Author: Barter

Compiled by: Tim, PANews

Stablecoin swaps: The good and the bad

The total supply of stablecoins nearly doubled in 2024, increasing from $129.8 billion to $203.4 billion, with more than half existing on the Ethereum chain. In the face of dozens of stablecoins circulating in the market and new coin types constantly emerging, ensuring liquidity swaps remain as close to a 1:1 exchange rate as possible is crucial. The Barter team conducted in-depth research and found: practice

Stablecoin swaps often deviate from the 1:1 exchange rate; this post will analyze the issue.

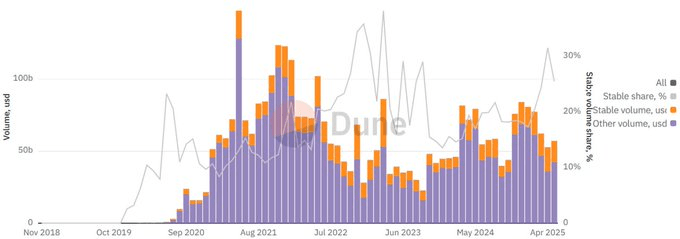

Seemingly ordinary, yet incredibly valuable

According to DEX trading data, the proportion of stablecoin trading volume in total trading volume has remained in the range of 20-30%, while its transaction count ratio has consistently been below 5%. During April 2025, the proportion of stablecoin trading volume reached 31.5% (absolute value of $16.6 billion), with the transaction count ratio only at 4.6%. This means that the average size of a single stablecoin transaction is 9.5 times that of a regular DEX transaction.

The lower the TVL, the higher the efficiency

The TVL of stablecoin liquidity pools has dropped from a peak of $12.3 billion in January 2022 to $600 million in May 2025. However, since the beginning of 2022, the trading volume of stablecoins has continued to grow, resulting in a 34-fold increase in liquidity turnover rate, with the weekly turnover rate reaching as high as 824% by April 2025. This means that: the market structure is shifting towards higher capital efficiency, and liquidity pools now support significantly expanded trading volumes.

Stable exchange ≠ stable execution

In the past year, retail trading involving stablecoins encountered slippage losses exceeding 0.1% amounting to $8.1 billion. Among these, $930 million of trades experienced slippage exceeding 1%, which is considered abnormally high in stablecoin exchanges, and 78.5% of the high slippage trades were concentrated in trading pairs with poor liquidity.

Although a 1% slippage might seem trivial at first glance, in the context of high trading volume stablecoin exchanges, it exposes deeper issues of scale efficiency. Therefore, stablecoin exchanges currently account for 53.8% of all sandwich attack trades, while MEV (miner extractable value) and arbitrage trades account for 47.0% of the total trading volume of stablecoin exchanges, equating to $1.61 billion weekly.

Low fees but high costs

The root cause of the high proportion of harmful trades in stablecoin swaps lies in fee compression. Over the past two and a half years, the average transaction fee for stablecoin swaps has plummeted by 5.5 times to just 0.011%, with the volume-weighted fee even as low as 0.005%. Although low fees can attract order flow, they have also led to an abnormal increase in the proportion of harmful trades. For example, on the Uniswap V4 platform, which offers an ultra-low fee of 0.001%, harmful MEV trades have now reached as high as 80.2% of the stablecoin swap trading volume.

Value analysis of friction costs in stablecoin exchanges