—— Subvert traditional financial logic and unlock new ways to earn 'sleeping income'!

One, why is traditional P2P being eliminated?

Over the past decade, P2P lending has swept the globe in the name of 'disintermediation,' but has repeatedly faced problems such as information opacity, weak risk control, and rigid interest rates.

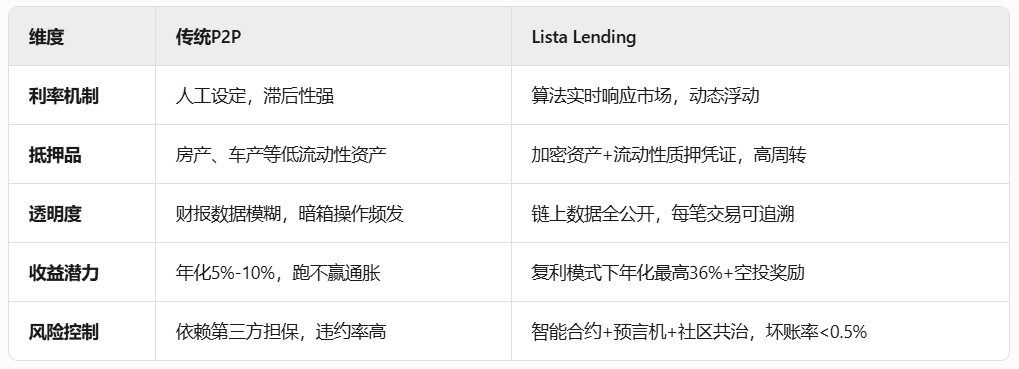

Pain point 1: One-size-fits-all interest rates

Traditional platforms use fixed interest rates 'one size fits all,' forcing borrowers with poor qualifications to bear high interest, while lenders cannot dynamically adjust their portfolios when their funds are idle.

Pain point 2: Single collateral

Most platforms only accept heavy asset pledges like real estate and vehicles, making it hard for ordinary people to participate, and liquidity is poor.

Pain point 3: Risk black box

Manual review efficiency is low, with a bad debt rate as high as 4%-5% (e.g., Lending Club), user funds are as safe as walking on thin ice.

And today, blockchain technology is rewriting the rules!

——————————————————————————

Two, Lista Lending: Redefining 'lending freedom'

On April 7, 2025, the decentralized lending protocol Lista DAO officially launched Lista Lending, igniting the DeFi lending revolution with three major moves: dynamic interest rates + intelligent risk control + multi-chain ecosystem!

1. Dynamic interest rates: The market decides, earnings never sleep

Real-time algorithmic pricing: Using Chainlink oracles to capture network-wide supply and demand data, interest rates automatically adjust every 30 seconds.

Case: If market lending demand surges, interest rates can spike from 6% to 12%, doubling lender earnings!

Step-by-step incentives:

New users enjoy 0% interest on their first loan (only pay a 0.1% handling fee)

Long-term locked users trigger accelerated compound interest (annualized yield stacked up to 18%)

2. Collateral revolution: Everything can be pledged, liquidity skyrockets

Multi-chain asset interoperability: Supports over 30 crypto assets such as BNB, ETH, sLISBNB as collateral, with the minimum collateral rate (MCR) as low as 50%, lending up to 70% of the collateral value.

Liquidity staking overlap:

- Pledge BNB to generate slisBNB (liquidity staking certificate)

- Use slisBNB to borrow lisUSD, achieving 'three benefits with one fish': staking income + lending leverage + governance dividends.

3. Risk control black technology: Zero delay in liquidation, safety is visible

Dual insurance mechanism:

- Isolated vaults: Collaterals of different risk levels are stored in separate pools to avoid systemic risks.

- Oracle sentinel: When price fluctuations exceed thresholds, automatically trigger liquidation and freeze accounts, completing asset disposal within 5 seconds.

veLISTA governance rights: Users holding governance tokens veLISTA can vote to adjust risk control parameters and participate in the 'rule-making rights' competition.

——————————————————————————

Three, the ultimate showdown with traditional P2P: Who is the future?

——————————————————————————

Four, how can ordinary people navigate Lista Lending?

Scenario 1: Newbies earn 'sleeping income' effortlessly

Operational path:

Pledge 1 BNB (worth $300) → Borrow $210 lisUSD

Deposit lisUSD into yield farms (like PancakeSwap) → Annual yield 12%

Net income: $210×12% = $25.2/year, leveraging returns to 8.4%!

Scenario 2: Advanced players 'nested' impact

Strategy portfolio:

- Use ETH as collateral to borrow DAI → Purchase ETH → Pledge ETH to borrow DAI (3x leverage)

- Match high-yield deposits through the Morpho protocol, with a comprehensive annualized rate exceeding 50%.

Scenario 3: Low-cost financing for business owners

Case: A cross-border e-commerce seller pledges inventory NFTs (such as BAYC) to borrow USDC, solving cash flow issues, with an interest rate of only 7.2% (traditional bank loans require 15% + mortgage registration fees).

——————————————————————————

Five, risk warning: The sobering agent behind the celebration

1. Market volatility risk: Crypto asset collateral may trigger liquidation due to market crashes (e.g., the 3AC collapse event).

2. Smart contract vulnerabilities: Although audited by Certora, theoretical attack surfaces still exist due to code complexity.

3. Regulatory uncertainty: Some countries may define over-collateralized lending as 'securities issuance,' leading to compliance risks.

——————————————————————————

Six, the future is here: Lista DAO's ecological ambition

Cross-chain expansion: Launching Ethereum Layer2 in Q3 2025, supporting interoperability with MakerDAO and Aave assets.

Credit system revolution: Introducing zero-knowledge proofs (ZK-SNARKs) to achieve 'anonymous lending + credit scoring.'

DAO governance upgrade: veLISTA holders can propose the issuance of 'regional stablecoins' to compete for global payment discourse power.

——————————————————————————

Conclusion

The emergence of Lista Lending is not only a victory of technology but also a dimensional blow to traditional finance. Here, everyone can participate in the financial rules — every mortgage, every vote, is reshaping the future financial landscape.

#ListaLending革新BNBChain借贷 @ListaDAO @BNBxyz

Note: Data for this article comes from: Lista DAO white paper, DeFi lending protocol analysis, industry research reports. The market has risks; investment requires caution.