The Federal Reserve 'breathed a sigh of relief'.

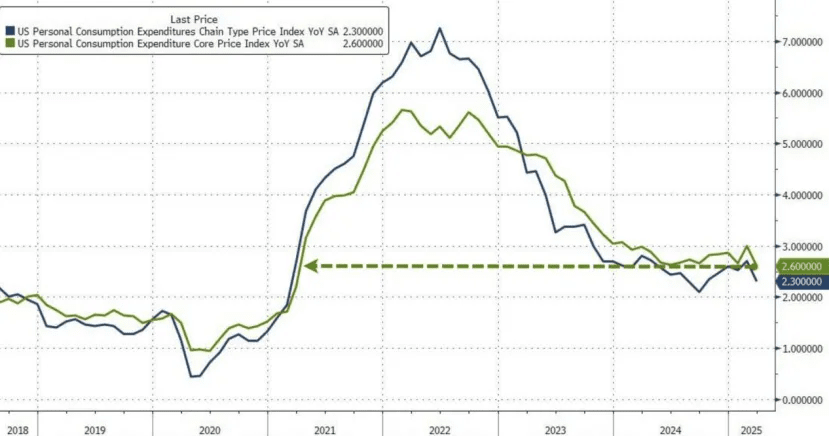

The Fed's preferred inflation indicator unexpectedly cooled, raising market expectations for a rate cut. The latest data from the U.S. Bureau of Economic Analysis shows that the U.S. PCE price index rose 2.3% year-on-year in March, the lowest level since last fall; the core PCE price index rose 2.6% year-on-year, down from the previous value of 2.8%; both PCE and core PCE remained flat month-on-month.

After the data was released, it alleviated market concerns about a resurgence of high inflation in the U.S., with traders expecting the Fed to cut rates four times by 25 basis points before the end of 2025. The CME 'Fed Watch' tool shows that the probability of a rate cut next week is 5.6%, but the probability of a cut in June has risen to 65.5%.

The market is currently closely watching the U.S. non-farm payroll data report for April, which will be released on Friday. If the U.S. labor market experiences severe turmoil due to the Trump administration's tariff policies, the probability of the Fed initiating its first rate cut of the year in June may significantly increase. Fed Governor Waller has repeatedly emphasized that if high tariff policies force U.S. companies to make larger-scale layoffs, he will support a rate cut to protect the U.S. labor market.

A piece of good data

On April 30, Eastern Time, the U.S. Bureau of Economic Analysis released data showing that the Fed's preferred inflation indicator—the U.S. PCE price index—cooled in March.

Specifically, the U.S. PCE price index in March rose 2.3% year-on-year, the lowest level since last fall, slightly higher than the expected 2.2% and a previous value of 2.5%; the month-on-month PCE price index for March was 0%, in line with expectations, with a previous value of 0.3%, marking the first time in nearly a year that PCE month-on-month remained flat; the core PCE price index in March rose 2.6% year-on-year, in line with expectations, with a previous value of 2.8%. The month-on-month core PCE price index for March was 0%, in line with expectations, with the previous value revised from 0.37% to 0.5%. The month-on-month core PCE also remained unchanged, marking the mildest reading in nearly five years.

The Federal Reserve, sudden good news!

Original

Zhou Le

Securities Firm China

May 1, 2025 15:22

Guangdong

3582 people

The Federal Reserve 'breathed a sigh of relief'.

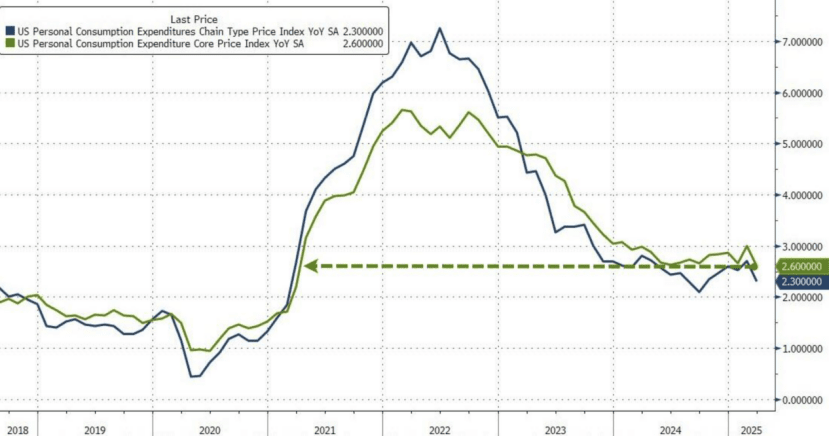

The Fed's preferred inflation indicator unexpectedly cooled, raising market expectations for a rate cut. The latest data from the U.S. Bureau of Economic Analysis shows that the U.S. PCE price index rose 2.3% year-on-year in March, the lowest level since last fall; the core PCE price index rose 2.6% year-on-year, down from the previous value of 2.8%; both PCE and core PCE remained flat month-on-month.

After the data was released, it alleviated market concerns about a resurgence of high inflation in the U.S., with traders expecting the Fed to cut rates four times by 25 basis points before the end of 2025. The CME 'Fed Watch' tool shows that the probability of a rate cut next week is 5.6%, but the probability of a cut in June has risen to 65.5%.

