May 8, 2025 — The American housing market is no longer a young person’s game. It’s a waiting game — and Gen Z is losing.

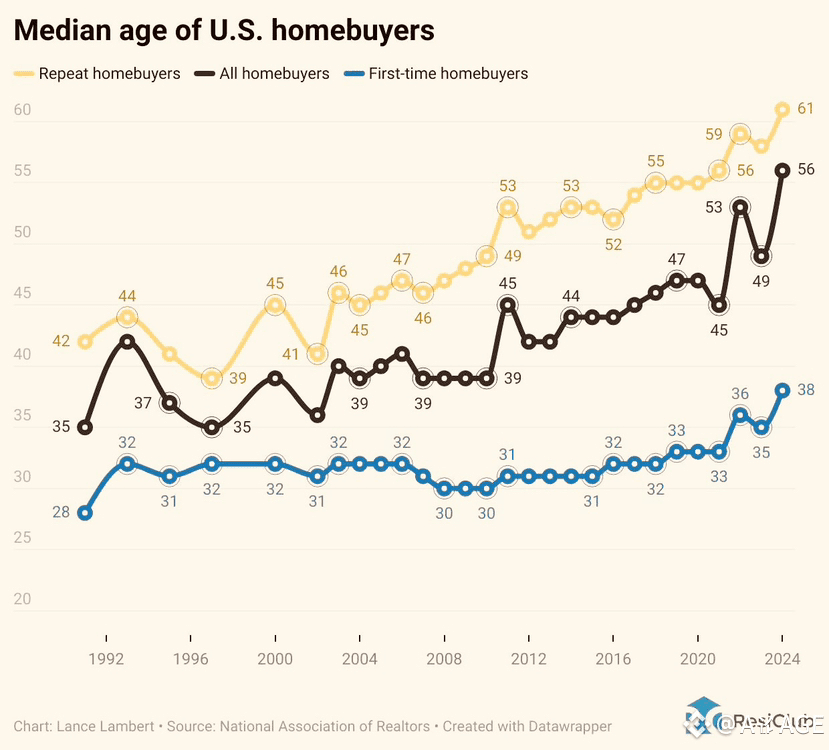

According to the latest report from the National Association of Realtors, the median age of first-time homebuyers in the U.S. has reached 38 years, a historic high. In 1991, it was just 28. Repeat buyers now average 61, while the overall average age of all buyers is 56.

This is more than economic drift. It’s a structural, generational lockout.

Since 2020, the convergence of housing inflation, post-COVID supply constraints, and sharply rising mortgage rates (especially after 2022) has made entry-level ownership nearly impossible. Home prices soared. Loan approvals tightened. Down payments grew heavier. And real wages? Mostly stagnant.

Millennials and Gen Z — once expected to drive a new era of ownership — have been pushed to the margins. Student debt levels remain record-breaking. Average educational duration has extended. Career starts are delayed. Many young adults now postpone marriage, children, and housing — all the traditional hallmarks of “growing up.”

Meanwhile, older Americans — Boomers and Gen Xers — continue to dominate the market with cash offers, equity-rich portfolios, and paid-off mortgages. They are less rate-sensitive, better hedged, and more mobile. They downsize, relocate, or invest in second homes — often skipping the bank altogether.

This shift is also psychological. For many younger Americans, the “starter home” isn’t just unaffordable — it’s mythological. They’re locked in cycles of renting, urban transience, or cohabitating with family well into their 30s.

But how does this compare globally?

In Germany, the median first-time buyer is 34. In Japan, 36. In France, 33. Even in Canada, where housing is notoriously expensive, the average first-time buyer is still younger than in the U.S. — around 35. The U.S. now ranks among the oldest homebuyer populations in the developed world.

Why? The American system still relies heavily on private credit risk, individual down payments, and volatile mortgage markets. Many other nations offset this through state-backed housing programs, rent control, or co-investment structures — models largely absent in the U.S.

So what’s next?

The future of U.S. housing may depend on how fast policymakers react. Will there be tax relief for first-time buyers? Student loan forgiveness tied to mortgage eligibility? More accessible credit frameworks for Gen Z?

Or will homeownership become a privilege of the aged and affluent, leaving an entire generation behind?

To the #AMAGE community:

Is this the death of the American Dream — or the start of a new economic reality?

What needs to change for young Americans to break back into the market — and who’s responsible for unlocking the door?