Authors | awxjack; kkone0x; EarningArtist; alexzuo4; BroLeonAus; bonnazhu; 0xHY2049; codeboymadif

Compiled by | Wu Says Blockchain Aki_Chen

This article aims to present various viewpoints truthfully. Regardless of support or opposition, they reflect different thoughts in the market regarding the competition between stablecoins and traditional cross-border payments, and do not constitute any investment advice.

Introduction

In June 2025, Jack Zhang, co-founder and CEO of Airwallex, tweeted repeatedly on social media, openly questioning the actual value of stablecoins in B2B settlements among G10 developed economies, sparking intense discussions among traditional finance and crypto communities regarding cost efficiency, financial freedom in emerging markets, and stablecoin regulation. The surface of this debate reflects differing views on the technological paths of cross-border payments, but at a deeper level, it reflects the clash of ideas between the existing financial system and the open blockchain system. This article presents Jack Zhang's core viewpoints, linking them to Airwallex's development history, licensing layout, and business model, organizing the viewpoints from both sides regarding the Twitter community and traditional financial practitioners. It interprets the positioning of stablecoins in the global payment arena, Airwallex's compliance competitive advantages, and the industry landscape and interest games behind the disputes.

On May 21, 2025, Airwallex completed a $300 million Series F financing round, bringing the company's valuation to $6.2 billion. This round of financing includes $150 million in secondary share transfers, with investors including Square Peg, DST Global, Lone Pine Capital, Blackbird, Airtree, Salesforce Ventures, and several long-established pension funds, with Visa Ventures participating as a strategic investor. After this round of financing, Airwallex's total financing has exceeded $1.2 billion.

Jack Zhang: Stablecoins cannot surpass the existing cross-border payment system.

Recently, Jack Zhang, co-founder and CEO of Airwallex, made a series of comments on Twitter questioning the practicality of stablecoins in cross-border payments between mainstream developed economies. Firstly, he pointed out that for B2B cross-border payments between G10 developed countries, stablecoins do not provide advantages in terms of foreign exchange costs and speed. If payment is made from USD to EUR, the recipient still needs to account in EUR, then the 'off-ramp' cost of converting stablecoins back to fiat currency is often higher than the cost of direct conversion through traditional interbank foreign exchange markets. In other words, in this scenario, stablecoins do not genuinely reduce costs.

He further stated that in his 15 years in the cryptocurrency field, he has yet to see cryptocurrency truly solve any practical problems. Although many have become wealthy by investing in crypto assets, the crypto technology itself has not created real value. Even if the price of stablecoins fluctuates less relative to fiat currencies, Zhang indicated that he still does not see how they can benefit inter-business transactions on a large scale, unless transactions involve obscure 'niche' currencies, which have relatively limited liquidity. He stated that compared to the ubiquitous applications of artificial intelligence, current crypto application cases are quite limited. Moreover, most of the trading volume of stablecoins does not encompass economic activities. Therefore, in his view, the usage frequency and value of stablecoins in the mainstream economy remain very low.

