With less than a week until the Trump administration's tariff implementation day on April 2, the strength of the policy is in question and may not fully materialize as previously envisioned. The Trump team aims to use tariffs to protect domestic industries and generate revenue to fill the deficit, but faces the risk of economic pressure. The implementation of tariffs may follow either a path of opponent compromise or a tit-for-tat response, with the latter being more probable in the short term. The Federal Reserve's slow response to tariffs has affected U.S. stocks, and the S&P 500 is at a critical point. The crypto market is also impacted, with doubts about Bitcoin's rebound; the April 2 policy will become a turning point influencing long-term direction.

This soon-to-be-implemented tariff policy is seen by the Trump administration as a key step in reshaping America's trade landscape. However, as policy details emerge, the market questions its strength and impact. In this global game, both traditional markets and the crypto sector are affected, and April 2 will reveal the future direction. This article is sourced from Luke, written by Mars Finance, and reprinted by Foresight News.

(Background: JPMorgan: The risks of Trump's tariff war are becoming clearer; it's time to 'stop selling the highs' of U.S. stocks.)

Less than a week remains until the highly anticipated 'April 2 Tariff Implementation Day.' This day has been termed 'Liberation Day' by the Trump administration, carrying the ambition to reshape America's trade landscape.

However, as media buzz begins to rise, the script for this policy drama seems less radical than the outside world expected. Meanwhile, the crypto market — a sector particularly sensitive to macroeconomic fluctuations — is also stirring under the shadow of tariffs.

A 'Moderate Shift' on Tariff Implementation Day?

Latest news indicates that the tariff policy on April 2 may not fully realize the grand blueprint previously outlined by Secretary of Commerce Lutnik. He envisioned a 'three-layered' tariff system: based on reciprocal tariffs, supplemented by targeted tax increases for specific industries and countries. However, recent rumors suggest that the latter two may be eased. It’s like a meticulously prepared banquet that ends up serving a simplified set meal — missing some seasonings, but the main dish remains.

Why has this adjustment occurred? The reasons are not hard to speculate. The Trump team knows well that tariffs are a double-edged sword. Since taking office, its trade policies have subjected global markets to severe shocks: the market value of U.S. stocks has evaporated by trillions of dollars, supply chain pressures have driven up prices, and even eggs have become 'luxury goods.' If tariffs are pushed to their limits at this time, the U.S. economy could be the first to feel the pressure. Goldman Sachs economists warn that despite the calm on the surface, this 'moderate stance' harbors risks of 'negative surprises.' The market expects a reciprocal tariff rate of about 9%, but Goldman estimates the actual figure could double to 18%. This gap is enough to make traders hold their breath, waiting for the other shoe to drop.

At the same time, the report on unfair trade practices set to be released on April 1 will become a key indicator. This report will reveal the U.S. investigation tendencies toward trade partners, directly affecting the pace and intensity of subsequent tariffs. If the report accuses certain countries of clear 'sheep shearing' behavior, Trump may seize the opportunity to escalate; if the tone is softer, the market may welcome a brief respite. Regardless, this report will serve as a preview for interpreting the plot of 'Liberation Day.'

Trump's Calculation — Fairness, Fairness, or Damn Fairness?

To understand the logic of tariff implementation, one might listen to the statements of core members of the Trump team. Recently, Treasury Secretary Basent and Commerce Secretary Lutnik shared their thoughts on the All-in Podcast. Lutnik reflected on history, noting that from 1880 to 1913, the U.S. relied entirely on tariffs to maintain its finances without needing to levy income taxes. After World War II, to support global reconstruction, the U.S. voluntarily lowered tariffs but allowed other countries to maintain high barriers, becoming the 'most open trade' loser. For instance, U.S. car exports to a certain country incur a 20% tariff, while the other country's vehicles entering the U.S. only require a 5% tariff. This imbalance prompted Trump to exclaim, 'Fairness, fairness, or damn fairness!'

Trump's intentions are clear: first, to protect domestic industries through tariffs and attract manufacturing back; second, to generate fiscal revenue to fill the $2 trillion deficit gap. Lutnik proposed a 'three-pronged' plan: increased tariff revenue, sovereign fund investments, and the 'immigrant golden card' project — the latter reportedly able to sell 1,000 cards a day, with Trump optimistically estimating it could attract 1 million buyers. As for the other half of the deficit, hopes rely on the 'Efficiency Department' to cut $1 trillion in wasteful spending. This department aims to eliminate 25% of the 'fat' in annual fiscal spending of $6.5 trillion, which sounds ambitious, but execution is undoubtedly fraught with challenges.

