Key Highlights

Hyperliquid has been added to the Monetary Authority of Singapore's (MAS) Investor Alert List (IAL) — a public disclosure list, not a blacklist or enforcement action.

The Hyperliquid team responded directly, stating clearly: "It is not, and has never claimed to be, licensed or authorised by MAS, and no one should regard it as such."

No operational impact — trading, deposits, withdrawals, self-custody, and on-chain settlement all continue completely unaffected.

Being added to the IAL is common for permissionless DeFi protocols that operate without pursuing traditional licensing in specific jurisdictions — and many major exchanges and protocols have appeared on this same list previously.

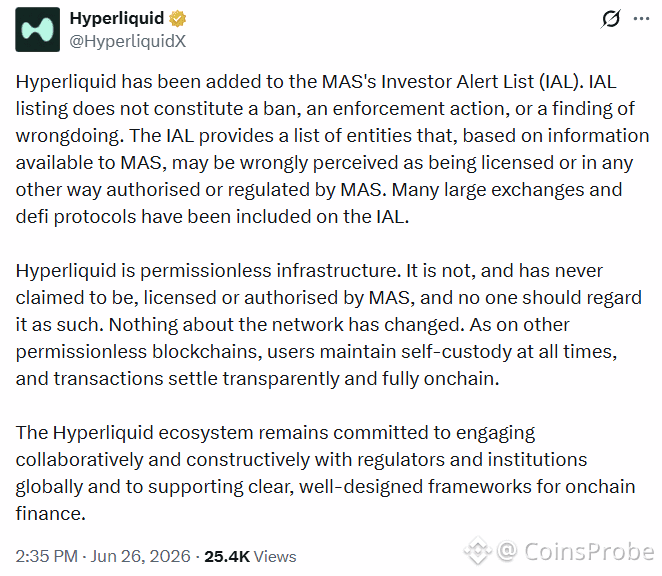

Hyperliquid has been added to the Monetary Authority of Singapore’s Investor Alert List (IAL) — a development the team addressed directly and promptly, clarifying exactly what the listing does and does not mean for users and the protocol’s operations.

What Is the MAS Investor Alert List?

The Investor Alert List (IAL) is a public warning list maintained by Singapore’s financial regulator, the Monetary Authority of Singapore. Its specific purpose is to flag entities that may be wrongly perceived by the public as being licensed, authorised, or regulated by the MAS — when in fact they are not.

This is an important distinction worth emphasising clearly: the IAL is not a blacklist of illegal operations. It functions as a disclosure and investor education tool rather than an enforcement mechanism. Many major centralised exchanges and decentralised protocols have appeared on this list previously — its presence is not, by itself, an indication of wrongdoing, fraud, or regulatory violation.

Hyperliquid’s Official Response — Direct and Unambiguous

The Hyperliquid team addressed the listing head-on, clarifying several key points without ambiguity:

“Hyperliquid is permissionless infrastructure. It is not, and has never claimed to be, licensed or authorised by MAS, and no one should regard it as such.”

The team’s statement laid out the core facts clearly:

Hyperliquid is permissionless infrastructure — it has never claimed, at any point, to be licensed or authorised by the MAS or any equivalent regulatory body in any specific jurisdiction.

The IAL addition is not a ban or penalty — it does not constitute any regulatory enforcement action, fine, or finding of wrongdoing against the protocol.

Nothing about the network has changed — the underlying protocol, its functionality, and its operations remain exactly as they were before this listing.

Users maintain full self-custody — at all times, consistent with Hyperliquid’s core architecture as a decentralised, on-chain trading venue.

All transactions settle transparently, fully on-chain — the network’s fundamental transparency and settlement mechanics are entirely unaffected by this regulatory disclosure listing.

The team also reaffirmed its broader posture toward regulation — committing to engage constructively with regulators globally while continuing to build out decentralised, on-chain financial infrastructure. This framing positions the IAL listing not as an adversarial moment, but as a routine part of operating permissionless infrastructure across a global regulatory landscape that varies significantly by jurisdiction.

Source: @HyperliquidX (X)

What This Means for Users — Practically Nothing Changes

For Hyperliquid users specifically, the practical impact of this listing is effectively zero:

No impact on trading, deposits, withdrawals, or platform functionality. Every core feature of the protocol continues operating exactly as before.

The protocol remains fully operational — across perpetuals, spot, and outcome markets, with no disruption to any existing product.

Self-custody and on-chain settlement continue as normal — the foundational architecture that distinguishes Hyperliquid from custodial centralised platforms is entirely untouched by this development.

This is largely a compliance labelling matter — common for decentralised platforms operating in the regulatory grey area that exists globally for permissionless, non-custodial financial infrastructure that does not fit neatly into traditional licensing frameworks designed for centralised intermediaries.

Why This Happens to Growing DeFi Protocols

As one of the leading decentralised perpetuals exchanges by trading volume — a position we have documented extensively throughout 2026, including HIP-3 open interest reaching new all-time highs and the platform’s continued institutional credibility build-out through products like Portfolio Margin — Hyperliquid’s rapid growth has naturally attracted increasing regulatory attention from jurisdictions around the world.

Being added to a disclosure or alert list like Singapore’s IAL is a relatively routine occurrence for permissionless DeFi protocols that, by design, do not pursue traditional licensing arrangements in every specific jurisdiction where users might access the platform. This is a structural feature of how permissionless, non-custodial protocols interact with a global patchwork of financial regulation — not a unique or unusual development specific to Hyperliquid.

Community Reaction — Mixed but Largely Unconcerned

The announcement has drawn a predictably mixed but largely measured reaction from the Hyperliquid community:

One view treats this as standard regulatory noise that any genuinely decentralised, permissionless project should expect to encounter periodically as it scales and attracts regulatory attention across more jurisdictions.

Another view sees the listing as a useful reminder of the ongoing, structural tension between permissionless financial innovation and traditional regulatory oversight frameworks — a tension that is unlikely to fully resolve as long as protocols like Hyperliquid continue operating as genuinely decentralised infrastructure rather than licensed financial intermediaries.

Neither view, notably, treats this as a fundamental threat to the protocol’s operations or its trajectory — consistent with the team’s own framing that nothing material has actually changed.

Bottom Line

Hyperliquid’s addition to Singapore’s MAS Investor Alert List is a disclosure and investor-education listing — not a ban, not an enforcement action, and not a finding of wrongdoing. The team’s response was direct, transparent, and consistent with how Hyperliquid has always described itself: permissionless infrastructure that has never claimed regulatory licensing or authorisation from the MAS or equivalent bodies.

Trading, deposits, withdrawals, self-custody, and on-chain settlement all continue completely unaffected. This is a routine compliance labelling matter that reflects the broader, unresolved tension between permissionless DeFi infrastructure and traditional financial regulatory frameworks — a tension that growing protocols like Hyperliquid will likely continue encountering as they expand across additional jurisdictions globally.

The protocol’s core operations, product roadmap, and growth trajectory remain entirely unaffected.

Disclaimer: The views and analysis presented in this article are for informational purposes only and reflect the author’s perspective, not financial advice. Technical patterns and indicators discussed are subject to market volatility and may or may not yield the anticipated results. Investors are advised to exercise caution, conduct independent research, and make decisions aligned with their individual risk tolerance.