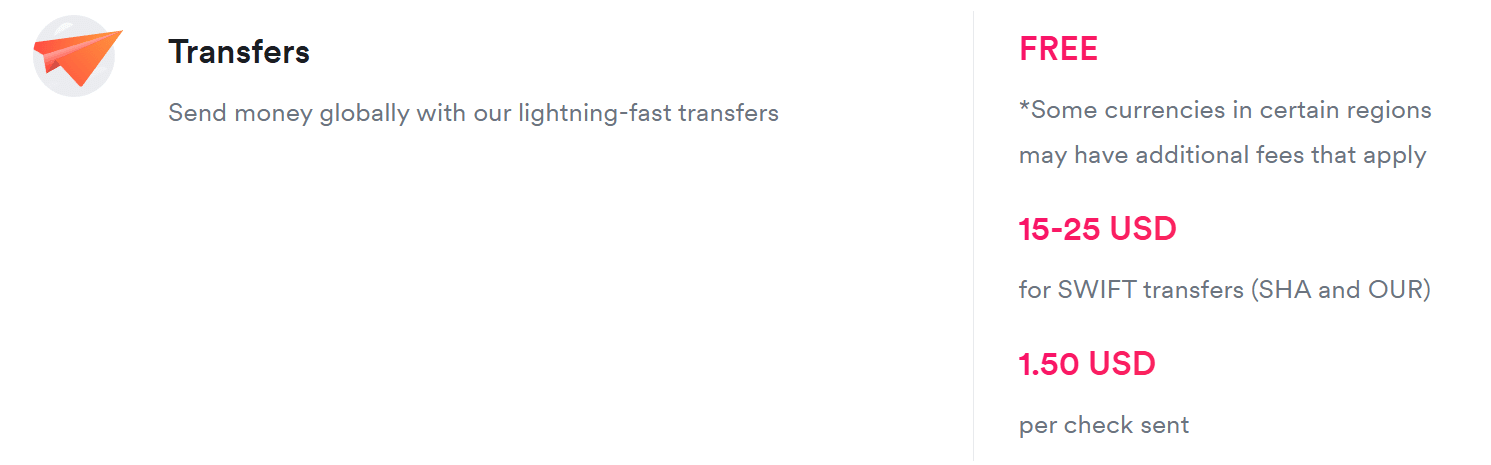

Zhang particularly emphasized that, as of today in 2025, he still 'does not understand how stablecoins can make cross-border transactions better among G10 currencies,' because Airwallex has already achieved real-time and even 'near zero-cost' cross-border settlement services—he stated that the company's current cross-border transfer fees are below 0.01%, which can almost be seen as 'free' and 'instant.' He candidly remarked, 'You can't be cheaper than free, and you can't be faster than real-time.'

The only stablecoin scenario he acknowledges is the business of Bridge, a company acquired by Stripe, which will provide stablecoin wallet infrastructure for consumers in Latin America or Africa. However, in Zhang's view, this practice is more about exploiting regulatory differences for arbitrage rather than a truly disruptive new technology.

Airwallex Company Overview and Business Model

To understand the background of Jack Zhang's viewpoints, it is necessary to understand Airwallex's own product model and business logic. Airwallex (Chinese brand 'Kongzhong Yunhui') was founded in 2015 and is headquartered in Singapore, with offices in 23 countries and regions globally and nearly 1,500 employees. Its business encompasses cross-border transaction collections, payments, foreign exchange conversions, etc., reshaping the traditional flow of cross-border funds through technological means. Its global payment network has covered over 180 countries or regions and served more than 100,000 enterprises, processing over $100 billion in transactions annually. It was co-founded by Jack Zhang and three alumni from the University of Melbourne. At the time of its founding, traditional banks still primarily relied on the SWIFT system established in the 1970s to process cross-border remittances, while Airwallex aimed to use the internet and financial technology to build a faster, lower-cost cross-border payment network. The founding team set a vision: to solve long-standing pain points in traditional financial infrastructure and create a new generation of global banking systems.

Compliance paths covered by licenses in multiple countries.

Unlike many crypto startups that focus on 'decentralization,' Airwallex has regarded compliance licenses and regulatory cooperation as its core competitive advantage since its establishment. The company currently holds payment licenses or financial business permits in over 60 countries and regions worldwide, including major payment institution licenses issued by Singapore's Monetary Authority of Singapore (MAS), electronic money licenses from the Dutch central bank, and prepaid card licenses held through joint ventures in China. These licenses grant it the qualification to operate cross-border payment and foreign exchange businesses legally across multiple countries, enabling it to establish a regulated, secure, and reliable international settlement network. Based on this compliant infrastructure, Airwallex can directly connect with local banking systems, providing enterprise-level account management and fund services while ensuring compliance with anti-money laundering (KYC/AML) regulations.

Global Fund Pool Mechanism and Batch Clearing

Airwallex provides a one-stop global financial service that includes multi-currency corporate accounts, international collections and payments, foreign exchange conversions, corporate cards, expense management, and online acquiring functionalities. Specifically, corporate users can online open global collection accounts within minutes, obtain local collection account information, set up local accounts in over 60 markets, and collect in over 20 currencies. All collected funds are automatically aggregated into the company's multi-currency digital wallet, which supports holding over 23 currencies and converting as needed.

