users hold the platform accountable? Should the platform assume functions like freezing funds and dispute resolution?

Regulatory definitions remain ununified:

Whether OKX Pay belongs to MSB (Money Service Business) or VASP (Virtual Asset Service Provider) depends on local interpretations of its payment functions. Some countries may view it as a wallet tool, while others may consider it equivalent to a payment institution.

Significant global policy differences.

The EU's MiCA regulation has started to establish a unified framework but requires specific execution by member states.

The regulatory landscape in the U.S. is fragmented; agencies like the SEC and FinCEN still blur the lines between trading, payments, and securities.

Southeast Asia and the Middle East have loose regulations, but many countries can later hold accountable under charges such as 'terrorism financing' or 'illegal fund transfers'. The lack of clear compliance paths actually increases uncontrollable risks.

Is OKX Pay a protocol? Or a tool constructed by major companies' ecosystems?

On the surface, PayFi represents the ideal of decentralized protocols, but in practical implementation, especially in the CEX ecosystem represented by OKX Pay, it manifests more as a cleverly packaged SocialFi marketing tool. OKX Pay attracts users through the PayFi concept, strengthens the binding of social interaction and payment behavior, enhances user stickiness and ecosystem activity, reflecting the significant role of major companies in promoting the popularization of Web3 payments.

For the industry, PayFi is both an innovative driver for the realization of Web3 payments and hides the risks of centralization driven by major capital. Meanwhile, as legal regulations gradually improve, the PayFi ecosystem needs to find a balance between compliance and openness, which is both a challenge and a necessary path for promoting healthy industry development.

/ END.

Authors: Mia, Zhao Qirui.