Treasury Secretary Basent analyzes the issue from a macro perspective, listing three major pain points of the U.S. economy: high debt, uncontrolled inflation, and declining manufacturing. His prescription includes cutting spending, reshaping the trade system, and revitalizing the middle class. Unlike Lutnik's radical approach, Basent emphasizes 'gradualism' to avoid triggering economic recession due to drastic measures. White House economic advisor Stephen Milan also added in a Bloomberg interview that as the world's largest consumer market, the U.S. holds the upper hand in negotiations and has the ability to force opponents to yield. This confidence stems from strength, but whether it can be translated into a winning situation depends on how opponents respond.

The tariff implementation may present two pathways:

One is that opponents compromise, lowering tariffs on the U.S., resulting in a victory for the U.S. and a rise in U.S. stocks;

The other is a tit-for-tat response, forcing Trump to escalate, leading to a short-term double loss and pressure on U.S. stocks.

In the short term, the latter is more likely, as there are few willing to show weakness first in the global game. However, in the long run, the U.S. may gradually reverse the trade imbalance with the leverage of its consumer market.

The Federal Reserve's slow response and the unresolved bottom of U.S. stocks

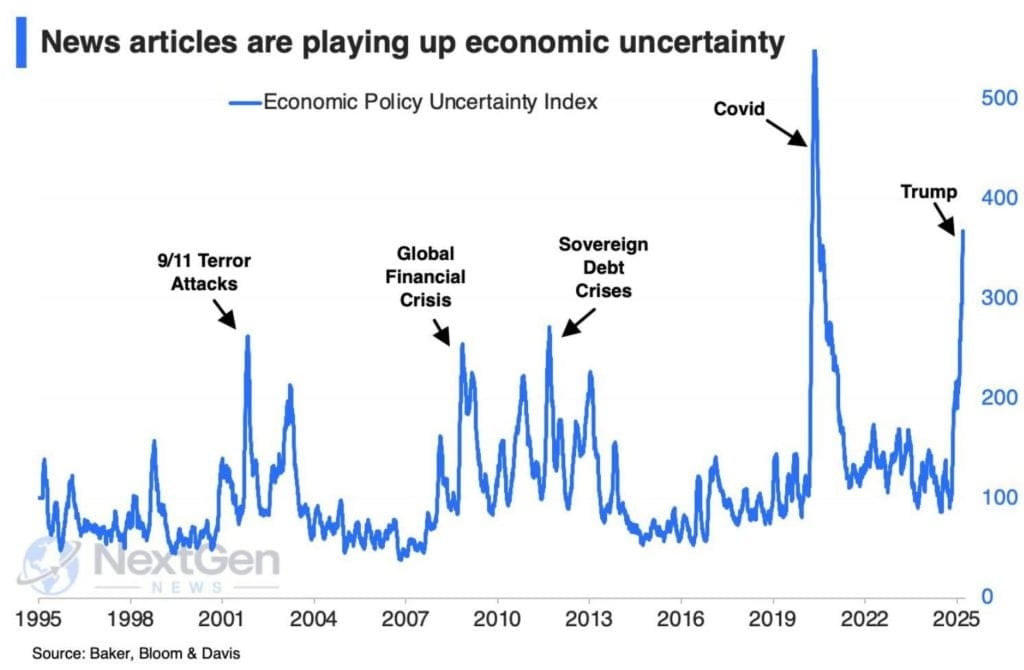

The uncertainty of tariff policies not only affects trade patterns but also transmits to capital markets through inflation and monetary policy. Looking back at 2020, the surge in inflation triggered by the COVID-19 pandemic caught the U.S. Federal Reserve off guard. Initially, the Fed was confident that inflation was 'transitory,' but by the end of 2021, Chairman Powell had to admit to Congress that it had misjudged and announced the abandonment of the term 'transitory,' subsequently initiating a substantial interest rate hike cycle. According to Bloomberg data (see Chart 1), the U.S. economic policy uncertainty index soared above 500 points at the beginning of the pandemic, reaching a historical peak. Although it has since retreated, events such as the 2022 Russia-Ukraine conflict and the 2024 Trump tariff policy have once again heightened uncertainty, with the index lingering at a high level of 200 points, far exceeding the average level from 1995 to 2019.

