MicroStrategy's recent operations can be described as 'daring' to the point of shocking. On one hand, they are wildly issuing stocks, and on the other, they are using the funds raised to buy bitcoins (BTC) in large quantities, even mortgaging their bitcoins for financing to continue issuing stocks... This approach is so extreme that describing it as 'aggressive' seems too conservative; it is almost like a 'tightrope act' continuously spinning in the financial sky. As long as the price of bitcoin continues to rise, everything appears picturesque; but once the market experiences even a slight disturbance, the entire plan could collapse in an instant. However, the market never develops according to anyone's script.

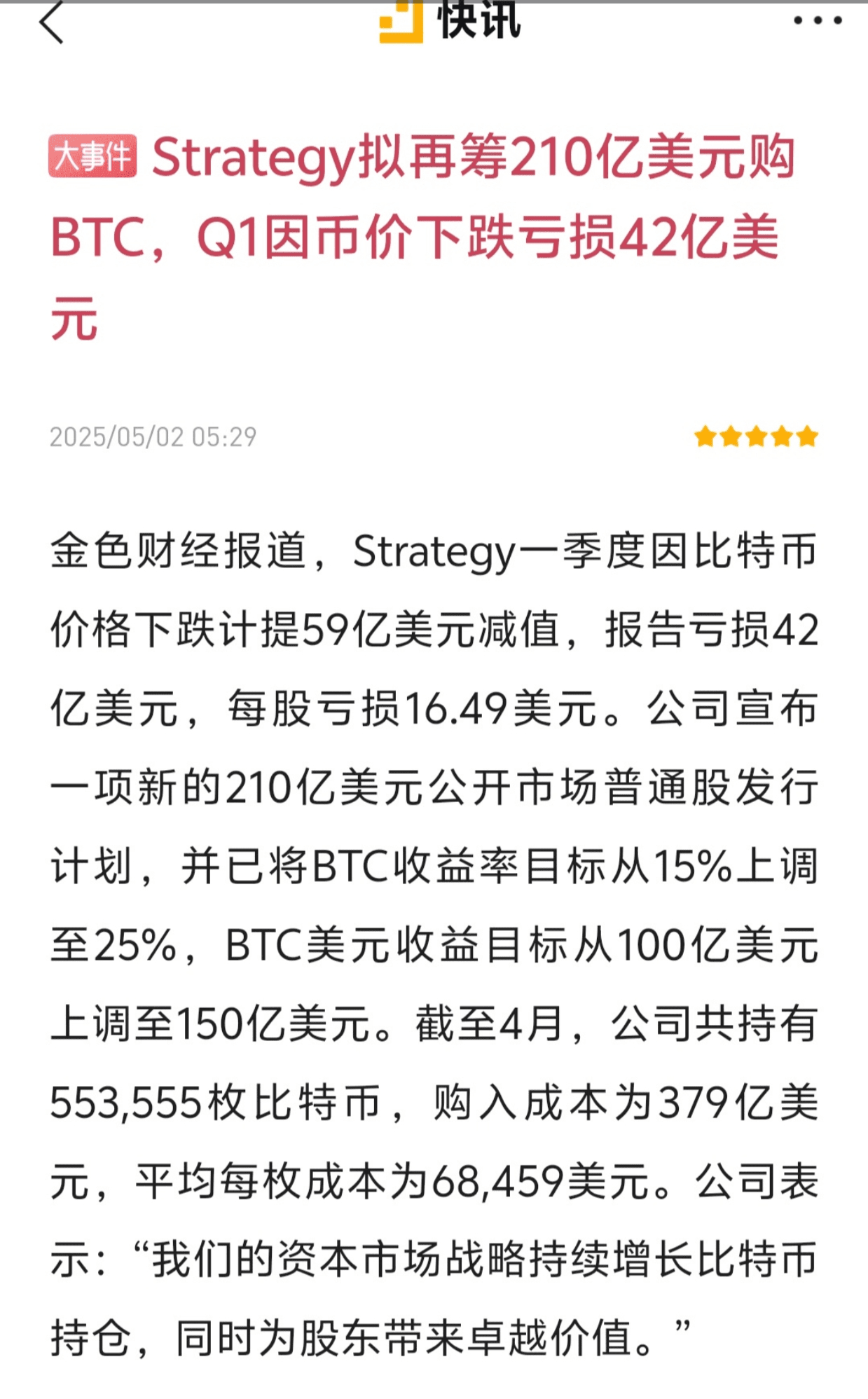

According to MicroStrategy's latest financial report, the decline in bitcoin prices in the first quarter has caused the company to suffer heavy losses, amounting to as much as $4.2 billion, equivalent to a loss of $16.49 per share. Logically, such a massive loss should prompt the company to act cautiously, but MicroStrategy has done the opposite, announcing a common stock issuance plan of up to $21 billion to continue buying bitcoin aggressively. Not only that, but they have also raised their bitcoin yield target from 15% to 25%, and the profit target has skyrocketed from $10 billion to $15 billion. This operation is simply so radical that describing it as 'doubling down on faith' is insufficient.

The problem is that MicroStrategy's asset volatility has completely depended on the price movements of bitcoin, and its core business has long been submerged by virtual asset investments. To some extent, MicroStrategy is no longer a traditional software company but more like a 'quasi-ETF' bitcoin position disguised as a public company. They use funds raised through stock financing to buy bitcoin, and after the bitcoin price rises, they continue to mortgage for financing to buy more bitcoin. This sounds like a perfect cycle, but in reality, it is a high-risk game of multiple leveraged snowballing. In other words, MicroStrategy's growth model is now deeply tied to the price of bitcoin: when bitcoin prices rise, everything seems beautiful; when bitcoin prices fall, it is like walking on a paper bridge, which could collapse at any moment.

The most crucial point is that this high-risk structure is no longer just a matter for MicroStrategy itself. Currently, MicroStrategy holds over 550,000 bitcoins, accounting for 2.6% of the total circulating supply. If this massive position collapses, it won't just be MicroStrategy that faces ruin; the entire cryptocurrency market could suffer a significant shock, potentially triggering a new round of market panic. MicroStrategy has become not just a 'time bomb' but a 'super bomb' that could ignite a secondary confidence crisis.

From a regulatory perspective, MicroStrategy's approach clearly walks a gray area. In traditional finance, a public company that continuously issues stocks to speculate on high-volatility assets, even using assets it has purchased to repeatedly finance and buy similar assets, should have long been under strict scrutiny by the U.S. Securities and Exchange Commission (SEC). However, the current cryptocurrency market is still in a regulatory gray area, and MicroStrategy's model not only circumvents the compliance restrictions of ETFs but also takes advantage of the financing convenience of public companies, making it a 'arbitrage expert' in the gaps between traditional rules and new finance.

Of course, we cannot completely deny MicroStrategy. They have indeed integrated 'Bitcoin faith' into their corporate strategy in an extremely aggressive manner, and their influence has far surpassed many crypto-native enterprises. However, the problem is that once this model enters a bear market, it may not only be MicroStrategy that suffers backlash, but it could also trigger a collapse in confidence for a series of positions. If the previous FTX collapse was the exchange version of a trust crisis, then MicroStrategy might be the next 'time bomb' in the public company version.

Investment itself has no right or wrong, but from MicroStrategy's path, the stronger the faith, the more aggressive the leverage, and once the market turns, the pain of decline becomes deeper.

#非农就业数据来袭 #币安HODLer空投STO #加密市场反弹 #BTC走势分析 #ETH $BTC