To reduce the costs and delays of cross-border transactions, after obtaining licenses, Airwallex built a proprietary global banking network, establishing direct cooperation channels with Standard Chartered, DBS Bank, Singapore's MAS licensed institutions, and the Industrial and Commercial Bank of China, among others. Airwallex opens local bank accounts in various regulatory regions and deposits funds, forming a distributed 'fund pool.' When customers initiate cross-border payments, Airwallex does not process them one by one through SWIFT, but instead utilizes its fund pool in the destination country to directly pay the local recipient; this achieves 'localized' transmission of funds, avoiding the high fees and slow speeds associated with multiple transfers through the traditional SWIFT network. Meanwhile, the 'pre-funding + internal matching' model deducts the equivalent amount within the originating country's fund pool, circumventing the cumbersome processes of traditional cross-border remittance.

Through these local settlement channels, Airwallex is able to directly clear funds in major markets, and Airwallex's API allows businesses to integrate payment processes with their own systems, enabling intelligent selection and automatic routing of payment paths: for example, automatically matching the optimal channel (local transfer or SWIFT) based on the destination country, and using real-time exchange rates to centralize and complete foreign exchange conversions in batches in the background. To reduce exchange rate losses, Airwallex uses AI algorithms to optimally decide which moment's exchange rate to execute large conversions, balancing cost and time. This automated financial routing ensures that funds flow globally at the lowest cost and fastest speed, allowing Airwallex to claim 'near real-time, near zero-cost' transfers in major currencies.

Stakeholders and partners

During its business expansion, Airwallex has established partnerships with several industry-leading partners. Firstly, in the card business, it has reached a global strategic cooperation with Visa to jointly launch the 'Airwallex Borderless Visa Card'—this allows Airwallex to issue multi-currency virtual and physical cards as a BIN sponsor of Visa, and Visa has also participated in Airwallex's subsequent financing.

Additionally, Airwallex has partnered with the international card organization Discover to expand its payment market access in the UK, enhancing services in the UK through virtual accounts and local payment channels. In the enterprise software sector, Airwallex has closely collaborated with Xero (a well-known cloud accounting software in New Zealand): the two parties have established a long-term strategic partnership to integrate Airwallex accounts with Xero's bookkeeping, supporting billing payment links embedded in Xero invoices, accelerating the collection process for SMEs. Through this cooperation, collections to Airwallex's multi-currency accounts can be directly marked for reconciliation, enabling businesses to invoice and collect in over 170 currencies without unnecessary currency conversion.

In the e-commerce sector, Airwallex has become one of Shopify's official payment partners, providing Airwallex payment plugins for Shopify merchants. Merchants can accept payments from global customers through this plugin and directly settle sales proceeds into Airwallex's multi-currency wallet, avoiding currency conversion losses. Shopify has also chosen Airwallex as its payment gateway, aimed at helping merchants reduce the foreign exchange costs of cross-border payments and improve capital turnover efficiency. Additionally, Airwallex has established system integration with major cross-border e-commerce platforms (such as Amazon, eBay, Lazada, Shopee, etc.), allowing sellers to link their Airwallex accounts to these platforms for instant payment collection and bulk foreign exchange settlement. In terms of financial management, Airwallex also provides integration plugins with ERP and accounting software such as Oracle NetSuite and QuickBooks, making it convenient for businesses to access Airwallex's payment functionality within mainstream financial systems. These extensive ecosystem collaborations enhance the stickiness and channel acquisition capability of Airwallex's services, reflecting its positioning not just as a payment tool but as a foundational financial network embedded in various industry scenarios.

Revenue model breakdown

As a fintech platform, Airwallex primarily generates revenue through transaction fees and the spreads on exchange rates; its business model essentially represents payment-as-a-service as a B2B financial infrastructure.