The Federal Reserve's response to the impact of tariffs has also been slow. Over the past few years, the supply chain pressures and rising prices caused by tariffs have significantly raised inflation expectations, but the Fed has preferred to soothe the market through dovish statements. However, this soothing can only bring about a brief rebound in U.S. stocks, not a trend reversal. The reason lies in the market's greatest uncertainty — the direction and intensity of tariff policies — which remains unresolved. From Chart 1, the economic policy uncertainty index has been accompanied by significant adjustments in U.S. stocks during historical events like the '9/11 terrorist attack', 'global financial crisis', and 'sovereign debt crisis', while the current level of uncertainty suggests that the bottom of U.S. stocks may still not have arrived. The market may need to wait for tariff policies to clarify or for more severe macro shocks to trigger a comprehensive reshuffle.

The recent performance of the S&P 500 further confirms this concern. According to data from Bloomberg and MacroBond, the S&P 500 has fallen 7.8% since its peak in February, and last week even saw a drop of 10%. Historical data shows that if the S&P 500 averages another drop of at least 5% in the next five months, the U.S. economy is likely to fall into recession (as indicated by the yellow line in Chart 2).

Conversely, if the S&P 500 can regain lost ground in the next 4 to 5 months, it could avoid economic decline (as shown by the black line in Chart 2). However, this data merely represents averages; if the economy does enter a recession, U.S. stocks may fall by at least 20%. Notably, market sentiment can sometimes amplify volatility; for instance, in 2022, the S&P 500 fell by more than 20%, yet a recession did not occur. At that time, the panic of 'expected recession' dominated the market's performance in the latter half of the year.

Currently, the S&P 500 is at a critical crossroads. Chart 2 shows that if the economy avoids recession, the stock market should rebound quickly; however, if recession risks intensify, selling pressure may continue. The ambiguity surrounding tariff policies undoubtedly exacerbates this uncertainty. If the policy on April 2 turns out to be unexpectedly aggressive, panic in the market may further push down U.S. stocks.

The crypto market is on high alert.

The direction of tariffs directly impacts the crypto market. Bitcoin recently climbed to $88,786, seeming to show signs of recovery, but industry insiders frequently issue warnings. CoinPanel trading expert Kretov points out that this rebound resembles a 'bull trap': trading volume is shrinking, retail investors are on the sidelines, funding rates have turned negative, and even 'smart money' is staying put. The market is as fragile as thin ice, and any wind or disturbance could cause it to crack. The lending rate for stablecoins on Aave has fallen to 4%, further confirming the spread of risk-averse sentiment.

What is even more concerning is the 'reluctance to sell' mentality of long-term Bitcoin holders. These 'veterans' expect higher exit prices, but inadvertently become a 'dead weight' of selling pressure in the market. Kretov believes that only when these holders sell off and the market is completely reshuffled can large players re-enter. However, signs of market washing have yet to emerge, casting doubt on the sustainability of any rebound.

Historical data rings alarm bells for the current situation. When Trump first launched the tariff war in 2018, global markets experienced severe turmoil. According to Chart 3, since the announcement of tariffs in March 2018, the S&P 500 has cumulatively fallen by 12%, while Bitcoin's drop has reached 65%, far exceeding the performance of traditional assets. The inherent nature of gains and losses in the crypto market is vividly illustrated: high risks bring high returns, but also accompany more severe downward pressures. In contrast, the Chinese index performed relatively steadily during the same period, with a cumulative decline of less than 20%, highlighting the sensitivity of different markets to tariff shocks.

CoinDesk's analysis has intensified this concern: Bitcoin is forming a 'double top' around $87,000; if this bearish signal breaks below the $86,000 'neckline,' it could dip to $75,000 in the short term. Altcoins will likely fare worse. SignalPlus partner Augustine Fan predicts that the market's soft rebound may continue until the end of the month, but the tariff announcement on April 2 will become a turning point. If the policy is moderate, Bitcoin could sprint toward $90,000, buoyed by the Fed's dovish stance; if it is unexpectedly aggressive, tightening liquidity may trigger a collective plunge.

Speculation on the Outcome

How will the tariff implementation on April 2 unfold? Based on existing information, Trump may choose a 'gentle start': setting reciprocal tariffs at 10%-12%, while delaying tariffs for specific industries and countries, preserving pressure while avoiding a hard landing for the economy. If the report on April 1 supports escalation, a second wave of attacks may arrive by mid-year. In the short term, the market may fluctuate due to expectation gaps; in the long term, if the trade war reshapes the economic landscape, recovery benefits may extend to the crypto sector.

For crypto investors, the tariff implementation day is not only a policy barometer but also a magnifying glass for sentiment. A moderate policy may ignite a short-term rebound, while aggressive escalation will test market resilience. Regardless of the outcome, this game reminds us that the interplay between macro policies and the crypto market is becoming increasingly tight; only those who understand the trends can ride the waves.