In the world of international finance, change rarely happens overnight. Systems that move trillions of dollars don’t get replaced easily—they evolve slowly, cautiously, and often behind the scenes. But every once in a while, a development surfaces that hints at a deeper shift already underway. The recent claim that XRP-based transactions in Japan can be up to 60% cheaper than traditional SWIFT-based transfers is one of those moments.

At first glance, it sounds like just another bold crypto headline. But if you look closely, it reveals something far more important: a growing tension between legacy financial infrastructure and newer, more efficient digital alternatives.

The Problem with Cross-Border Payments

To understand why this matters, you need to understand how international payments actually work.

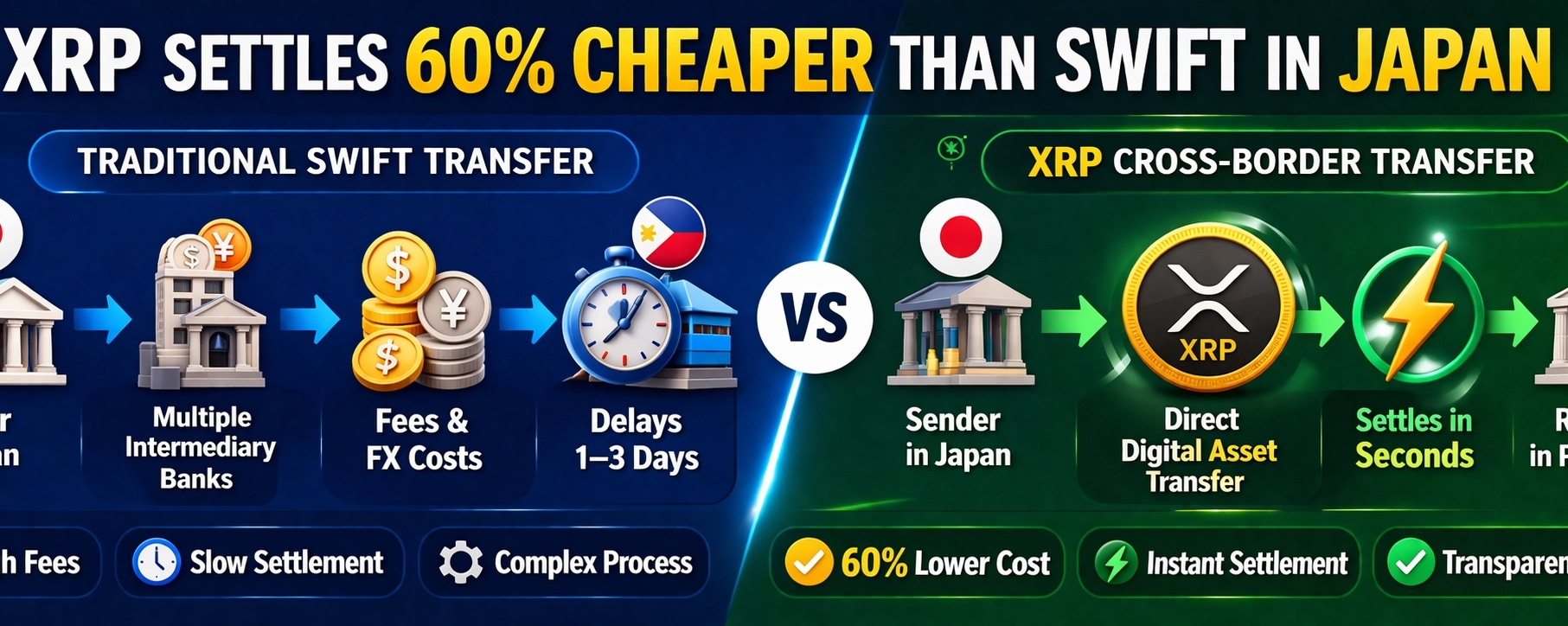

When money moves from one country to another through traditional systems like SWIFT, it doesn’t travel in a straight line. Instead, it passes through a chain of banks—each acting as a middleman. These are called correspondent banks, and each one may charge fees, apply exchange rates, and add processing time.

This system has worked for decades. It’s reliable and trusted. But it’s also expensive and slow.