Specifically, foreign exchange revenue is an important component: Airwallex claims to provide customers with rates close to the mid-market rate, but in reality, they charge about 0.2%–0.5% as a fee for the foreign exchange difference during conversion. Since many customers use Airwallex for multi-currency fund conversions, this accumulated contribution generates considerable revenue.

Secondly, international payment fees are also a source of income. Although Airwallex implements a free strategy for most local transfers, if customers choose SWIFT lines or non-primary currency lines, a fixed fee is charged for each cross-border remittance, and for some regional accounts, Airwallex charges a 0.3% processing fee on incoming funds (from third-party payers). These fees also contribute to revenue in large transactions.

Thirdly, Airwallex's merchant acquiring business generates revenue from payment processing fees: when merchants use its payment gateway to collect payments, each transaction is charged a rate ranging from 2.8% to 4.3% based on card organizations and regions. This part of the business is similar to payment companies like Stripe, profiting through transaction commissions.

Fourthly, although the card issuance business itself is free to customers (no issuance fees, no international transaction fees), Airwallex can earn a share from the interchange fees of card transactions as the issuer of Visa cards, and enhance customer stickiness through corporate cards to increase revenue from other businesses.

Fifthly, as the scale of funds deposited on the platform increases, Airwallex begins to generate interest income: the funds retained in customers' multi-currency wallets bring interest revenue to the company, especially after the global interest rate increase in 2023, which has led to significant growth in this income (Airwallex disclosed that part of its revenue growth comes from customer fund interest).

Finally, Airwallex also charges for value-added services and platform integration, such as customized solutions for large platform customers and higher API call limits, which will adopt a separate pricing negotiation model. Overall, Airwallex's business model relies on expanding transaction volumes: by providing near-free basic functionalities to attract customers, then profiting from tiny rates on massive transactions.

Airwallex uses real costs: pricing and user feedback

According to Airwallex's publicly disclosed charging policy, it first claims that Airwallex has no account opening fees, no monthly fees, and no hidden fees, and that local accounts opened on the platform can receive local transfer funds for free.

However, in some specific scenarios, users have discovered unexpected fees. For instance, in Hong Kong, Airwallex charges a 0.3% fee on deposits from third parties, but this fee was not clearly communicated previously; even its automated customer service once provided erroneous information of 'free.'

Regarding international transfer fees, cross-border payments via Airwallex are free in most cases, especially when using its local payment network instead of SWIFT. Only in certain cases (such as when the destination does not cover local channels) where SWIFT wiring is required, a fixed fee of about $15–25 is charged per transaction.

