The IMF’s latest forecast has made something very clear the golden run of global growth is finally fading. After years of recovery, record markets, and stimulus-fueled optimism, the world is entering a much slower, more uncertain phase.

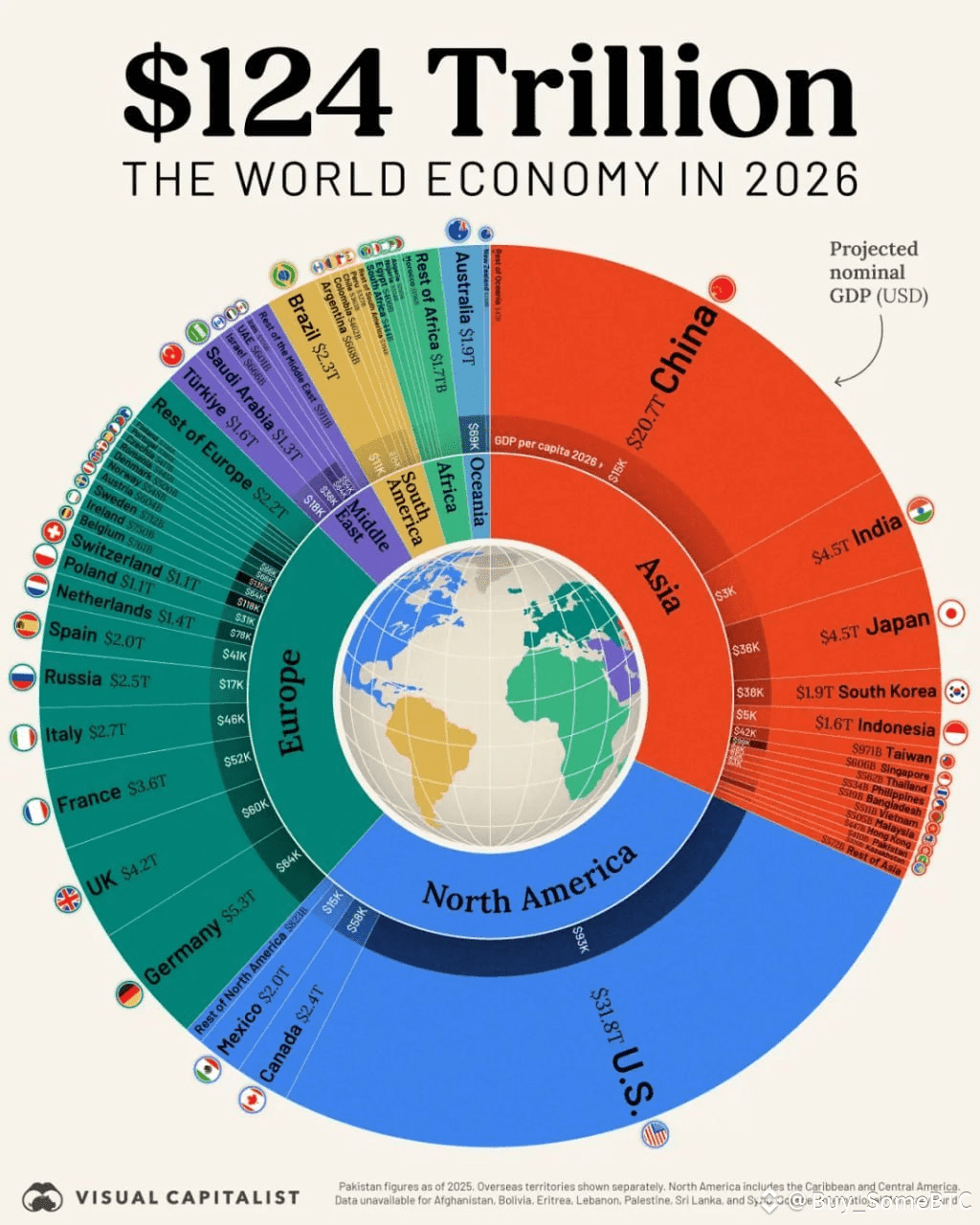

By 2026, the global economy is expected to reach around 124 trillion dollars. That sounds impressive on paper, but the momentum behind it is losing strength. Inflation may be cooling, but it has left deep scars. Debt is piling up, trade tensions are rising again, and growth engines that once drove the world economy are now sputtering.

The United States will remain the largest economy, sitting at nearly 35 trillion dollars, but growth is clearly cooling. High interest rates are biting into business profits and consumer confidence, while the once unstoppable tech rally is starting to wobble. The IMF warns that overvalued tech stocks could become a real risk to financial stability if markets turn sharply.

China is still the world’s number two, expected to hit around 21 trillion dollars, yet its story has changed.

The property market slowdown, weak exports, and heavy local debt have taken away the shine that once made China the global growth engine. India is the bright spot, rising fast with its 4.5 trillion dollar economy built on innovation and a strong domestic base. Still, its challenges remain inequality, infrastructure, and jobs.

Europe, on the other hand, seems stuck in slow motion. Germany, France, and the UK continue to add weight to the global economy, but none are growing fast enough to make a real difference. High energy costs, aging populations, and political uncertainty are holding the region back.

Emerging markets are under stress too.

Rising borrowing costs and a strong dollar have pushed many developing nations into debt troubles. Some are still recovering from the pandemic shock while others are being hit by unstable commodity prices and reduced global investments.

What’s perhaps most interesting about the IMF’s forecast is what isn’t changing. The order of the world’s largest economies will remain the same through 2026. The United States, China, India, Japan, and Germany will keep their positions. No new power is breaking through. It’s a sign that the global economy is maturing, maybe even slowing into a plateau.

And this slowdown is not just about numbers. The world itself is becoming more fragmented. Countries are pulling back into regional trade zones, building local supply chains, and putting national interests ahead of global cooperation. Protectionism is rising again. The connected world we knew is quietly giving way to smaller, divided markets.

Technology, the great equalizer, is also turning into a new fault line. AI and automation are bringing incredible efficiency, but they’re also creating waves of job losses and deep inequality. The tools that were meant to push growth forward are now forcing economies to rethink how humans fit into the system.

The IMF’s message isn’t a prediction of collapse it’s a reality check.

The boom years are gone.

The next chapter will be defined by slow, uneven growth and constant adaptation. The world won’t fall apart, but it will feel heavier to move forward.

For investors, this means chasing stability instead of speculation. For governments, it means managing debt, supporting innovation, and protecting jobs. For everyone else, it means preparing for a world where opportunity still exists but it takes more patience, skill, and timing to find it.

By 2026, the global economy will be bigger in numbers but smaller in energy. The age of easy expansion is ending.

What comes next is the test of endurance.