A transfer that looks simple on the surface—say, sending money from Japan to the Philippines—might take one to three days to settle. Along the way, costs pile up: transaction fees, FX spreads, and the hidden cost of maintaining liquidity in multiple countries.

For businesses and remittance providers, these inefficiencies aren’t just annoying—they’re expensive.

Japan as a Testing Ground

Japan has quietly become one of the most interesting places to watch this transformation unfold.

Through partnerships involving companies like Ripple and financial groups such as SBI Holdings, XRP has already been tested in real-world remittance corridors, particularly between Japan and Southeast Asia.

These corridors are ideal for experimentation. They handle large volumes of payments, especially from overseas workers sending money home. That makes even small improvements in cost and speed highly valuable.

Recent pilot demonstrations presented at fintech events in Tokyo suggest that XRP-based settlement can reduce costs by as much as 60% compared to traditional methods. Even more striking, these transactions reportedly settle in just a few seconds.

Why XRP Changes the Equation

At the heart of this shift is a simple idea: remove unnecessary steps.

Instead of relying on multiple banks to pass money along, XRP acts as a bridge asset. Funds are converted into XRP, transferred almost instantly, and then converted into the destination currency on the other side.

This approach eliminates the need for pre-funded accounts—money that banks traditionally have to hold in foreign countries just to facilitate transfers. By freeing up this capital, institutions can operate more efficiently and reduce costs.

It also compresses the transaction timeline dramatically. What used to take days can now happen in seconds.

The Cost Advantage—And Its Limits

The “60% cheaper” figure is compelling, but it’s important to interpret it carefully.

Not every transaction will see the same level of savings. The benefits of XRP are most noticeable in specific corridors—especially where traditional systems are less efficient or where liquidity is fragmented.

It’s also worth noting that SWIFT itself isn’t a payment system in the same way XRP is. It’s a messaging network—a way for banks to communicate payment instructions securely. The actual movement of money depends on the banks behind the scenes.

So when people compare XRP to SWIFT, they’re really comparing two different approaches to the same problem: how to move money across borders efficiently.

Speed: The Hidden Advantage

Cost is only part of the story. Speed is just as important.

In today’s digital economy, waiting days for a payment to settle feels outdated. Businesses need faster cash flow. Individuals want instant access to funds. Delays create friction—and friction creates opportunity for disruption.

This is where XRP has a clear edge. Near-instant settlement isn’t just a technical improvement; it changes how money can be used. It enables real-time payments, reduces uncertainty, and opens the door to new financial services.

Why Japan Matters Globally

Japan’s role in this story goes beyond its borders.

It is one of the few major economies where traditional financial institutions have actively explored blockchain-based payment solutions at scale. The collaboration between Ripple and SBI has created a unique environment where innovation can be tested in real-world conditions, not just in theory.

If XRP proves consistently effective in Japan’s remittance corridors, it could serve as a blueprint for other regions—especially in Asia, where cross-border payments are a daily necessity.

Not a Replacement—Yet

Despite the excitement, it would be a mistake to assume that XRP is about to replace SWIFT entirely.

The global financial system is deeply interconnected, and SWIFT remains a critical piece of that infrastructure. It has decades of trust, regulatory integration, and network effects that are not easily replicated.

What’s more likely is coexistence.

Traditional systems will continue to operate, especially in large-scale institutional contexts. At the same time, blockchain-based solutions like XRP will carve out niches where they offer clear advantages—particularly in high-volume remittance corridors.

A Shift in Perspective

The real significance of the “60% cheaper” claim isn’t the number itself. It’s what the number represents.

It suggests that the economics of cross-border payments are changing.

For years, blockchain technology has been discussed in terms of potential. Now, it’s being measured in terms of performance—cost savings, settlement times, and operational efficiency.

That’s a different conversation entirely.

Looking Ahead

If the trends emerging from Japan continue, we may be entering a new phase in global payments—one where efficiency becomes as important as trust, and where digital assets play a practical role in everyday financial operations.

XRP may not replace SWIFT, but it doesn’t have to.

All it needs to do is prove that there’s a better way to move money—and in certain parts of the world, it already might be doing exactly that.