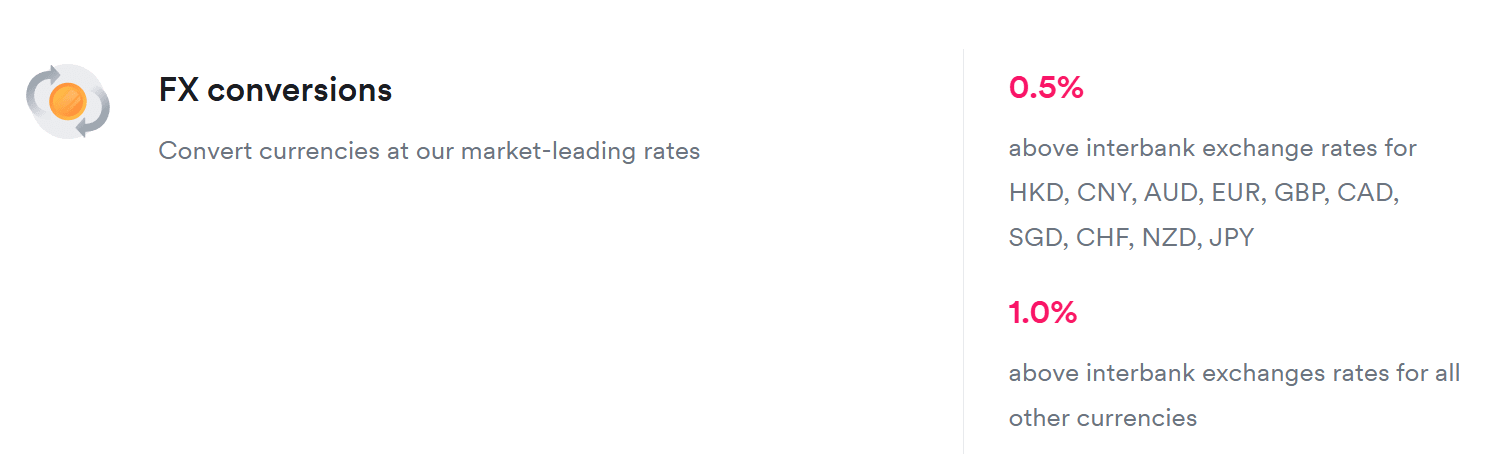

Regarding foreign exchange conversion fees, Airwallex offers highly competitive rates, adding only about 0.2%–0.5% as a conversion fee on top of the market mid-rate (specific additions depend on the currency and region, generally around 0.5% for mainstream currencies). This rate is significantly lower than the typical 1%-3% foreign exchange spread common in traditional banks.

Regarding payment acquisition fees, Airwallex charges merchants a percentage of the transaction amount for online collections: the payment rate for locally issued bank cards is about 2.8% + a fixed $0.30 per transaction, while the international card payment rate is about 4.3% + $0.30; local e-wallets or transfer alternatives generally charge $0.30 per transaction plus the cost rate of each payment method.

In terms of corporate cards and expense management, Airwallex provides clients with free virtual/physical multi-currency cards, with no monthly or transaction fees; the accompanying expense reimbursement and control software is currently also free in most regions to enhance user adoption (in some regions like Hong Kong, a fee of HK$40 per card per month for advanced reimbursement features was previously charged but has been removed in subsequent versions).

Overall, Airwallex's public pricing system highlights a 'low rate' selling point: basic operations at zero cost, with transaction fees significantly lower than those of banks and mainstream competitors, claiming 'no hidden fees.' By pre-placing liquidity globally and building a fund pool, it has achieved localized processing of cross-border transfers. Although this model bypasses the intermediary fees of traditional banks, reducing the marginal cost of each transaction, it carries substantial fixed operating costs behind it: compliance investments for obtaining licenses in multiple locations, the cost of maintaining thousands of bank accounts for fund deposits, management fees for personnel and technology, etc. Airwallex needs to have sufficient transaction volume to amortize these operating expenses, thereby serving customers with low rates while remaining profitable. Thus, it resembles a business model driven by economies of scale: the more transactions, the lower the unit cost.

However, for any latecomer, replicating such a global network requires substantial investment and time. High barriers to entry ensure that pioneers like Airwallex maintain a competitive advantage in the short term, which also means that its cost structure includes a considerable premium. Yet user experiences and feedback indicate that despite the attractive official rates, some fee explanations from Airwallex are unclear. For example, in Hong Kong accounts, the system backend actually charges a 0.3% fee for each deposit from non-affiliated accounts, but previously, Airwallex's bot customer service provided misleading information of 'zero fee,' and this inconsistency makes it difficult for users to understand the true costs in a timely manner.

On the other hand, emerging on-chain stablecoin payments are taking another path. For example, on the crypto network, transferring funds across borders using stablecoins like USDC may incur transaction fees of less than $1 and arrive instantly. However, considering that stablecoins ultimately need to enter and exit fiat currency, users often have to cash out through over-the-counter trading or exchanges, possibly incurring spreads of 0.2%–0.5% and withdrawal fees in the process. If unclear regulations lead to increased compliance costs, these implicit fees may far exceed those of traditional financial channels. Overall, the emergence of Airwallex has lowered the traditional cost standards for cross-border payments, providing businesses with a compromise option between banks and crypto networks.

Twitter community response: both support and skepticism coexist.

The public questioning by Jack Zhang regarding stablecoins has sparked heated discussions among tech finance media, industry research institutions, and social platforms. Based on various comments, viewpoints are generally divided into two camps: one side tends to believe that licensed financial networks like Airwallex can still suppress the rise of stablecoins in cross-border payments in the foreseeable future, while the other believes that stablecoins are likely to gradually replace traditional payment tracks in specific scenarios.