The market is currently closely watching the U.S. non-farm payroll data report for April, which will be released on Friday. If the U.S. labor market experiences severe turmoil due to the Trump administration's tariff policies, the probability of the Fed initiating its first rate cut of the year in June may significantly increase. Fed Governor Waller has repeatedly emphasized that if high tariff policies force U.S. companies to make larger-scale layoffs, he will support a rate cut to protect the U.S. labor market.

A piece of good data

On April 30, Eastern Time, the U.S. Bureau of Economic Analysis released data showing that the Fed's preferred inflation indicator—the U.S. PCE price index—cooled in March.

Specifically, the U.S. PCE price index in March rose 2.3% year-on-year, the lowest level since last fall, slightly higher than the expected 2.2% and a previous value of 2.5%; the month-on-month PCE price index for March was 0%, in line with expectations, with a previous value of 0.3%, marking the first time in nearly a year that PCE month-on-month remained flat; the core PCE price index in March rose 2.6% year-on-year, in line with expectations, with a previous value of 2.8%. The month-on-month core PCE price index for March was 0%, in line with expectations, with the previous value revised from 0.37% to 0.5%. The month-on-month core PCE also remained unchanged, marking the mildest reading in nearly five years.

Among them, the core service prices—which exclude housing and energy—are a closely watched category that has barely changed and is also at its mildest level since 2020.

PCE is the Fed's preferred inflation indicator, as officials believe it better measures long-term trends.

Following the release of this data, concerns about a resurgence of high inflation in the U.S. have eased, with traders expecting the Fed to cut rates four times by the end of 2025, each by 25 basis points.

As a result, the U.S. stock market, which was initially down significantly, staged a collective rebound, recovering all initial losses, with the Dow Jones and S&P 500 indices ultimately closing up, while the Nasdaq's losses narrowed to 0.09%.

Nick Timiraos, a well-known financial journalist known as the 'Fed's mouthpiece', stated that although the 12-month PCE figure is 2.3%, close to the Fed's target of 2%, the annualized inflation rates for six months and three months are around 3%.

Timiraos further pointed out that the core PCE data for February was significantly revised upward from 0.37% to 0.50%, making the annualized core PCE inflation rate for March at 3% for six months and 3.5% for three months, both higher than the 12-month core PCE annualized inflation rate of 2.6%, which is very close to the lowest level in four years.

It is worth noting that U.S. consumer spending increased by 0.7% month-on-month in March, the largest increase since the beginning of 2023, with an expected increase of 0.5% and a previous value of 0.1%; March's Personal Consumption Expenditures (PCE) rose by 0.7% month-on-month, expected to rise by 0.6%, with a previous value of 0.4%. This indicates that American households are actively consuming before the new tariffs take effect.

Additionally, on an annualized quarterly basis, U.S. consumer spending on motor vehicles and parts surged by 56.6% in March.

Wall Street warns that as the Trump administration's tariff policies take effect, American consumers will also face price increases for their daily necessities. Companies such as Amazon, Temu, and Shein have recently significantly raised the prices of a range of imported daily goods in the U.S. to reflect the impact of Trump's high tariffs.

Goldman Sachs previously warned that the core PCE price index annual rate in the U.S. is expected to rise to 3.5% by the end of 2025, marking a new high since September 2024.

The Federal Reserve's decision

On April 30 at local time, U.S. President Trump stated that the Federal Reserve should lower interest rates, which would be a good thing for those looking to buy homes and other items.

According to the schedule, the Federal Open Market Committee (FOMC) will hold a policy meeting from May 6 to 7 local time.

The CME 'Fed Watch' tool shows that the probability of a rate cut next week is only 5.6%, while the probability of keeping rates unchanged is 94.4%. However, the probability of a rate cut at the June meeting has risen to 65.5%, with a probability of 34.5% for keeping rates unchanged in June.

Although Fed Chair Powell and other officials have recently expressed that the Fed may take a cautious approach before adjusting policies, traders currently expect the Fed to cut rates by a full 100 basis points by the end of this year.

City Index and Forex.com analyst Fawad Razaqzada stated that the weak economic data for the first quarter in the U.S. may prompt the Federal Reserve to cut interest rates, and the Fed is now more likely to act quickly on rate cuts. The weak data may also encourage Trump to relax tariffs and expedite trade agreements.

The Chief Investment Officer of Navellier & Associates stated, 'If the U.S. government quickly announces a series of trade agreements, optimism will rise, and the Fed may cut rates soon. However, if it drags on for weeks or even months, the damage to the supply chain and inevitable inflation could trigger stagflation, which would be very detrimental to the U.S. stock market.'

Cleveland Fed President Harker recently stated that if economic data can provide clear direction by June, the Fed may take action in June. Federal Reserve Governor Waller, who has long held a hawkish stance on monetary policy, has recently shifted toward a dovish position, repeatedly emphasizing that if the high tariff measures implemented by the Trump administration force U.S. companies to make larger-scale layoffs, he will support a rate cut to protect the U.S. labor market.

The market is currently closely watching the U.S. non-farm payroll data report for April, which will be released on Friday. Economists warn that the U.S. labor market may face severe turmoil due to the Trump administration's tariff policies, which could significantly increase the likelihood that the Fed will begin its first rate cut of the year in June.

Apollo Global Management's Chief Economist Torsten Slok stated, 'The U.S. employment report for April will be released on May 2 (Friday) Eastern Time, and some leading indicators suggest that the U.S. labor market may show a significant weakening trend in the coming months.'