Supporters: Stablecoins are unlikely to shake the traditional cross-border payment networks.

Viewpoint 1: The efficiency of the existing system has significantly improved.

Many industry insiders agree with Jack Zhang's viewpoint, believing that his criticism is based on real data and experience, and is a rational expression. Supporters point out that in the context where efficient payment architectures have already been established in mainstream economies like the G10, stablecoins do indeed lack disruptive advantages. The speed and cost of interbank payments have improved significantly, and some regions' instant payment systems (such as SEPA instant, FedNow, etc.) make cross-border transfers nearly real-time, with fees approaching zero. Supporters argue that rather than risking compliance by trying new things, it is better to make full use of existing systems.

Viewpoint 2: The hidden costs of stablecoins are high and tax violations are a concern.

Comment from alexzuo4 states that Jack's viewpoint reflects a realistic perspective: starting from the B2B scenario, for markets with a well-established banking infrastructure, the costs and efficiencies of the existing system are already high, leaving little room for stablecoins.

EarningArtist also agrees with this view and summarizes the core points of Jack's remarks: in B2B payment scenarios, the cost of converting stablecoins back to fiat (off-ramp cost) is very high, providing no advantage compared to direct remittances via platforms like Airwallex; furthermore, stablecoins cannot directly serve taxation and may even help bypass taxes, thus raising compliance issues.

Viewpoint 3: Regulatory and trust issues.

Many supporters question the regulatory legitimacy and lack of credit endorsement for stablecoins, stating that 'issuing currency is the central bank's responsibility, and private stablecoins walk on the edge of regulation.' They worry that widespread use of stablecoins may disrupt financial order, as ordinary businesses trust payment networks supported by central banks more. Frequent risk events exposed by stablecoins (such as algorithmic stablecoin crashes and reserve transparency issues) are also cited to illustrate their unreliability.

Viewpoint 4: The scenarios for stablecoins are limited.

Compliance risk is the primary issue; if businesses attempt to transfer funds from heavily regulated jurisdictions to unregulated chains and then back to local fiat currencies, the entire chain contains legal and compliance uncertainties. Jack does not completely deny stablecoins but emphasizes their situational limitations. For example, there are indeed emerging market users who turn to USDT due to unstable local currencies, but these markets often come with high risks and money laundering concerns, making it difficult for legitimate businesses to participate. These individuals believe that stablecoins serve more the needs of crypto trading and gray areas, with little relevance to the daily operations of mainstream businesses. The existing system can meet the cross-border needs of most compliant enterprises, making stablecoins non-essential for the mainstream market.

For regions without bank accounts or unstable currencies, stablecoins may have their utility, but in mainstream fiat markets, an efficient solution has already been provided through a complete compliance infrastructure, making it unlikely that stablecoins will replace this network. Overall, supporters believe that the application focus of stablecoins should be on marginal areas that are not covered by the existing financial system (such as underdeveloped regions, unbanked populations, etc.), rather than attempting to compete directly with mature markets and banking systems. This perspective asserts that the regulated financial networks represented by Airwallex have significantly improved efficiency in the cross-border realm, and stablecoins lack disruptive advantages in comparison, facing challenges to be adopted by mainstream businesses due to regulatory and trust issues.

Opponents: Stablecoins may rise in specific scenarios.

Viewpoint 1: Stablecoin rates are lower and the system is better.

Many advocates in the crypto field have also questioned and disagreed with Jack Zhang's statements. Supporters of this position argue that the value of stablecoins is not just about how much money can be saved, but rather about providing a better payment clearing system. Simon Taylor commented that Jack's understanding of stablecoins is superficial; he only sees the fees and overlooks their fundamental significance. Stablecoins achieve point-to-point instant clearing and full transparency, with funds not needing to pass through layers of accounts and intermediaries, naturally reducing friction. Even if they have not yet completely replaced the old system, they are already a better solution in terms of system design. Some users have pointed out that Airwallex's own services are not without costs or delays.

For instance, kkone0x mentioned that although Airwallex advertises extremely low exchange rate fees, there are still potential costs such as account opening fees and deposit fees; in actual use, sometimes funds do not arrive in real-time, and some international transfers may even take days to process. These hidden costs and timeliness issues make stablecoins competitive in certain cross-border remittance scenarios. For example, some netizens cited the case of Filipino overseas workers using USDT to remit back home, where recipients exchange it for fiat currency in the local over-the-counter market, with overall fees still lower than traditional remittance methods. This indicates that stablecoins have already shown potential for cost reduction and speed enhancement in specific remittance scenarios.

Viewpoint 2: A new paradigm rather than a mere adjustment of the old track.

Some people view this matter as a struggle between traditional finance and new finance. For example, commentators like BroLeonAus and 0xHY2049 believe that Jack's statement reflects the struggle between traditional financial gatekeepers and the new forces in crypto over 'settlement rights' and 'pricing power.' Emerging institutions like Airwallex, while innovative, are still reformers within the existing financial system, while stablecoins and decentralized finance attempt to fundamentally reshape the rules of the game. The so-called compliance barriers of stablecoins are also barriers set by traditional fields, which will gradually be dismantled with the explosion of stablecoins.

Others focus on the future technological landscape, believing that Jack has underestimated the long-term value of blockchain payment networks. Commentators like xiaoxoca and bonnazhu argue that stablecoins are still in their growth phase, and as more people use them, they may gradually form network effects and build a real on-chain settlement network, bypassing the traditional banking system; this is the fundamental reason for their revolutionary potential. Although currently stablecoins require over-the-counter channels or banking routes for fiat conversion, as more merchants directly accept stablecoins and more financial services go on-chain, stablecoins are expected to form an autonomous payment loop, significantly enhancing cross-border transaction efficiency. That is, the entire process from payment to storage is completed on-chain and within the stablecoin system, without relying on fiat currency banking channels.

Once such closed loops mature, they will significantly reduce costs, improve efficiency, and impact the status of traditional cross-border payment networks. Especially in regions with weak financial infrastructure, stablecoins will find real demand. For example, the fintech company Juicyway in Africa has completed a cumulative $1.3 billion in cross-border payment transactions using stablecoins without needing to establish a banking network. Similarly, payments between Nigeria and Brazil, which take several days through traditional systems with multiple intermediary banks, can be completed in minutes using stablecoins, with fees far lower than bank wire transfers.

Stepan Simkin, CEO of fintech startup Squads, responded on the X platform, pointing out that the true disruptive nature of stablecoins lies in empowering a new generation of startups to build financial services faster and cheaper. He likened the traditional banking system to a 'high-cost, high-latency' legacy system, while stablecoins allow entrepreneurs to launch global financial products with smaller teams and shorter cycles, which is agility that traditional institutions cannot provide.

Viewpoint 3: Financial inclusiveness and disintermediation.

Paolo Ardoino, CEO of Tether and a representative figure in the crypto industry, voiced from the perspective of financial sovereignty, criticizing the banking industry's resistance to stablecoins as a means to maintain its monopoly position. He believes that in countries with high inflation and strict regulations, stablecoins offer ordinary people a means of financial independence and a counter to policy risks; their significance lies not just in payment efficiency, but in reshaping the financial power landscape. Currently, over 1 billion people lack access to basic financial services because the compliance costs and profit motives of the existing system make it disinterested in servicing long-tail populations. Stablecoins, combined with mobile phones and the internet, allow anyone in the world to directly hold the value of the dollar and conduct global remittances and transactions. In their view, Jack's so-called 'regulatory arbitrage' is actually the new financial order taking root in places the traditional system cannot reach.

Summary: 'Institutional Battle' or 'Market Choice.'

Looking beyond the phenomenon to the essence, the dispute between Airwallex's CEO and stablecoin supporters is both a battle of institutional paths and a difference in user positioning. The former represents a defense of the boundaries of the compliant financial system and a wariness of new entities, while the latter represents the challenge of open crypto networks to traditional monopolies and a commitment to inclusive visions.

From an institutional perspective, the debate reflects the fundamental contradiction between centralized finance and decentralized finance. Traditional finance is accustomed to a regulated, centralized system that emphasizes security, stability, and controllability; while the crypto world advocates a system of no borders and autonomy in the hands of users, emphasizing efficiency, transparency, and inclusiveness. When stablecoins—a product that lies between the two—emerge, the former instinctively questions their legitimacy and necessity, while the latter views them as a tool to disrupt the old order. This is essentially a clash of financial paradigms: ledgers shift from banks to blockchains, credibility transforms from institutional endorsements to algorithms and consensus. At this level, both sides are contending for dominance over the future financial landscape. It is foreseeable that as stablecoins gradually enter compliance (with various countries' regulations being implemented), this institutional tension will ease, but the inevitable competition will become increasingly fierce.

From a market perspective, this debate presents a picture in which users and scenarios choose according to their needs. Airwallex's model serves global enterprises that require efficient cross-border financial services that integrate with existing banking systems, are legal and compliant. Airwallex meets their pain points, thereby achieving commercial success. The stablecoin model attracts marginal markets and individual users who are either underserved by traditional systems or are seeking alternatives due to distrust in their local currency (in regions with severe currency inflation) or dissatisfaction with capital controls. In the eyes of these individuals, stablecoins are a timely aid. Therefore, the two are not simply alternatives but rather seem to excel in different segmented markets. At least for now, both Airwallex and USDT have their own survival soil.

Perhaps both sides of the debate need some perspective. For traditional finance people, it should be recognized that technological advancements bring structural changes: stablecoins are not just a new tool; they signify a more flat and open financial architecture, and their long-term impact may exceed current imaginations. Even if the price of DVD rentals was pushed to the extreme back then, it still could not compete with the rise of streaming services, because the latter changed not just the price, but the model itself. Similarly, even if banks and payment companies reduce cross-border fees to zero, the complexity and exclusivity of account systems still exist; blockchain thinking provides another answer. Conversely, for the crypto industry, it should also acknowledge the importance of financial stability and trust: relying solely on technological advantages cannot resolve everything; large-scale applications of financial tools must address regulatory compliance, consumer protection, and other issues. If stablecoins are to truly become the cornerstone of future finance, they must integrate into the human trust system, rather than remain self-enclosed on an island of idealism.

codeboymadif provided a comprehensive perspective on this dispute. He analyzed the discussion through dimensions such as product form, network effects, and applicable scenario range: under the current framework, Jack Zhang's judgment that stablecoins lack advantages is valid, as existing interbank networks and compliant platforms like Airwallex already provide nearly optimal solutions in the mainstream market. However, he also acknowledged that there are uncertainties in the long run—as technological advancements and market conditions change, new tools such as stablecoins may find breakthroughs in the future. Therefore, assessments of the future potential of stablecoins should not be one-size-fits-all; there remains room for discussion between short-term pragmatism and long-term vision.

These viewpoints emphasize that although stablecoins are currently marginal in mainstream enterprise payments, their growth curve is exceptionally bright in specific domains, and in the long run, they may expand from the margins to the mainstream. Especially as future regulatory frameworks gradually clarify, stablecoins, if they can resolve issues of trust and compliance, have every opportunity to become a significant track in cross-border payments, potentially even replacing parts of traditional networks.

Link:

https://x.com/awxjack/status/1931239220204486879?s=19

https://x.com/kkone0x/status/1931673643995824332?s=19

https://x.com/EarningArtist/status/1931647964772229521?s=19

https://x.com/alexzuo4/status/1931680650584891761?s=19

https://x.com/BroLeonAus/status/1931750507611374070?s=19

https://x.com/bonnazhu/status/1931708632598757493?s=19

https://x.com/0xHY2049/status/1931674658182500740?s=19

https://x.com/codeboymadif/status/1931722361843470773?s=19

https://x.com/portal_kay/status/1931946852276150405?s=19